By Patricia Laya

Venezuela has defaulted on a gold swap agreement valued at $750 million with Deutsche Bank AG, prompting the lender to take control of the precious metal which was used as collateral and close out the contract, according to two people with direct knowledge of the matter.

As part of a financing agreement signed in 2016, Venezuela received a cash loan from Deutsche Bank and put up 20 tons of gold as collateral. The agreement, which was set to expire in 2021, was settled early due to missed interest payments, said the people, who asked not to be named speaking about a private matter.

In the meantime, opposition leader Juan Guaido’s parallel government has asked the bank to deposit $120 million into an account outside President Nicolas Maduro’s reach, which represents the difference in price from when the gold was acquired to current levels. As part of efforts to unseat Maduro, the U.S. and more than 50 countries have recognized Guaido as the legitimate leader of Venezuela even though he still doesn’t control key institutions at home, including the central bank.

“We’re in touch with Deutsche Bank to negotiate the terms under which the difference owed to the central bank will be paid to the legitimate government of Venezuela," said Jose Ignacio Hernandez, Guaido’s U.S.-based attorney general. “Deutsche Bank can’t risk negotiating with the central bank’s illegitimate authorities," particularly after it was sanctioned by the U.S. government, Hernandez said.

A spokesman for Deutsche Bank declined to comment. A press official for Venezuela’s Central Bank didn’t immediately reply to a request for comment.

It’s the second time this year that the Maduro regime has failed to make good on financing agreements which have resulted in losses at a time when reserves are at a record low. Dwindling gold holdings have become one of Maduro’s last remaining sources to keep his regime afloat and his military forces loyal. The central bank missed a March deadline to buy back gold from Citigroup for nearly $1.1 billion. Before that, the Bank of England refused to give back $1.2 billion worth of Venezuelan gold.

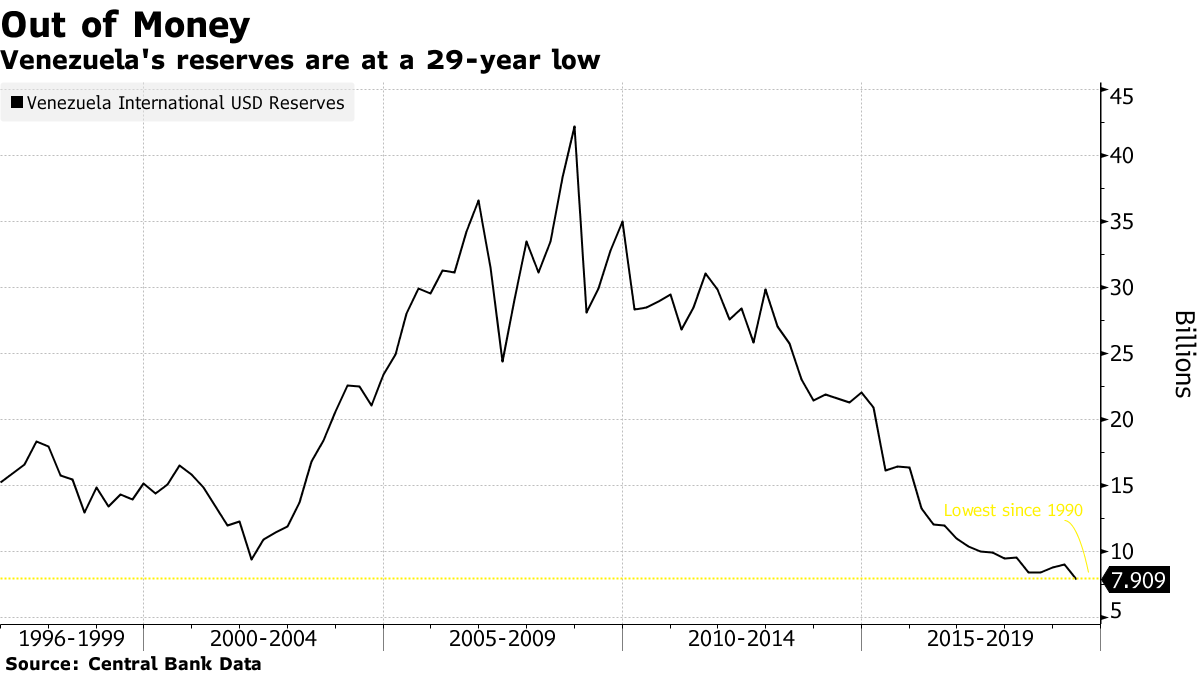

While Maduro is becoming increasingly cut off from the global financial network due to sanctions, it still managed to sell $570 million in gold last month, prompting reserves to tumble to a 29-year low of $7.9 billion. The government blew through more than 40% of Venezuela’s gold reserves last year, selling to firms in the United Arab Emirates and Turkey in a desperate bid to fund government programs and pay creditors.

Venezuela defaulted on its dollar-denominated bonds in late 2017.

Original source: Bloomberg

Reproduction, in whole or in part, is authorized as long as it includes all the text hyperlinks and a link back to the original source.

The information contained in this article is for information purposes only and does not constitute investment advice or a recommendation to buy or sell.