The price of gold rebounded further, despite hawkish Powell’s letter to Senator Rick Scott.

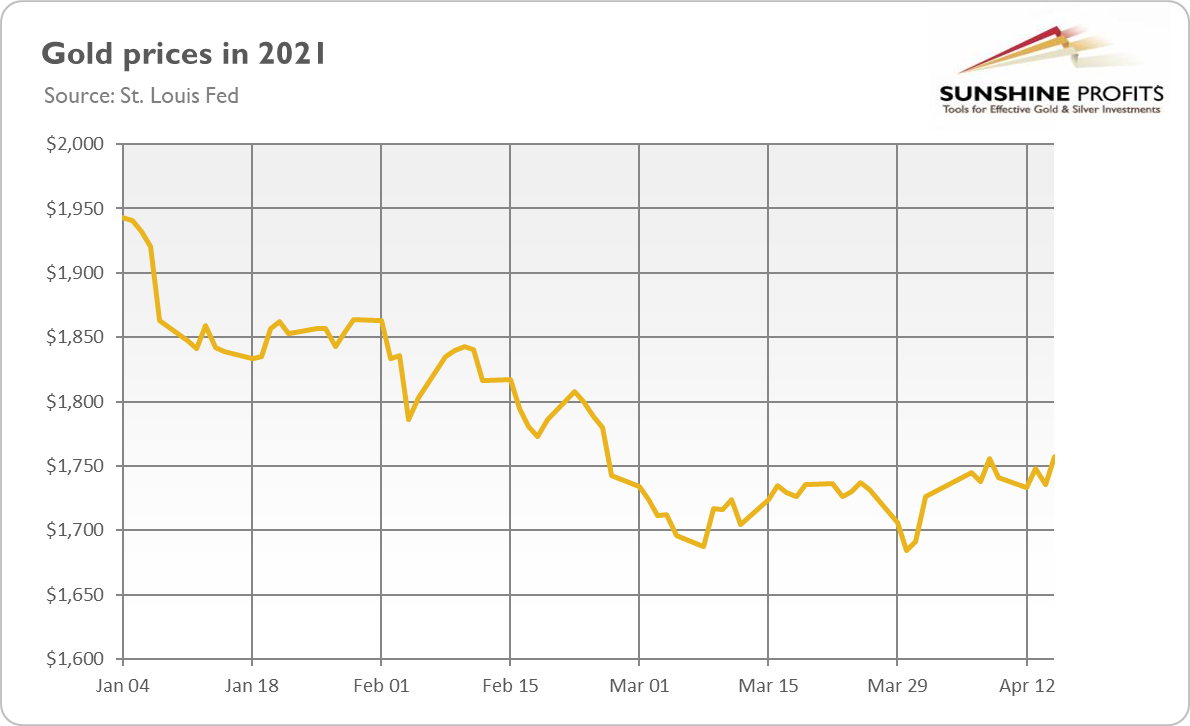

The second quarter of 2021 started much better than the first one for the gold bulls. As the chart below shows, the yellow metal rebounded from the late March bottom of $1,684 to $1,778 on Tuesday (April 20).

Is it a temporary recovery in a long, downward slide or a return to the bull market that started in 2019? Well, it’s probably too early to determine whether that’s the case. What is, however, crucial here is that the yellow metal has managed to go up, despite some bearish news. The most important fact is that Powell has replied to the letter from Senator Rick Scott on rising inflation and public debt. The Fed Chair’s reply was rather hawkish, as he said that any overshoot of inflation target would be limited:

We do not seek inflation that substantially exceeds 2 percent, nor do we seek inflation above 2 percent for a prolonged period (…) we are fully committed to both legs of our dual mandate – maximum employment and stable prices (…) We understand well the lessons of the high inflation experience in the 1960s and 1970s, and the burdens that experience created for all Americans. We do not anticipate inflation pressures of that type, but we have the tools to address such pressures if they do arise.

Although Powell didn’t say anything surprising, his tone and emphasis on the commitment to stable prices could be interpreted as generally hawkish and, thus, negative for the gold prices. However, the yellow metal continued its rebound, which is encouraging.

Implications for Gold

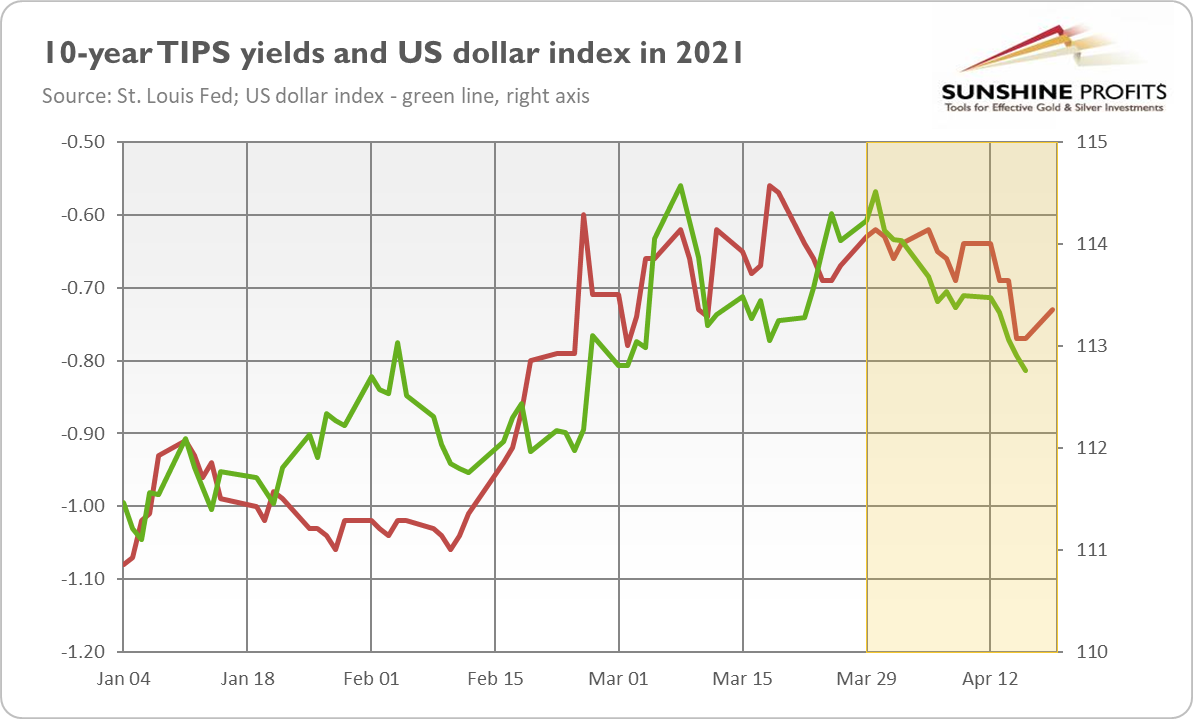

So why has gold been rising recently? Well, in a sense, the reason might be simple: the sentiment was so negative that the downward trend had to reverse. However, there are also some fundamental factors at play here. First of all, the rallies both in the bond yields and the US dollar have stalled. As the chart below shows, both the greenback and the real interest rates have receded from their March peaks..

The declines in the bond and forex markets enabled gold to catch its breath. Of further importance is that they started falling when it became clear that the Fed would be more dovish and tolerant of higher inflation than was originally believed by the markets.

Second, there has been a surge in global coronavirus cases which renewed a demand for the safe-haven assets, such as gold. Also, in the US, the number of confirmed cases and hospitalizations is increasing in some areas of the country, despite the vaccination progress. That is the effect of the new variants of the virus and the pandemic fatigue, i.e., many people tired of it have dropped their infection control measures.

Third, inflation is accelerating, which is becoming increasingly visible. For example, the latest IHS Markit U.S. Manufacturing PMI shows that costs and charges have historically elevated in March.

Supplier lead times lengthened to the greatest extent on record. At the same time, inflationary pressures intensified, with cost burdens rising at the quickest rate for a decade. Firms partially passed on higher input costs to clients through the sharpest increase in charges in the survey’s history.

Commenting on the numbers, Chris Williamson, Chief Business Economist at IHS Markit, said:

Raw material prices are increasing at the sharpest rate for a decade and factory gate selling prices have risen to a degree not seen since at least 2007. The fastest rates of increase for both new orders and prices was [sic] reported among producers of consumer goods, as the arrival of stimulus cheques in the post added fuel to a marked upswing in demand.

What matters here is that the inflationary pressure is likely to remain with us for a while, despite the pundits’ claims that it’s triggered merely by temporary factors. In the 1970s, they were talking the same – until stagflation emerged and gold shined.

Reproduction, in whole or in part, is authorized as long as it includes all the text hyperlinks and a link back to the original source.

The information contained in this article is for information purposes only and does not constitute investment advice or a recommendation to buy or sell.