Picking up where DoubleLine CEO Jeff Gundlach left off yesterday with his Ira Sohn recommendation, which as a reminder was to short Facebook on concerns of regulatory crackdown and go long commodities ahead of a late-cycle inflationary boom, on Tuesday Gundlach spoke at an event for DoubleLine clients and reiterated his late-cycle skepticism, warning that treasuries are still "not attractive" even though the benchmark 10Y yield briefly crossed the key 3% threshold earlier in the day.

The bond king said he is in no rush to buy, well, bonds, because he expects that, based on recent Core CPI prints and the NY Fed underlying inflation gauge, that US inflation will go even higher, sending Treasury prices lower. The fund manager said some indicators are suggesting 3% inflation, and noted that while it might not get there, "something higher than the current rate is sensible."

Quoted by Reuters, Gundlach said the Fed’s "quantitative tightening", which as we described earlier today is already taking the high-grade corporate market by storm where "cash-rich" companies haven't issued a single bond YTD, was a factor in rising Treasury yields.

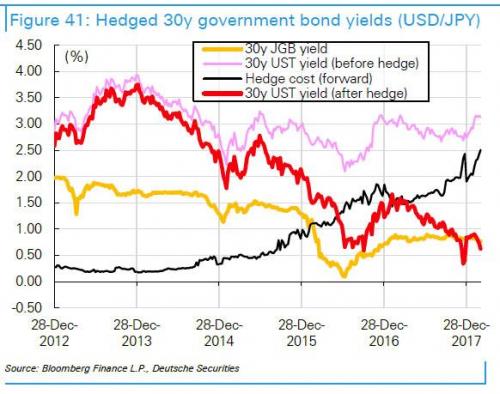

Furthermore, picking up on another previously covered topic, namely the recent surge in USD funding costs, Gundlach warned that the rising yields will continue as foreigners will be averse to purchasing U.S. Tsys because of hedging costs which have made the US 30Y Treasury the least economical of all govt bonds.

Still, the DoubleLine CEO said he has little conviction the 10Y will break hard above the 3% level:

"Maybe this level will hold on the 10-year. I’m not in that camp, but my conviction is low. My conviction on breaking above 3 is low. I don’t think you need conviction - let the market prove your opinion."

More curiously, unlike a growing chorus on Wall Street, and even the market itself where forward OIS curves have already inverted, Gundlach said that he does not think the yield curve will invert before the next recession. This likely goes to Gundlach's thesis, which he proposed in January, that in the next recession we won't see a bid for safety out of stocks and into bonds. In other words "we won't see a bond market rally."

If so, he is right: there would be no inversion; there would be just an epic cross-asset crash, that incidentally will blow up all risk-parity funds in the process.

Which leads us to the final two points.

First, Gundlach said he thinks that Fed chair Jerome Powell is "not going to bail out the market." Here he may be referring to what Zero Hedge first observed in January, when in the recently declassified 2012 FOMC transcripts, we found the following gem:

"[W]hen it is time for us to sell, or even to stop buying, the response could be quite strong; there is every reason to expect a strong response. So there are a couple of ways to look at it. It is about $1.2 trillion in sales; you take 60 months, you get about $20 billion a month. That is a very doable thing, it sounds like, in a market where the norm by the middle of next year is $80 billion a month. Another way to look at it, though, is that it’s not so much the sale, the duration; it’s also unloading our short volatility position."

Second, Gundlach said that the next big move will likely be in gold prices which have broken their downtrend line, and are on the verge of breaking out to the upside. "It’s getting almost exciting... something big is happening,” he said cryptically.

He then revealed his target, saying that based on classic chart reading, an "explosive, potential energy" of a huge "head-and-shoulders bottom" base was signaling a move of $1,000 in gold prices, and added that "Gold is maintaining an upward pattern above its rising 200-day moving average, which is extremely good."

Original source: Zero Hedge

Reproduction, in whole or in part, is authorized as long as it includes all the text hyperlinks and a link back to the original source.

The information contained in this article is for information purposes only and does not constitute investment advice or a recommendation to buy or sell.