Italy is unmanageable, just like the euro, as we wrote on March 8, right after the Italian general elections; we’ve just had confirmation of that. After the two winners (Luigi Di Maio, of the 5 Star Movement and Matteo Salvini, of the League) had finally come together on choosing a program and a Prime minister, after weeks of negotiations and stalling, the house of cards crumbled and there will be a need for new elections!

The stumbling block has been the euro – which is quite amazing, because it wasn’t part of the debate during the campaign, since neither party wanted to go back to the lira. But one cannot ignore the common currency, especially in Italy, where public debt has risen to 132% of GDP (the highest percentage after Greece) and where the banking sector is in shambles. The President of the republic, Sergio Mattarella, has refused the nomination of the euro-sceptic Paola Savona for Minister of the Economy, on which Salvini didn’t want to give. As a result, there will be no government at all and new elections will be held this summer or fall. Meanwhile, a “technical” Prime minister, Carlo Cottarelli, formerly with the IMF, will manage current affairs until then.

The President of the republic proclaimed, “I said no to someone who professes exiting the euro. It’s a question of respect for the savings of households”. Wow, the head of State is preoccupied with the savings of households... Mama mia! In fact, this will bring back the euro question in the midst of the next Italian elections, along with the public debt and the failing health of the banks. The common currency issue is coming back like a boomerang and it may bring with it the same sovereign debt crisis that the euro zone went through in 2010-2011 with Greece, Ireland, Portugal and Cyprus.

Furthermore, Spain is facing a political crisis with the indictment of several members of Prime minister Mariano Rajoy’s party for corruption, which increases the probability of early elections before the end of the year. A new sovereign debt crisis would no longer be a thing for “small” countries only, but a thing for Italy and Spain as well...

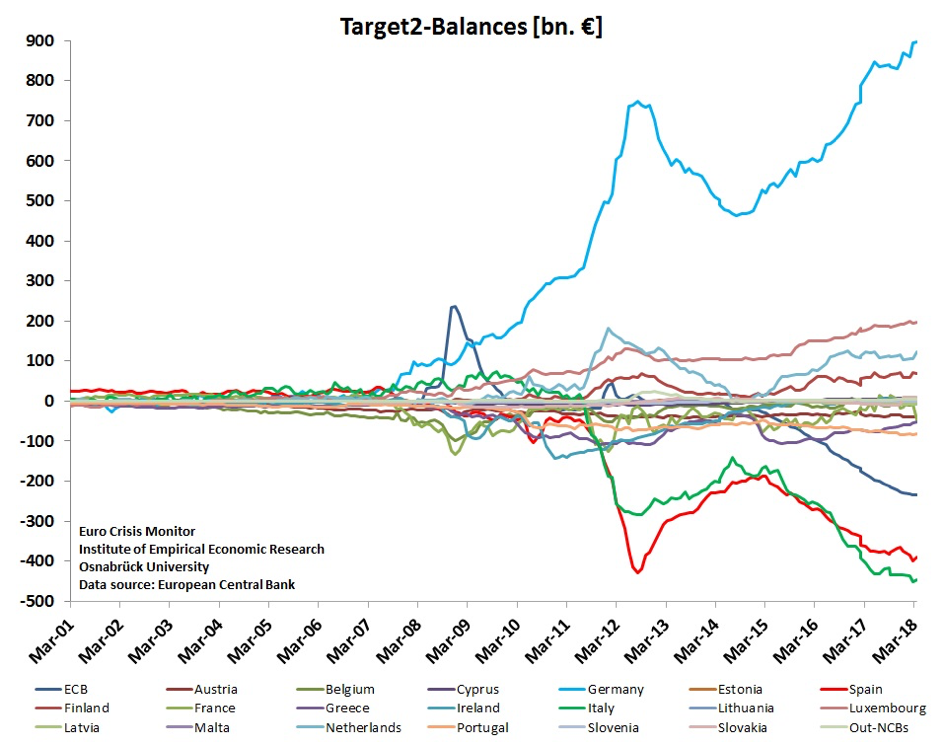

We’ve already seen interest rates tightening up in Italy these last few days, as well as in the southern countries, and in France also, with its banks very much implicated in the transalpine economy. We’re hearing talks of money transfers from Italy to Germany, as the banking system is less and less trustworthy – that will not help with the growing imbalance of Target2 payments, which tracks capital movements throughout the euro zone. Both Italy and Spain are plunging toward deficits (400 billion euro each) as Germany accumulates surpluses (close to 900 billion euro). Records that were reached in the last sovereign debt crisis are being shattered... savers are right to be worried – not only Italians, but all Europeans...

Reproduction, in whole or in part, is authorized as long as it includes all the text hyperlinks and a link back to the original source.

The information contained in this article is for information purposes only and does not constitute investment advice or a recommendation to buy or sell.