Are we witnessing a movement of European bank mergers? Rumors have been circulating for several years about a merger between Commerzbank and Deutsche Bank or with BNP Paribas, between Société Générale and Unicredit, but nothing has happened so far. But lately several mergers have taken place.

First of all, this summer, the Italian bank Intesa Sanpaolo absorbed its rival UBI Banca to form a group of 1.1 trillion assets, one of the largest in Europe. On September 18, in Spain, we witnessed the takeover of Bankia by CaixaBank to form the country's leading banking group, ahead of Santander, with a balance sheet total of 664 billion euros. Then, on October 5, again in Spain, we learned that Unicaja and Liberbank could merge, as both institutions had already started official discussions, but also that BBVA could buy Banco Sabadell. In France, the Crédit Agricole would consider an offer on the Italian Banco BPM. Then, rumors are spreading and accelerating, suggesting other announcements (merger of the Swiss UBS and Credit Suisse, BNP Paribas and Société Générale, etc.).

What are the underlying reasons for these connections? Better profitability? Not really. Let's recall, for example, that in 2012, Madrid had saved Bankia from bankruptcy by injecting 22 billion euros to prevent the collapse of a banking sector devastated by the bursting of the real estate bubble, a replica of the subprime boom in the United States in 2008. Profitability in retail banking in Europe has virtually vanished because of zero interest rates. The European Central Bank (ECB) has just published its latest statistics: the return on equity (RoE) of EU banks in June was only 0.01%, and 1% in the first quarter. Let's note, for example, that the Sino-British banking giant HSBC had bought Crédit Commercial de France (CCF) in 2000 for 11 billion euros, that it was trying to sell it for a significant euro at the beginning of the year (see our article), but that after the coronavirus crisis, it will have to pay 500 million euros in cash to the buyer, the American fund Cerberus!

No, these mergers have one main objective: to become big enough and indispensable so that in the event of a serious crisis, the government and the ECB would be obliged to come to their rescue. The principle of 'too big to fail' becomes a management rule. Secondly, it is also a question of reducing competitive pressure in order to increase fees. In both cases, the prospects for the basic customer are not very encouraging, because if there is a risk of bankruptcy, he is not certain to recover all his assets (under the BRRD), and his bank will cost him more.

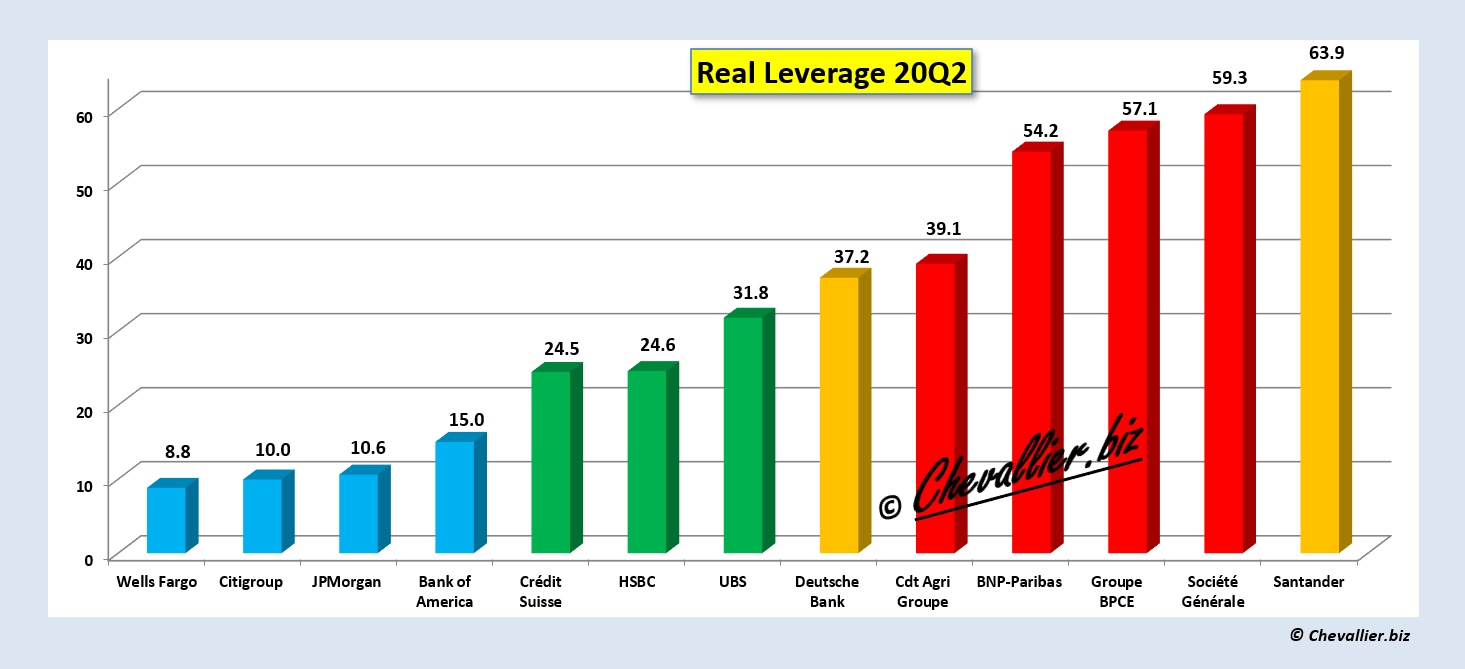

Rather than allowing or encouraging such mergers, the authorities of the countries concerned at both government and regulatory levels should instead require banks to rebuild their capital base. Since the 2008 crisis, they have not really made any real effort to increase them, unlike the American banks. While the leverage of the latter is around 1/10, that of European banks often exceeds 1/30. Merging only postpones the problems, whereas it would be imperative to make the large European banks more resilient.

Reproduction, in whole or in part, is authorized as long as it includes all the text hyperlinks and a link back to the original source.

The information contained in this article is for information purposes only and does not constitute investment advice or a recommendation to buy or sell.