In an investment world of instant gratification and Fed Intervention, when short term trading and speculation is the norm, real values are forgotten.

Confucius understood the value of long term thinking and thus real values:

If you think in terms of a year, plant a seed, if in terms of ten years, plant trees, if in terms of 100 years or more – teach the people. – Confucius

In the 2000s, fortunes have been created which are of magnitudes that are unfathomable.

No speculator or investor has had to plan his investments in this century on a 100 year basis as Confucius suggested. Instead, wealth beyond anyone’s wildest dreams have been created in a couple of decades.

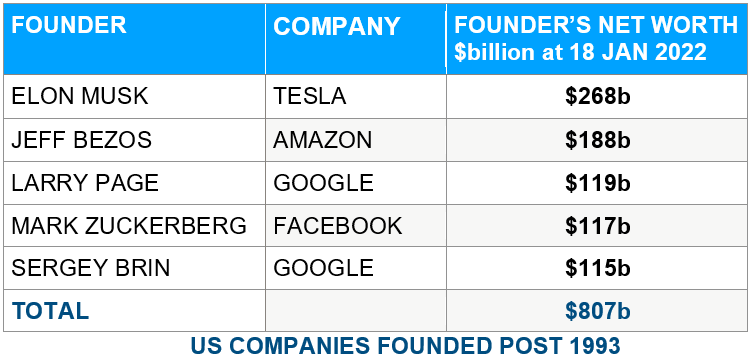

Just take some of the wealthiest Americans today. Pre 1994, the following multi-billionaires hadn’t even started their businesses:

US COMPANIES FOUNDED POST 1993

In 1993, before any of the above companies existed, the richest American was Warren Buffett who then had a $8 billion fortune. In 2022 Buffett’s net worth is $117 billion.

So in under 30 years, the richest American’s wealth (Musk) is 33X greater than the wealthiest American 30 years earlier.

THE NEW ROBBER BARONS WITH MEGA WEALTH BEYOND BELIEF

The total wealth of the 5 nouveau-riche Americans above exceeds the GDP of countries like Switzerland, Holland, Sweden, and Poland. It is beyond belief that the founders of 5 companies that have been in existence less than 30 years have amassed more wealth than the GDP of countries some of which are over 1,000 years old.

Yes, I know it is all new technology companies in different forms. But take a company like Google which basically offers a more sophisticated yellow pages service on a global scale. The two founders of Google, Page and Brin have a combined wealth of $234 billion based on a company that produces no tangible products. This is a totally new phenomenon in the last few decades. Founders of companies worth trillions of dollars which are primarily software or technology based have emerged as the new Robber Barons from a century earlier.

Like all new and innovative industries, these technology companies will meet the same destiny as most leading industries throughout history. They will be overtaken by new companies and new technology. Also, valuations of many of these companies will decline substantially. Of the original 12 companies in the Dow Jones Industrial Average, NONE remain today. History will most certainly repeat itself over the next 100 years.

END OF AN ECONOMIC ERA

As I have pointed out numerous times, we are now at the end of a major economic era.

Typical for the end of a cycle are bubbles in many asset markets and commodities. This is exactly what we have seen in this century with historical overvaluations of stock, bond, and property values.

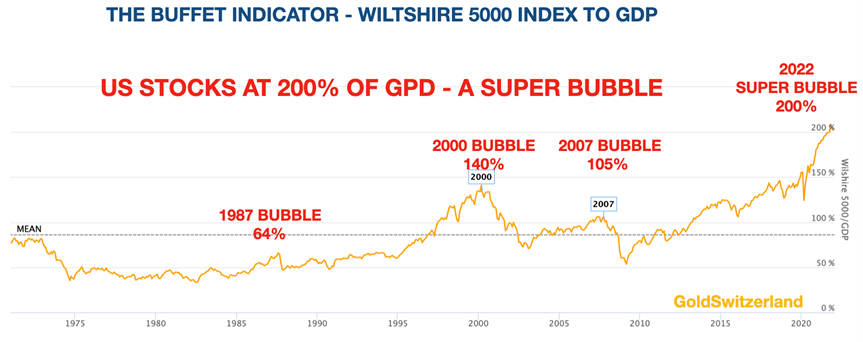

The Buffett Indicator now shows US stocks at over 200% above GDP. This is an epic overvaluation and massively above the 2000 high of 140%. See graph below.

GRANTHAM – “A SUPER BUBBLE”

As Jeremy Grantham says, this US Super Bubble is shockingly overpriced. It will not just return to the mean but will go beyond trend on the downside just as it has on the upside.

What we must remember is that Super Bubbles end with a shocking decline in both price and time. What few investors will fathom is that in the next decline, buying the dips will fail.

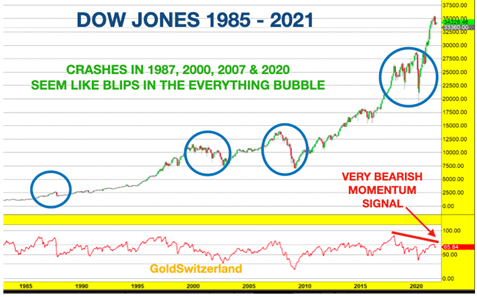

During my professional life all Western markets have recovered from major falls. This was the case in after the corrections starting in 1973 (not shown), 1987, 2000, 2007 and 2020. Virtually every fall during those five bear markets/corrections look like a blip on the chart today.

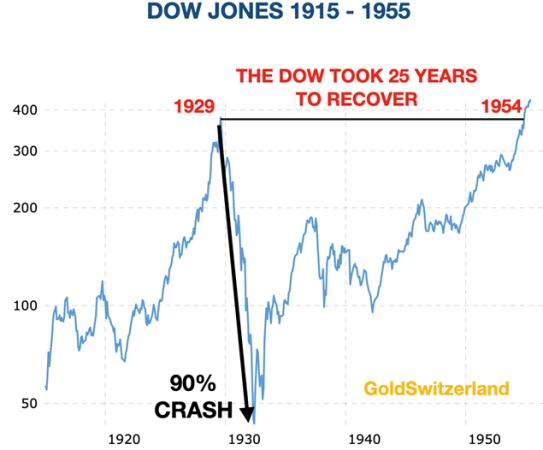

But this time it will be different. Just like the Dow in 1929 and the Nikkei in 1989.

The Dow fell 90% between 1929 and 1932. It then took 25 years in nominal terms, until 1954, to recover to the 1929 high.

The Nikkei peaked in 1989 at 39,000 and subsequently fell by 89%. Today, 33 years later, the Nikkei has still not reached the 1989 peak in spite of massive money printing and debasement of the currency.

BUYING THE DIP WILL FAIL THIS TIME

So any investor who has the idea of buying the dips, when the Super Bubble soon bursts, is going to get the shock of a life time as he trades in and out of super volatile market which relentlessly turns down after every rally and reaches new lows.

The average investor will continue to expect that the Fed Put (Bernanke, Yellen & Powell) will work as it have done in the past. The Fed Put in simple terms means that the Fed saves the stock market by printing enough money and manipulating interest rates so that stocks quickly recover.

Let’s just remind ourselves that saving the stock market has never been one of the Fed’s official mandates. (For information the mandates are stable/low inflation and full employment.) But the Fed is of course controlled by private bankers in whose interest lies an eternally rising stock market for their own benefit.

But sadly this time the Fed Put will not work, although most dip buyers will not realise this until it is much too late. And so they will ride the coming super bear until they have lost most of their money in real terms.

SUPER BUBBLES CAN ALWAYS GET BIGGER

Remember that a Super Bubble will most of the time extend further than anyone can imagine, so timing the exact top is a mug’s game. Looking at the Nasdaq and the Russel 2000, it seems that the top is already in.

The Nasdaq had gone up a massive 16X between the 2009 top and the peak in November 2021. There is nothing stopping this Super Bubble getting slightly bigger. But it serves no purpose whatsoever to squeeze the last drop out of a market which is up 150X since 1985.

No one goes bankrupt by taking profit too early. But many will lose everything by holding on until the top and then riding the market all the way down.

UBIQUITOUS RISK – IN STOCKS, BONDS, PROPERTY & DOLLAR

But the stock market is just one of the many danger signs facing the investment world currently.

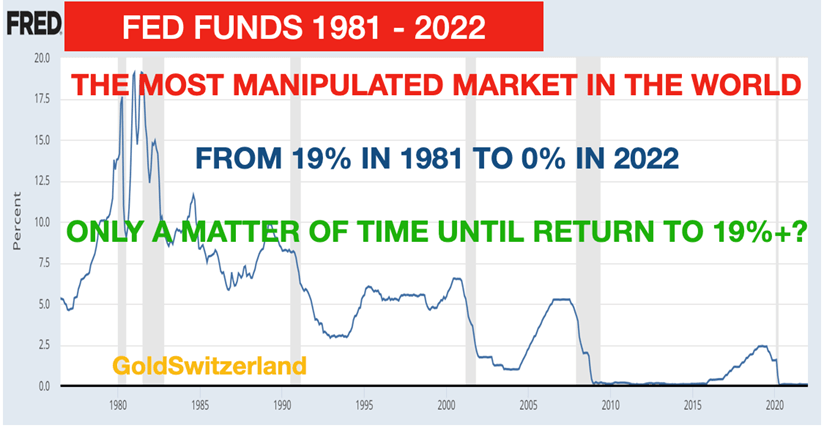

The bond market is equally dangerous and a bubble as great as the stock market. The Federal Funds rate peaked in 1981 at 19% and has been in a 40 year downtrend. Since the Great Financial Crisis in 2008, Fed Funds have been around 0%.

Fed Wizards – The Mega Manipulators

In a free market, without manipulation, such a strong demand for money would have raised the cost of borrowing to the levels in 1980-81 i.e. near 20%. Instead, the Fed Wizards are performing their hocus pocus with fake money and fake rates.

Without their Wizardry, it would have been impossible for the Fed and US government to create $10s of trillions at ZERO cost.

But in my view, their game is now up. For the last few years, I have expressed that the Fed will lose control of the long end of the bond market and that is exactly what is happening with the 10 year approaching 2%. Next phase is that the long rates will pull the short rates up and rates will rise faster than the Fed would like.

That will make tapering difficult or impossible, especially since budget deficits will continue to grow in addition to major liquidity pressures in the financial system.

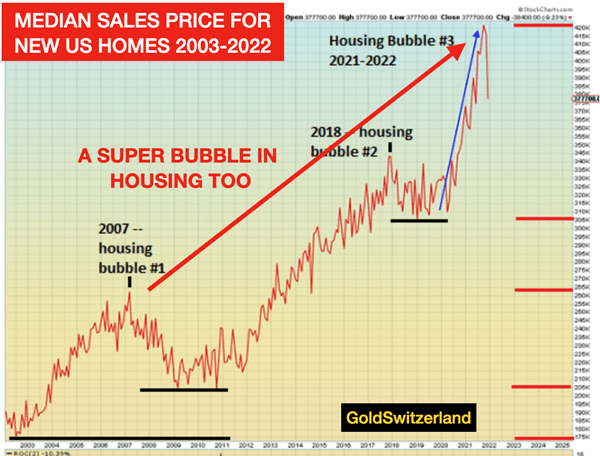

Add to that a US housing bubble which is looking more dangerous than during the sub-prime crisis in 2006-2008. If we just look at the median sales price for new homes, they are up 150% since 2007.

With higher house prices, mortgage loans are also growing and are now $17.6 trillion, which is 20% above the 2008 peak. It is a virtual certainty that with historically low interest rates, the quality of mortgage loans as well as the leverage is as unsound as in 2006-2008. Therefore, yet another problem in the mortgage debt market is very likely.

Another problem area for the US is the artificially strong US dollar. Since the closing of the gold window in 1971, the dollar has declined rapidly. Against the strong Swiss franc for example, the dollar has fallen 80% since 1971. It now looks like the dollar has just turned down again and I would expect a 40-50% fall against the Swiss franc in the next few years.

So the picture clearly doesn’t look good for a US economy which is now on the brink of collapse.

To summarise, starting in 2022, we will see in the next few years falls of 75-95% in US stocks (in real terms), a collapsing bond market and property market, a much weaker dollar and high inflation.

Also, debt will continue to increase until one day the whole debt market collapses, led by the $2 quadrillion derivative market.

So what will be the solution?

Well, the same one that has not just maintained its intrinsic value for 5,000 years and been the best asset to hold in periods of crisis in order to preserve wealth.

Obviously, I am talking about physical gold. Since the gold window was closed by Nixon in 1971, gold is up 52X.

PHYSICAL GOLD – ULTIMATE INSURANCE

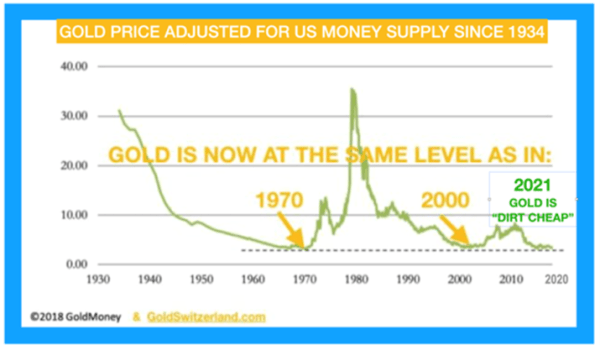

Gold moved up for 12 years from $250 in 1999 to $1,920 in 2011. We are just seeing the end 11 year consolidation that is on the verge of breaking out to much higher highs. So there is not much time left to buy gold and silver at these bargain prices.

As I have pointed out in most of my articles, gold is now as unloved and undervalued as it was in 1971 at $35 and in 2000 at $290. Therefore, gold will not only protect investors’ wealth, but also enhance it considerably.

Finally, let us leave the last word to Confucius again with the addition of just two words:

If you think in terms of a year, plant a seed, if in terms of ten years, plant trees, if in terms of 100 years or more – teach the people about GOLD – Confucius

Original source: Matterhorn - GoldSwitzerland

Reproduction, in whole or in part, is authorized as long as it includes all the text hyperlinks and a link back to the original source.

The information contained in this article is for information purposes only and does not constitute investment advice or a recommendation to buy or sell.