In my monthly bulletin for Goldbroker clients, I take another look at the continuing decline in LBMA silver inventories.

I explain that, unlike 2021, “physical demand is not coming from speculators: countries such as India could quickly deplete London's physical metal reserves, especially if market players try to limit their losses by stepping up sales to curb rising prices.”

What is the current state of silver inventories?

On the COMEX, the replenishment of inventories in the 'Registered' category, which began a year ago, seems to be stalling. The problem is that Open Interest remains very weak. In other words, a resumption of investor speculation on silver could occur at insufficient inventory levels, putting pressure on medium-term reserves:

The other delivery market, Shanghai, is no better off. Although replenishment has prevented inventories from falling this summer, they remain very low:

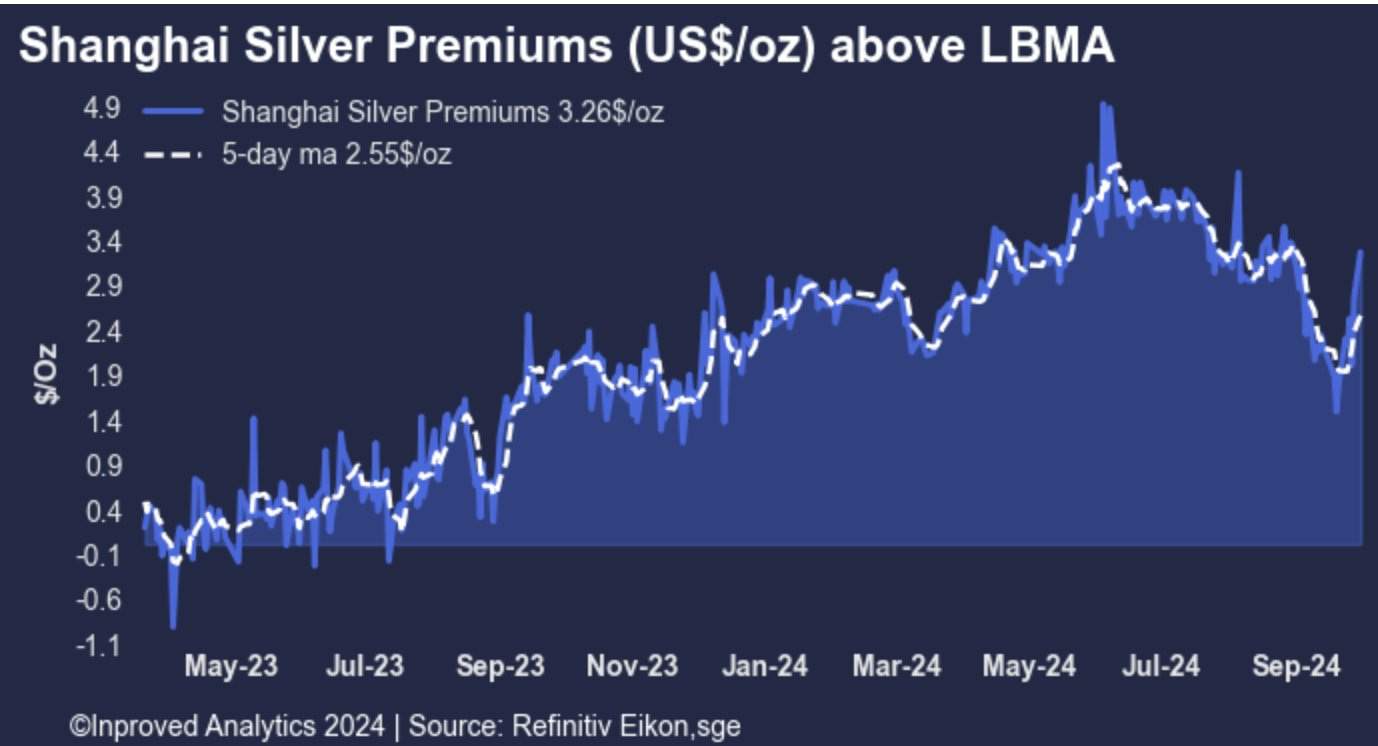

All the more so as silver premiums are on the rise in Shanghai:

For the past two years, every time this premium has exceeded $2, silver prices have risen again:

Over the past year, it has become increasingly clear that the physical market is gradually taking over from the paper market in determining the spot price. We are witnessing a similar phenomenon in the gold market: physical demand, often invisible to Western speculators, is dictating the metal's price. Gold's rise was not anticipated and remains misunderstood in the West, as this time virtually no investors, whether institutional or individual, have participated. The silver market is likely to follow the same trajectory. The weakness of Open Interest is a telling sign: interest in silver trading is virtually non-existent. Yet silver is already reaching record levels, sustained exclusively by physical demand that is invisible to Western investors.

This threat does not seem to be worrying commercial traders who, as in the case of the gold market, have opted to strengthen their short silver positions in order to stem the rise in prices and protect their short positions.

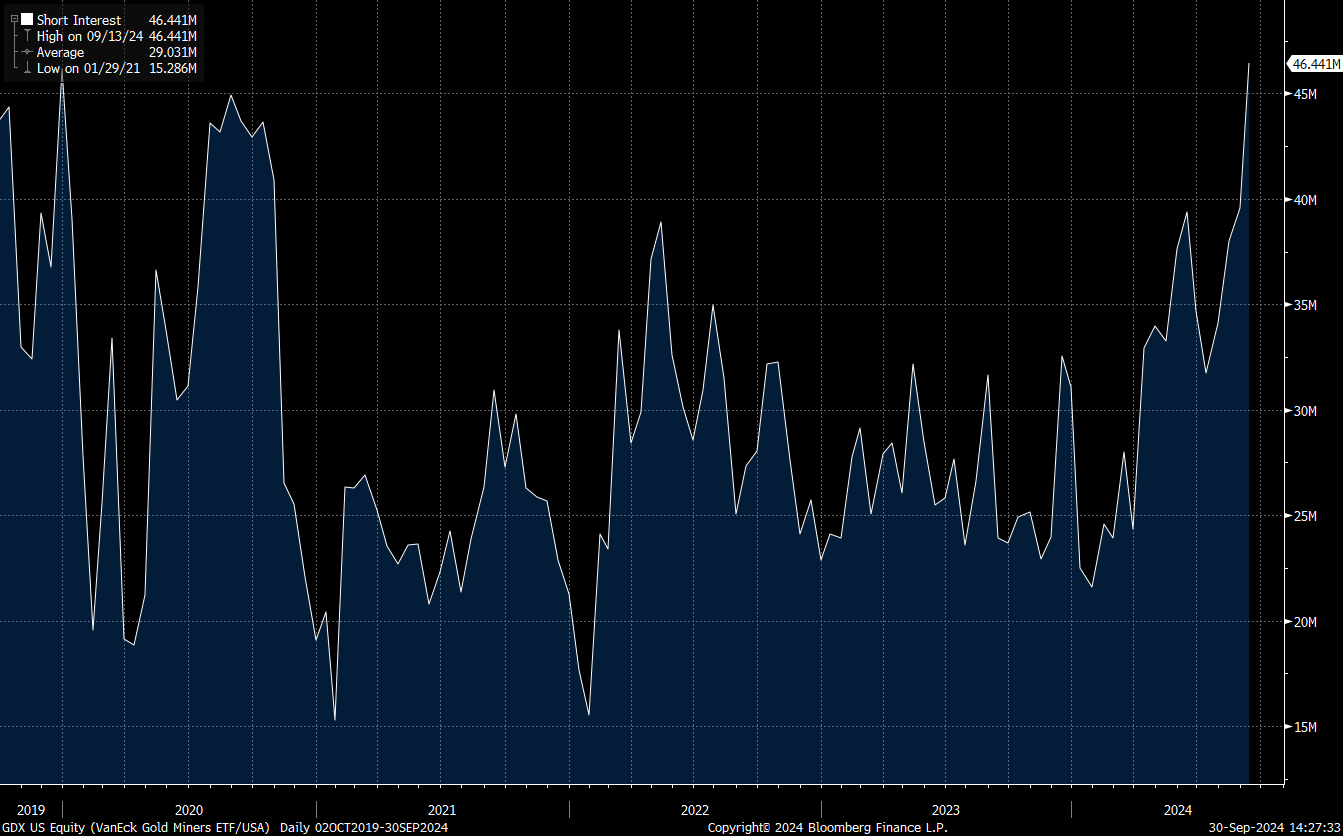

Short positions in mining stocks also increased. At the end of September, the number of short positions on the GDX index reached a 4-year high:

This traditionally heralds an offensive on mining and silver in the weeks ahead. If so, COMEX inventories are likely to melt even faster than expected!

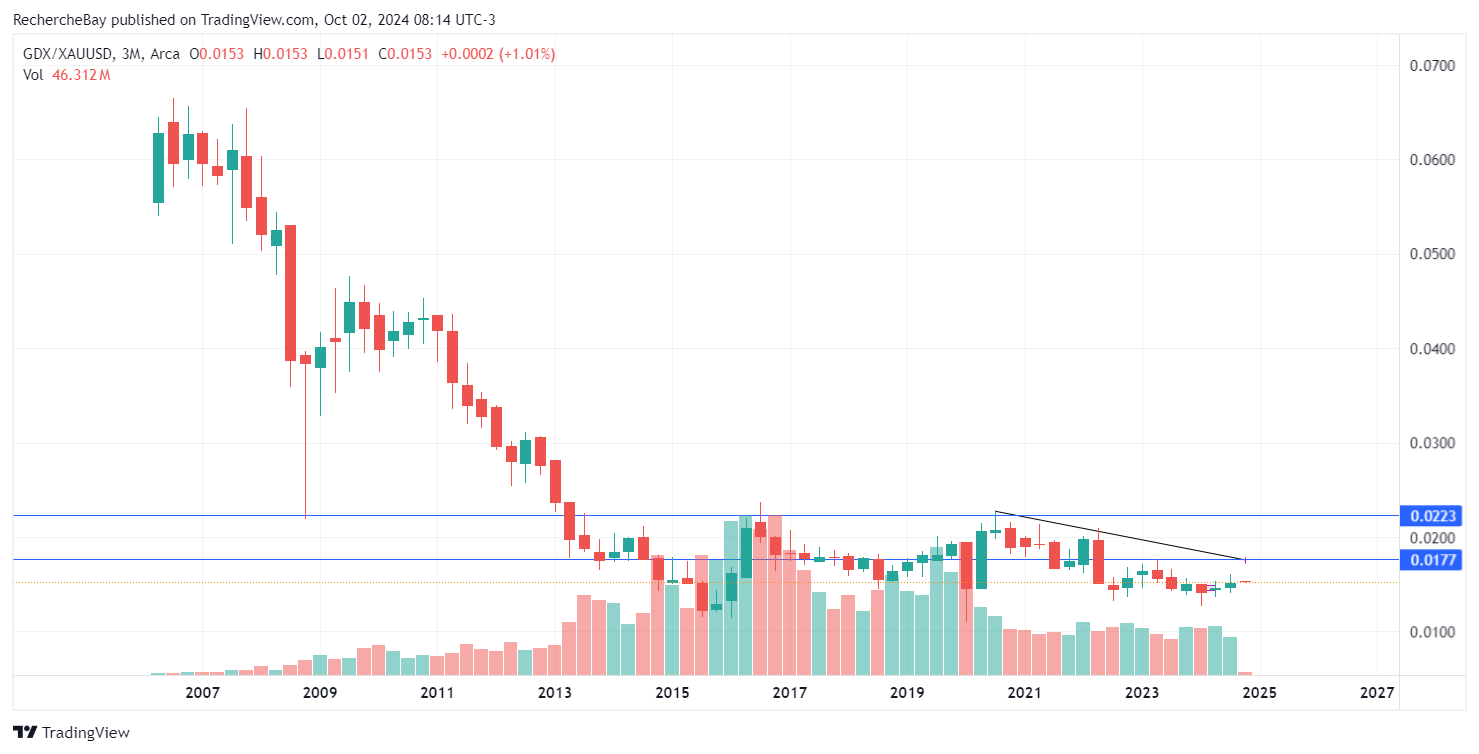

This raid would come at a time when miners have never been so cheap relative to gold. The GDX/gold quarterly chart is still stuck at its lows:

This poorly-timed selling pressure represents an opportunity for long-term investors, who are anticipating an increase in mining margins this quarter: oil is down, gold is up, and announced cash flows could well exceed forecasts.

Attempting to control an underlying trend by manipulating the paper markets works in the short term, but amplifying this type of control ends up reinforcing the underlying trend.

This is precisely what could happen to mining and silver over the coming weeks.

Physical demand represents a major risk for bullion banks' short positions on the COMEX.

Similarly, rising mining margins pose a major threat to short sellers of mining indices.

The gold price, for its part, remains at a record high after recording a double monthly and quarterly closing record.

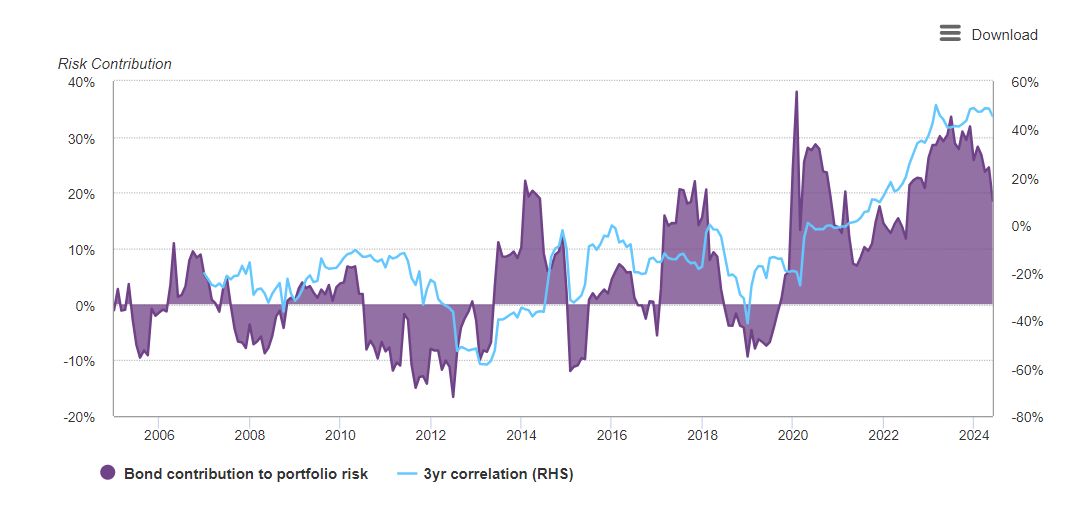

In my September article, I wrote that the World Gold Council recently published an article explaining why, by 2024, gold is set to become the ultimate defensive asset, replacing bond assets.

I highlighted the main chart of this study, which illustrated the risk contribution of the two asset classes, equities and bonds:

The correlation between equities and bonds has become positive. Gold is now the ultimate protective asset in Swiss portfolios, as Swiss bonds no longer play this role.

It is probably this new context that led UBS to publish a new report on gold this week. In this report, UBS raises its price target for gold to $2,750 for year-end and $2,850 for mid-2025.

However, the most significant aspect of this UBS publication concerns the allocation advice given by the bank: “UBS reiterate our recommendation for a diversified USD-denominated portfolio to include a 5% allocation to gold as a broad portfolio hedge.”

This is the first time a major European bank has issued such a warning.

This is all the more important given that the average portfolio allocation to gold is still less than 1%!

As I meet with asset managers in Switzerland, I notice a general lack of exposure to physical gold. For several years now, only a few family offices have been protecting their portfolios with physical gold. Their clients sleep peacefully, much better than those stuck in bond products issued by troubled governments. For the former, physical gold offers a guarantee against counterparty risk, ensuring the security of their assets. For the latter, their capital is tied to the promise of a paper security, whose return on investment is becoming increasingly uncertain.

Gradually, awareness of the value of gold is growing in Switzerland.

Gold has finally broken through resistance in Swiss francs, setting a new monthly closing record in September:

Gold in Swiss francs is in a breakout phase and has just crossed a third milestone since its 2014 low. In ten years, the price of gold in CHF has doubled: its performance against one of the world's strongest currencies is remarkable.

Reproduction, in whole or in part, is authorized as long as it includes all the text hyperlinks and a link back to the original source.

The information contained in this article is for information purposes only and does not constitute investment advice or a recommendation to buy or sell.