The 2024 In Gold We Trust report entitled "The New Gold Playbook" has been published! Over 400 pages of research, with topics ranging from gold, macro, and inflation to mining and the price of beer in gold. This is the gold standard of all gold studies.

Here are the 10 key points you need to know :

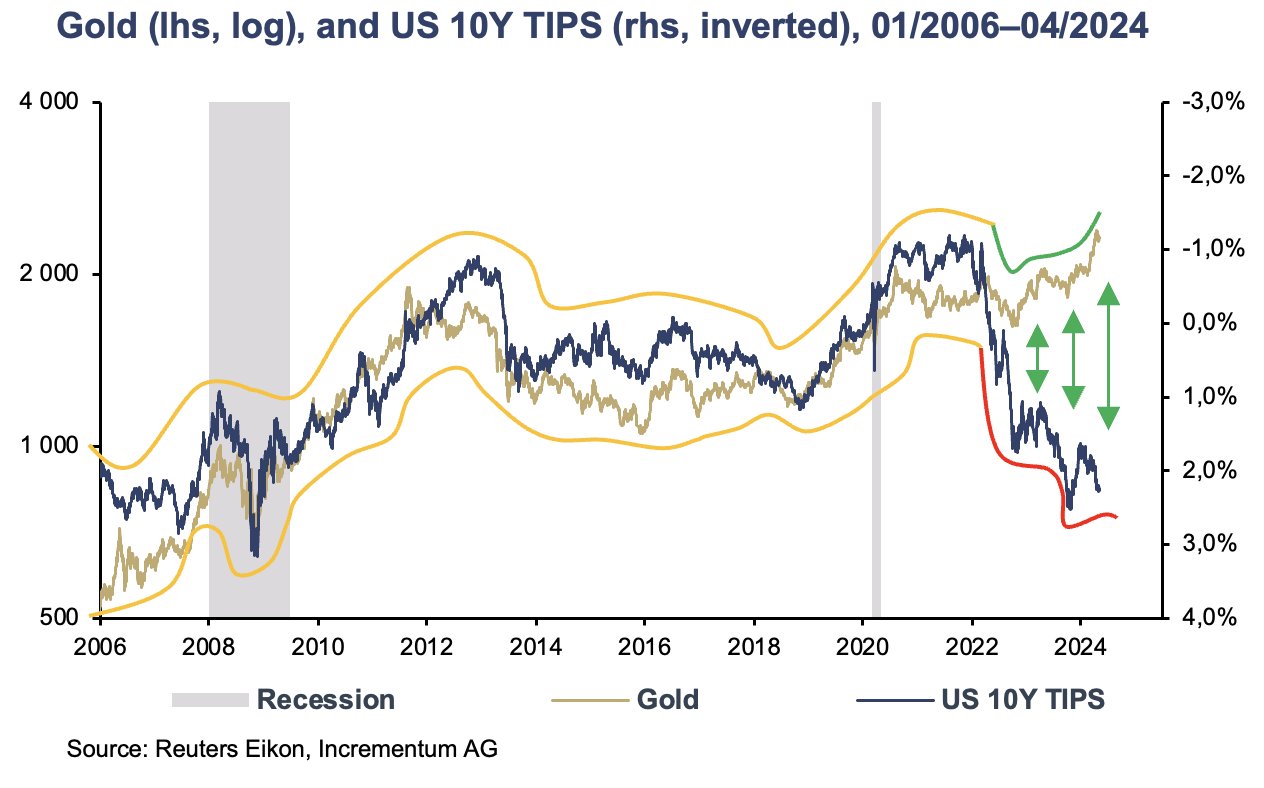

1. The high inverse correlation between US real yields and the gold price is history (for now). Despite the rise in real yields, the rise in the gold price could not be halted.

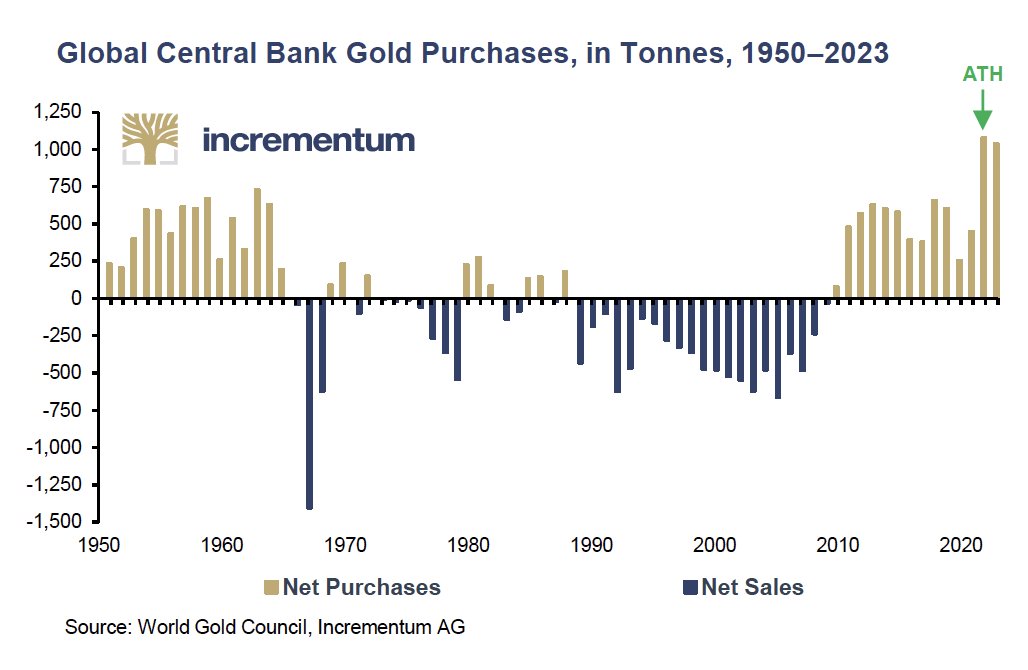

2. Central banks are a decisive factor in the demand for gold: Demand from these institutions is not very price-sensitive. Central banks are likely to have put a floor under the gold price.

3. The weaponization of fiat money has lasting consequences: The confiscation of Russian reserves and assets of Russian oligarchs in 2022 was a wake-up call for numerous states, as well as wealthy private individuals from the Gulf states, Russia, and China. (Luxury) real estate in London, New York or Vancouver has always been the preferred destination for savings from emerging markets, but this has changed in 2022.

4. Safe-haven assets are becoming scarce: The list of liquid safe-haven assets is getting shorter, and new and old safe-haven assets are gaining in importance.

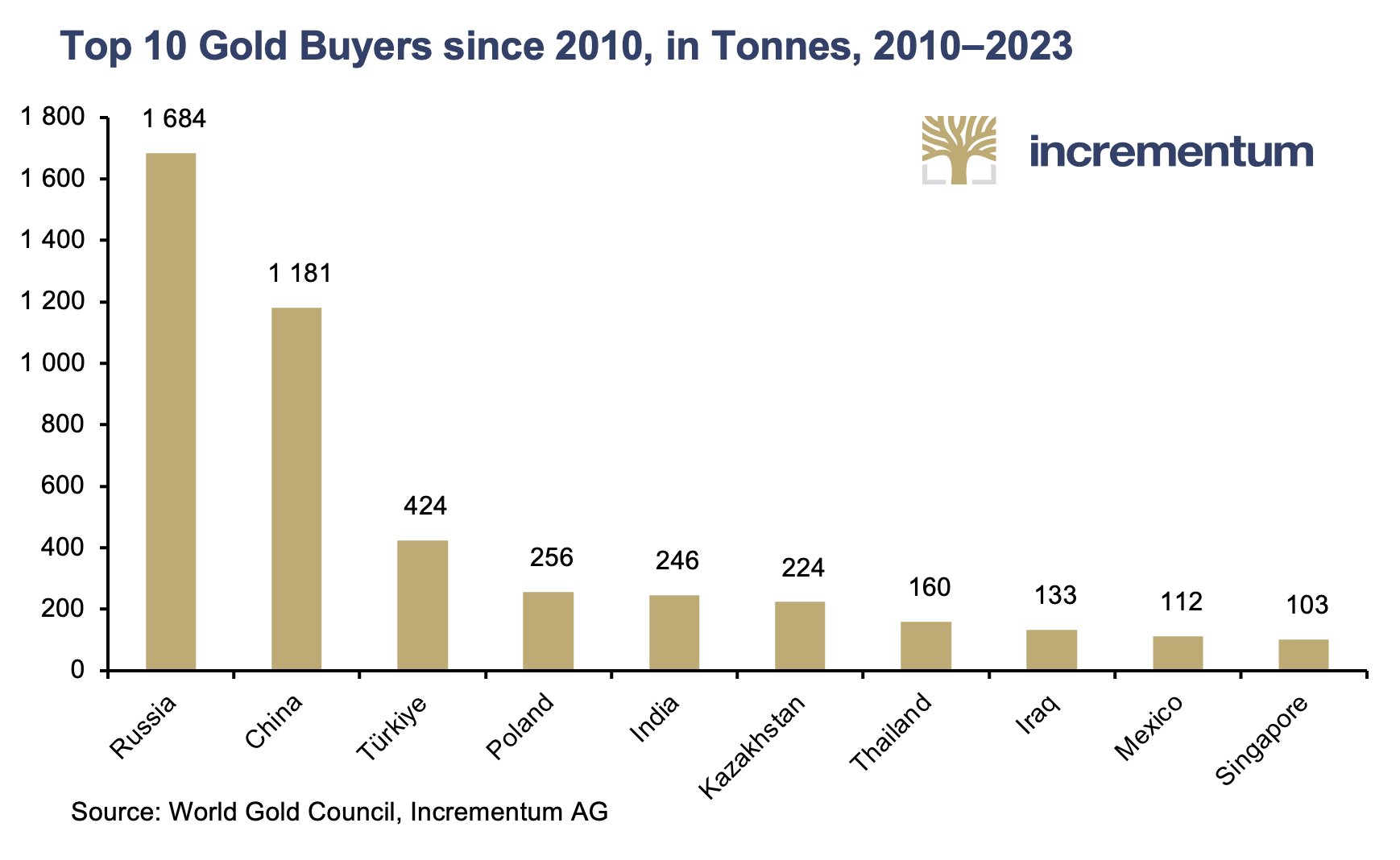

5. In contrast to the gold drain in the US in the 1960s, emerging markets are now experiencing a gold gain. China is playing a leading role in this respect but is no longer alone. The Western financial investor is no longer the marginal buyer or seller of gold. The pricing power of the gold market is increasingly shifting to the East.

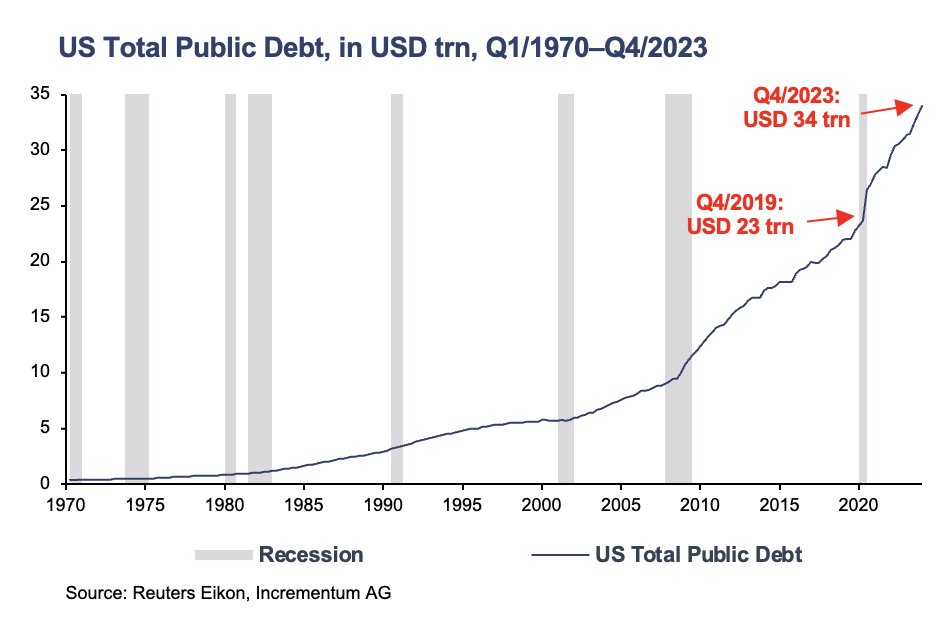

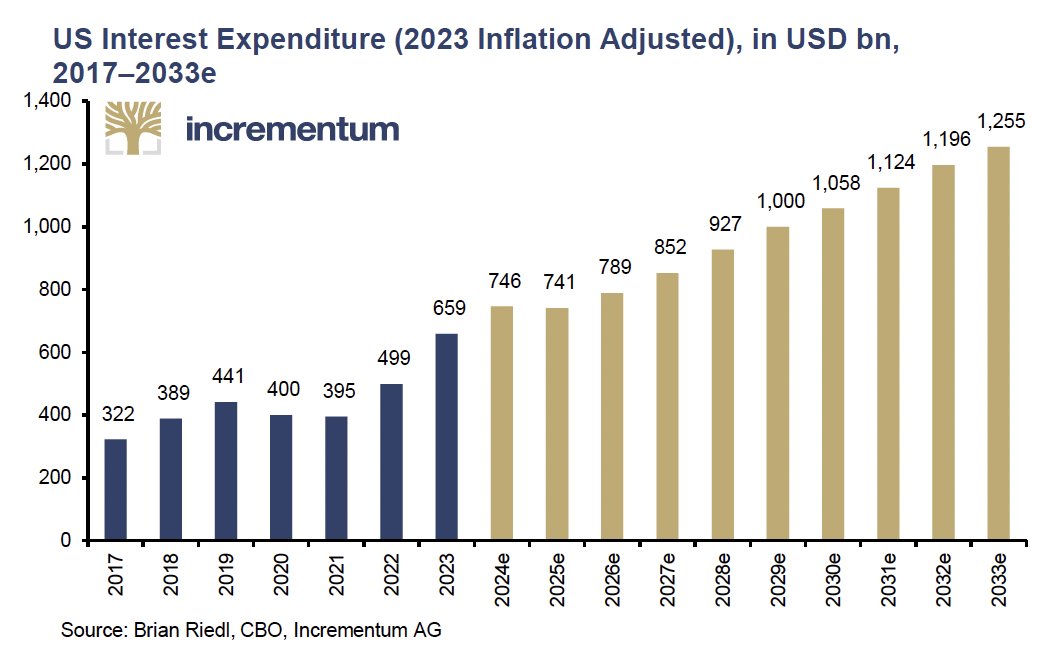

6. Monetary climate change: Fiscal largesse has seriously jeopardized the debt sustainability of Western countries. The explosion of the interest burden is a harbinger of the limits of debt sustainability.

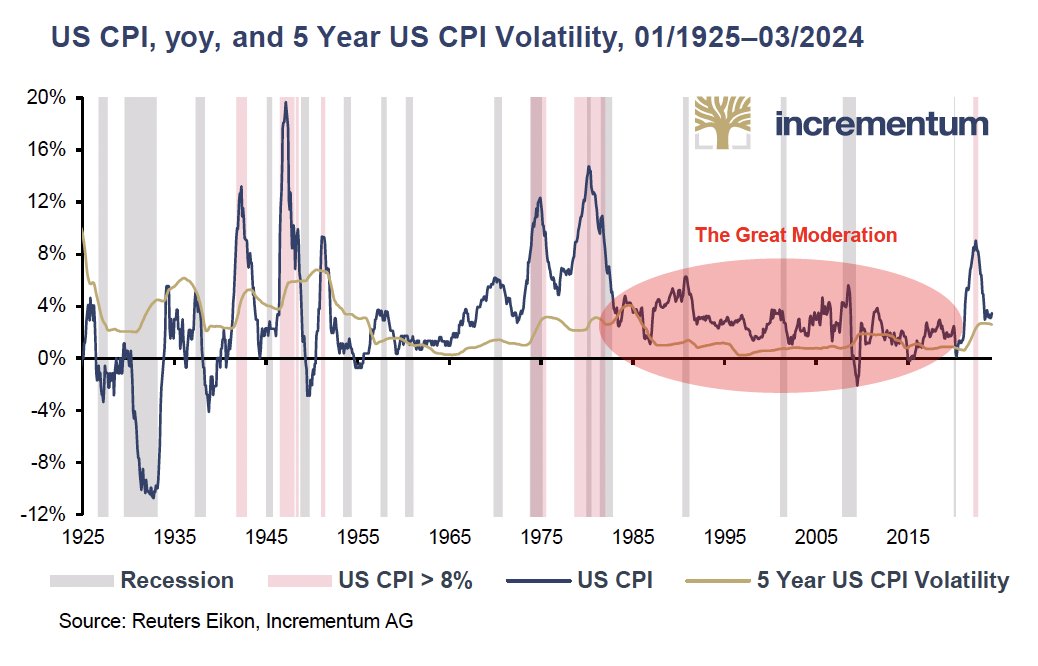

7. The new playbook in the context of stagflation 2.0: The Great Moderation is over. Periodic supply shocks will cause additional fluctuations in inflation.

8. The end of the 60/40 portfolio: A positive correlation between equities and bonds, as in the case of structurally higher inflation rates, means that bonds offer no protection when growth slows.

9. The central bankers’ new playbook: The holy grail of the 2% inflation target is no longer sacrosanct. Even before the mark has been sustainably reached again, Western central banks are openly talking about a change of course to a less restrictive monetary policy.

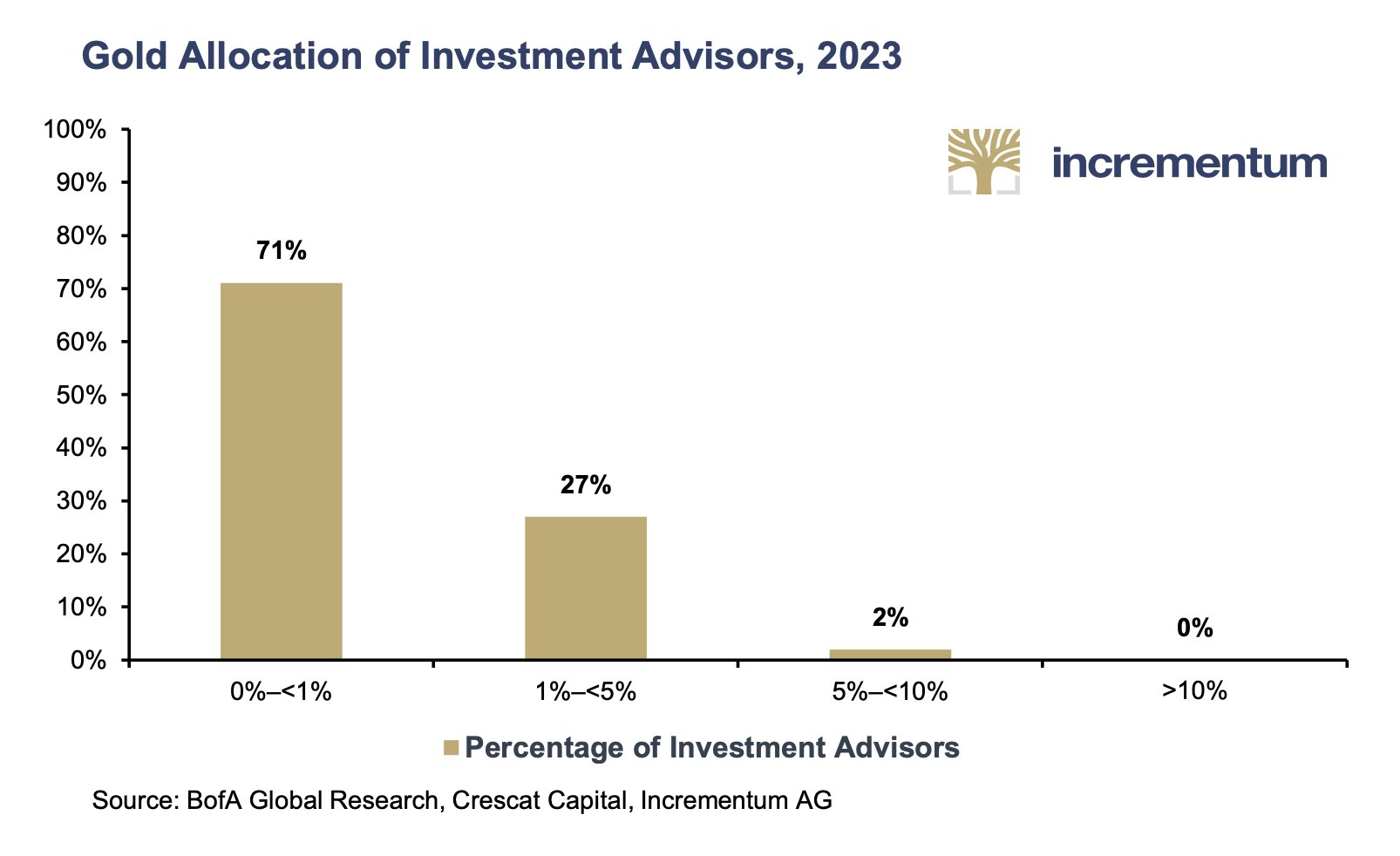

10. The low affinity for gold among large sections of the investment community : 71% of US advisors have little to no gold allocation, i.e. it is less than 1% of their portfolio. We also see a similar lack of interest in gold mining stocks, which have largely lost the trust of investors in view of their disappointing performance.

Reproduction, in whole or in part, is authorized as long as it includes all the text hyperlinks and a link back to the original source.

The information contained in this article is for information purposes only and does not constitute investment advice or a recommendation to buy or sell.