For several weeks now, U.S. stock indices have shown remarkable resilience. Despite a major energy crisis, growing geopolitical tensions, rising sovereign bond yields, and an increasingly unstable macroeconomic environment, equity markets remain near their highs.

At first glance, this resilience could be interpreted as a sign of confidence. However, when you look beneath the surface, the message sent by the market is much more ambiguous.

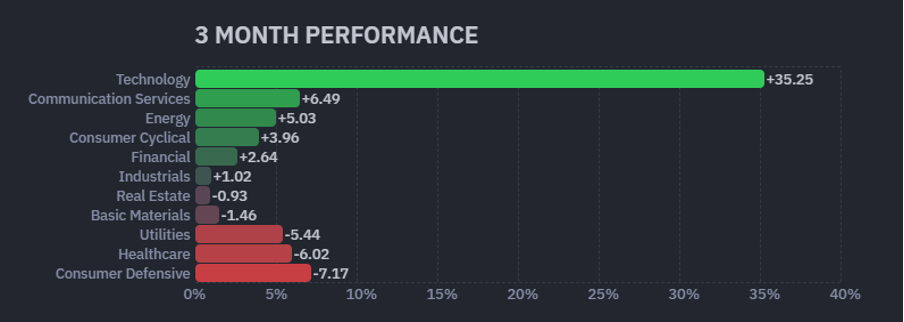

Sector performance figures for the past three months are particularly revealing:

The technology sector is up more than 35%, far outpacing all other sectors. In contrast, basic materials are down, utilities are underperforming significantly, defensive consumer goods are being shunned, and even the energy sector — despite the most significant global oil disruption in decades — is struggling to attract capital inflows.

This divergence warrants closer examination.

Because a market that believes in a sustained acceleration of global growth does not normally behave this way.

In a true economic re-acceleration cycle, capital generally flows toward the sectors most directly exposed to real economic activity: industrials, energy, materials, banks, and infrastructure. These are the sectors that benefit first from increased investment, physical demand, and credit growth.

Yet this is not what we are seeing today.

Banks continue to send signals of weakness. Basic materials remain unable to take the lead. Mining stocks are significantly underperforming despite gradually improving fundamentals. As for the energy sector, it is barely reacting even as tensions in the physical oil markets reach levels rarely seen before.

In other words, the market isn't really buying the growth narrative.

It's buying into something else.

What it is buying today is essentially artificial intelligence.

The rise in U.S. indices is increasingly driven by an extremely small group of companies: Alphabet, Nvidia, Microsoft, Meta, Amazon, Broadcom, and a few other stocks directly linked to the AI theme. Their weight is now so significant that they alone are capable of masking the weakness of much of the rest of the market.

The S&P 500 thus gives the impression of a robust market, while actual participation remains surprisingly limited.

This concentration is not only fundamental; it is also mechanical.

For several weeks now, the markets have been operating under an extremely unusual volatility regime. Systematic strategies, option-related flows, and dealer positioning continue to cushion a large portion of the corrections. Every significant pullback triggers buying that limits the damage in the short term.

In this context, investors naturally favor the most liquid assets and those best able to absorb massive flows. Tech megacaps thus become a somewhat unconventional safe haven.

In times of uncertainty, capital no longer seeks refuge in traditional defensive sectors. Instead, it concentrates on the most liquid tech stocks.

This situation creates an illusion of strength.

Bitcoin’s behavior, moreover, sheds further light on the true nature of current market flows. If the rise in tech megacap stocks truly reflected a widespread return of risk appetite, cryptocurrencies would logically be part of the trend. Yet the opposite is happening. Bitcoin does not support the theory of a market driven by a uniform wave of speculation. On the contrary, it signals growing pressure on liquidity.

Two recent events are particularly telling. The first concerns the U.S. Treasury’s crackdown on Iran’s crypto ecosystem. Scott Bessent announced that the United States had now seized nearly $1 billion in digital assets linked to Iran and sanctioned several major platforms used to circumvent international sanctions. For the first time on this scale, the market is rediscovering that stablecoins do not necessarily constitute a monetary system independent of governments but remain exposed to political, regulatory, and geopolitical risks. Part of the trust premium associated with the crypto universe has been called into question.

The second event is likely even more significant. Strategy (formerly MicroStrategy), a true symbol of the “never sell” mantra, announced its first bitcoin sale in several years. Admittedly, the amount sold is insignificant compared to the more than 843,000 bitcoins held by the group. But the amount matters less than the signal it sends. For years, Michael Saylor embodied the idea that a major institutional holder would never sell its bitcoins. That assumption has just vanished. Strategy has now demonstrated that its reserves can be tapped to meet financing needs or dividend payouts.

The market immediately got the message. The subsequent price drop isn’t linked to the sale of a few dozen bitcoins. It reflects the undermining of a fundamental psychological pillar. When the market’s most iconic marginal buyer ceases to be a permanent buyer, the perception of liquidity changes instantly.

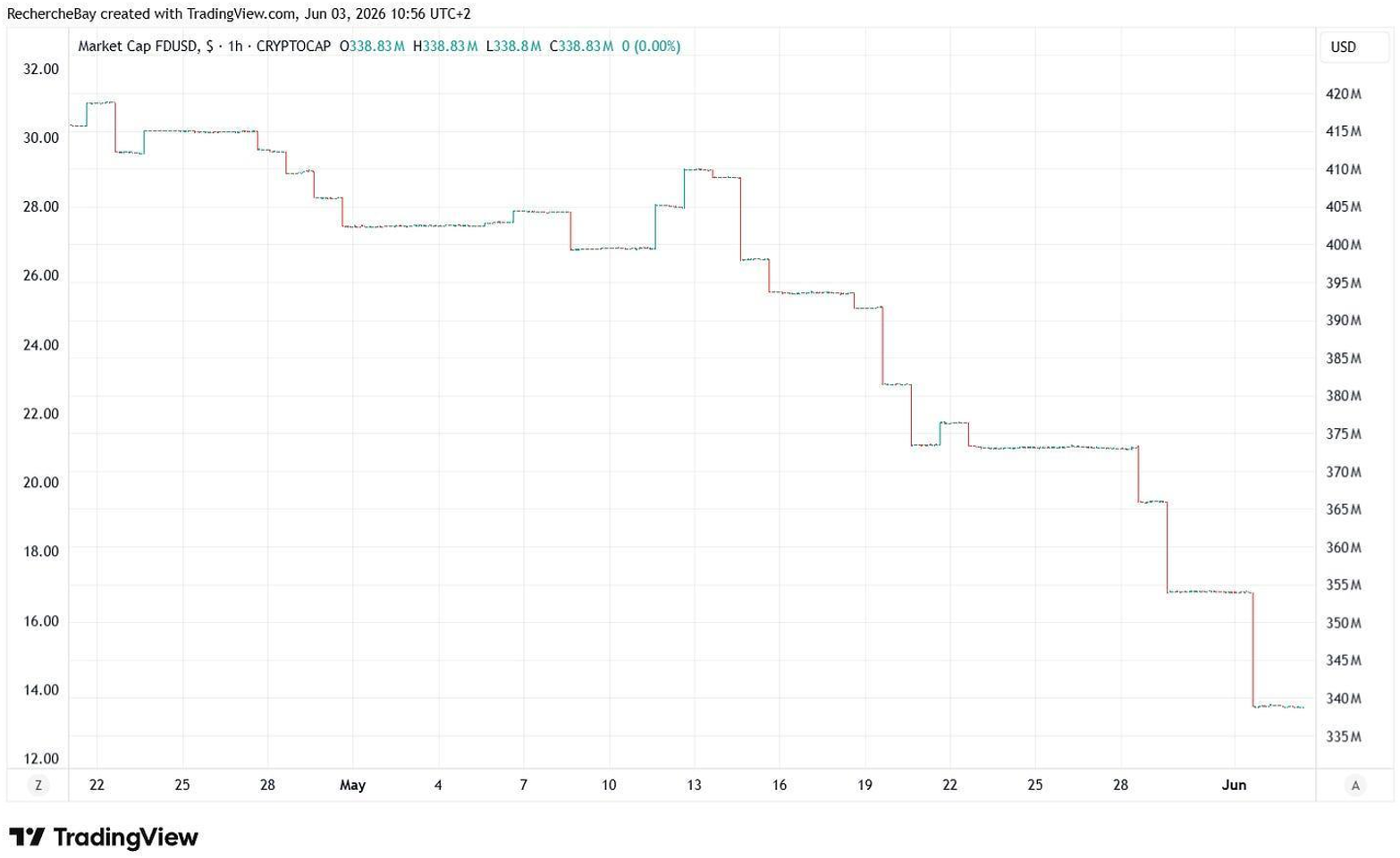

Moreover, the signal sent by cryptocurrencies is becoming increasingly difficult to ignore. While tech megacaps continue to capture the bulk of capital flows, a significant portion of the crypto ecosystem is sending a radically different message. The most striking example is likely that of FDUSD, whose market capitalization continues to plummet at an alarming rate:

Since its recent peak, the stablecoin has lost nearly a quarter of its market capitalization, dropping from approximately $420 million to less than $340 million in just a few weeks. This development is by no means insignificant. Unlike a stock or a commodity, a stablecoin is supposed to represent a form of liquidity available within the crypto ecosystem. When its market capitalization contracts sharply, it means that capital is leaving the ecosystem, positions are being closed, or confidence in certain market infrastructures is eroding.

More broadly, the continued decline of FDUSD echoes episodes observed during previous liquidity crunches in the sector. It is not so much the absolute size of the stablecoin that matters as the direction of the flow. For several weeks now, every rebound in tech markets has paradoxically been accompanied by a gradual drying up of certain pockets of crypto liquidity. This divergence warrants attention. In a true “risk-on” environment, capital simultaneously flows into technology, cryptocurrencies, speculative assets, and the riskiest segments of the market. Today, this is no longer the case. Flows are concentrating on an ever-smaller number of assets, while the rest of the system is gradually losing depth.

This trend reinforces the idea that we are not facing widespread euphoria but rather an extreme concentration of capital. Investors are buying Nvidia, Microsoft, or the supposed big winners of artificial intelligence, but they are simultaneously withdrawing liquidity from other segments traditionally associated with risk appetite. The contrast is striking: while Wall Street celebrates the future abundance promised by AI, certain liquidity indicators continue to send a much more cautious message. Historically, this type of divergence rarely appears at the start of major bull markets. It manifests much more often when liquidity becomes more selective and the market begins to distinguish the few assets it absolutely wants to hold from all the others.

The more capital concentrates on a small number of stocks, the more resilient the indices appear. But the more this concentration increases, the more fragile the market as a whole becomes.

The same investors who are aggressively buying into artificial intelligence leaders continue to sell or ignore sectors directly linked to the real economy: energy, industrial metals, infrastructure, and materials.

Yet it is precisely these sectors that will be indispensable for building the power grids, data centers, energy infrastructure, and industrial capacity necessary for the development of artificial intelligence.

The paradox is all the more striking as investors continue to assign ever-higher valuations to the supposed beneficiaries of artificial intelligence while largely ignoring the physical constraints that will limit their future growth. Markets today are buying into the promises of AI without actually buying the raw materials, energy, and infrastructure that will make this revolution possible. Yet demand for copper, electricity, transportation networks, and industrial capacity is already skyrocketing. This contradiction is even evident within the tech giants themselves. Google recently had to sell shares to help finance the sharp increase in its investments in artificial intelligence and cloud infrastructure. Behind the impressive revenue growth lies a far less glamorous reality: AI has become an extremely capital-intensive industry. Hyperscalers are no longer just building software; they are now building power plants, networks, data centers, and physical infrastructure costing hundreds of billions of dollars. Yet the market continues to value these companies as if future growth were primarily digital, even though a growing portion of their business model now relies on heavy industrial investments.

In other words, Wall Street continues to bet on the architects of the AI revolution, but still refuses to buy the bricks, cement, and cables that will make it possible to build it. It is often in this type of disconnect that the biggest sector rotations emerge.

This disconnect cannot last indefinitely.

As physical constraints re-emerge — whether in copper, electricity, hydrocarbons, or infrastructure — the issue of real resources risks gradually overshadowing mere promises of growth. The resilience of physical gold serves as a subtle yet powerful reminder of this reality. Despite the euphoria surrounding AI, investors continue to pay a significant premium to hold the ultimate monetary asset, a sign that risks related to liquidity, debt, and the credibility of currencies have by no means disappeared. After reaching new all-time highs, the price of gold is now consolidating below its record levels, but this consolidation masks structural forces rarely observed with such intensity. Central banks continue to accumulate the metal at a steady pace, China is recording record purchases of bars and coins, and gold now accounts for a larger share of global reserves than U.S. Treasury bonds. Since the freezing of Russian reserves in 2022, a growing number of countries have come to view gold not merely as a store of value, but as a true monetary insurance independent of any issuer. In other words, while the market pins its hopes for growth on a handful of artificial intelligence giants, central banks continue to increase their exposure to one of the oldest assets in financial history. This coexistence between the market’s sole promise of growth and the ultimate monetary asset is likely one of the most revealing divergences of the current cycle.

That is precisely what makes the coming months particularly interesting.

If the current volatility regime remains under control, the concentration could continue for some time and extend the lead of mega-cap tech stocks.

But if a liquidity shock, a bond market crash, or a breakdown in the short-volatility strategy were to occur, the market could suddenly rediscover a reality it seems to want to ignore today: no technological revolution can develop without physical resources.

And when this realization sets in, capital rotations are rarely gradual.

They are usually abrupt.

So perhaps the question is no longer how much higher tech stocks can go.

The real question is how much longer the market can continue to ignore the rest of the real economy.

Reproduction, in whole or in part, is authorized as long as it includes all the text hyperlinks and a link back to the original source.

The information contained in this article is for information purposes only and does not constitute investment advice or a recommendation to buy or sell.