While equity investors continue to celebrate AI, share buybacks, and narratives of a soft landing in a frenzy that increasingly resembles the excesses of a late-cycle environment, the bond market has been sending a radically different message for several weeks now. And historically, it is always fixed income that ultimately sets the tone for the rest of the financial system.

Something unusual is happening: despite an objectively risk-off geopolitical environment, risky assets continue to outperform while bond markets are quietly deteriorating in the background. Equity volatility, as measured by the VIX, fell rapidly after the initial shock in the Middle East, but sovereign yields continued to climb.

The implicit message from the bond market is becoming increasingly difficult to ignore.

Fixed-income investors are beginning to come to terms with a much more uncomfortable reality: skyrocketing budget deficits, energy-driven inflationary pressures, massive refinancing, growing fragility in the private credit market, and the return of physical constraints in the global economy.

I am writing this bulletin from London, where I have been holding numerous discussions over the past few days with portfolio managers, asset allocators, and fixed-income specialists. And a very clear shift in tone is beginning to emerge.

As recently as last year, most discussions remained focused on the possible return of the classic 60/40 portfolio — stocks and bonds — with the idea that bonds would gradually regain their historical role as a stabilizer following the inflationary shock of 2022.

Today, the doubt is becoming much deeper.

The question is no longer simply whether bonds will regain their appeal, but whether they can continue to serve as a “risk-free” asset in the long term in a world marked by structural deficits, energy tensions, and massive refinancing needs.

And one particularly telling sign: the potential role of gold in investment portfolios is now being discussed much more seriously. This was clearly not the case just a year ago.

Even in London — the historic heart of the Western financial system and the global bond market — the current crisis is beginning to reignite debates that many still considered marginal until recently: the sustainability of sovereign debt, the credibility of central banks, the return of financial repression, and the place of real assets in long-term portfolios.

The United Kingdom now appears to be one of the primary epicenters of this tension.

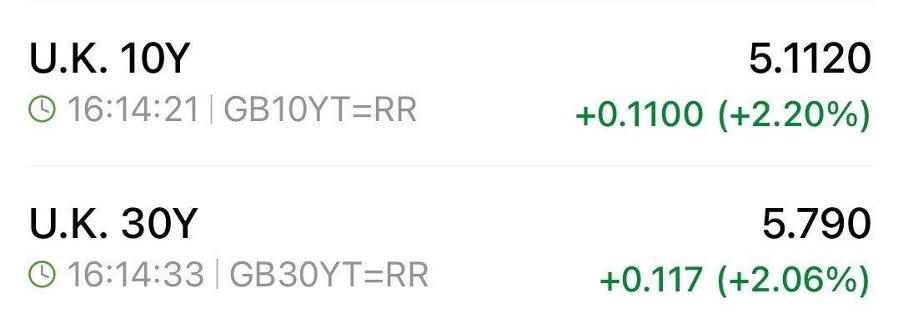

British GILTs are returning to levels that are dangerously reminiscent of the 2022 pension fund crisis, with the 10-year yield now above 5.1% and the 30-year yield close to 5.8%:

Many had viewed the Liz Truss episode as an isolated political blunder. In reality, it was likely the first warning sign of a much deeper problem: that of an economic system that has become extremely sensitive to the cost of capital after more than a decade of artificially low interest rates. The United Kingdom today faces several vulnerabilities: a high budget deficit, weak growth, persistent inflation, heavy energy dependence, and, above all, significant reliance on foreign investors to finance its debt.

But there is likely another dimension that is widely underestimated: the United Kingdom is also a large island that is extremely dependent on energy, food, and industrial imports. In a world of seamless globalization and low energy costs, this model worked perfectly. In an environment marked by geopolitical fragmentation, maritime tensions, rising logistics costs, and the return of physical constraints, this vulnerability is suddenly reemerging.

Japan is likely an even more critical case. For over twenty years, the global financial system has relied heavily on the artificially low rates maintained by the Bank of Japan.

The yield on the 30-year Japanese JGB now stands at 3.835%, the second-highest level in its history and a potencial record weekly close since the bond’s inception in 1999.

This tension comes as markets increasingly anticipate another rate hike by the Bank of Japan at its June 16 meeting, with traders now pricing in a nearly 77% probability. The shift in tone is striking: some BOJ members now believe that a rate hike remains possible even if the conflict in the Middle East drags on.

The problem is that Japan remains extremely vulnerable to a sustained rise in rates. With public debt exceeding 220% of GDP — the highest in the developed world — every rise in yields automatically increases the government’s refinancing costs and gradually weakens banks, insurance companies, and the global carry trade.

For years, the markets have operated under the assumption that the BOJ had complete control over its bond market. That certainty is now beginning to fade.

This policy has fueled the global carry trade, suppressed international yields, and propped up risky assets across the board. But Japan is now beginning to import real inflation through energy, food, the weak yen, and rising import costs. Yet the BOJ finds itself trapped. If it allows rates to rise freely, the entire Japanese economic structure becomes vulnerable: government refinancing, domestic bond portfolios, banks, insurance companies, and the global carry trade. And if it continues to artificially keep rates too low, the yen will continue to depreciate, further exacerbating imported inflation. Here again, the geographic and energy factors are likely central. After Fukushima, Japan became even more dependent on hydrocarbon and LNG imports. Like the United Kingdom, it is an island heavily reliant on global maritime trade, imported energy, and the stability of international supply chains. The resurgence of tensions over energy and shipping routes therefore strikes directly at the heart of the Japanese economic model.

The fact that these two jurisdictions are the first to see their bond markets tighten so sharply is therefore likely no coincidence. These are two economies:

- heavily indebted;

- extremely sensitive to the cost of capital;

- heavily dependent on imports;

- and historically built around a world of stable globalization, abundant energy, and persistently low interest rates.

In other words, the bond market may be starting to price in much more than just a budget problem. It may be gradually factoring in the return of a world where:

- energy is once again becoming a strategic constraint;

- supply chains are becoming fragile;

- deficits remain massive;

- and central banks can no longer maintain financial stability indefinitely without monetary consequences.

In this context, a question naturally arises: why hasn’t demand for precious metals skyrocketed in these two countries, even though the price of gold in yen recently reached historic highs?

The paradox is, in reality, only apparent. While gold is already skyrocketing in terms of the Japanese yen, this reflects above all a gradual loss of the currency’s purchasing power rather than a genuine systemic panic among domestic savers.

In other words, the foreign exchange market and gold are already signaling monetary deterioration, but collective psychology has likely not yet fully shifted toward an open loss of confidence in the financial system itself.

This is particularly true in Japan.

For more than thirty years, Japanese investors have lived in a world of:

- deflation;

- financial stability;

- zero interest rates;

- low inflation;

- and absolute confidence in domestic government bonds.

JGBs were considered virtually risk-free. Japanese households accumulated massive domestic savings, invested primarily in:

- deposits;

- life insurance;

- bonds;

- or extremely conservative investment vehicles.

Even today, despite the surge in gold prices in yen terms and the gradual rise in Japanese yields, a large portion of domestic investors likely continues to believe that the Bank of Japan will eventually regain control of the system, just as it has always done in the past.

And that is the crux of the problem: confidence in central banks has not yet been completely shattered.

For now, the market is seeing:

bond market tensions;

- imported inflation;

- a weak yen;

- rising living costs;

- but not yet an outright breakdown of the monetary system.

Historically, however, major rushes into precious metals generally occur much later in the cycle:

- when investors realize that central banks are trapped;

- that real interest rates will remain negative for the long term;

- and, above all, that money itself is becoming the true risky asset.

The United Kingdom presents a different logic but one that is ultimately quite similar.

London remains one of the world’s major financial hubs. British institutional investors still think primarily in terms of:

- asset allocation;

- duration;

- bond management;

- hedging via derivatives;

rather than the preservation of physical assets.

In other words, even though GILTs are beginning to send extremely worrying signals, a large part of the British financial system continues to operate according to a “portfolio management” logic, not yet a mindset focused on “protection against systemic monetary risk.”

And this is likely where the fundamental difference lies with countries such as:

- China;

- India;

- Turkey;

- or certain regions of the Middle East,

where gold retains a much stronger cultural, monetary, and civilizational significance.

There is also likely another very important factor: the current crisis is still driving enormous demand for liquidity.

In the early stages of systemic stress, investors first seek:

- cash;

- collateral;

- dollars;

- liquid assets;

This is exactly what we observed in March 2020:

Gold initially corrected sharply before surging later when central banks were forced to ramp up liquidity injections on a massive scale.

And that is likely what many precious metals experts are watching for today.

Because if the bond crisis continues to worsen:

- central banks will likely have to intervene again;

- rate control programs could reappear;

- the implicit monetization of deficits would become more visible;

- and monetary credibility could then begin to be questioned much more openly.

At that point, the rise in gold could take on a completely different character.

Today, gold is rising primarily as a symptom of gradual monetary depreciation.

Tomorrow, it could rise as an asset of systemic distrust.

And it is likely this psychological transition that has not yet fully taken place in Japan and the United Kingdom:

investors are beginning to understand that sovereign bonds are no longer entirely “risk-free”…

but they have not yet fully accepted that the currencies themselves could gradually become the real problem.

Reproduction, in whole or in part, is authorized as long as it includes all the text hyperlinks and a link back to the original source.

The information contained in this article is for information purposes only and does not constitute investment advice or a recommendation to buy or sell.