The silver market is shifting into a much tighter situation than it appears at first glance. Behind the sometimes erratic fluctuations in futures prices, the physical market continues to tighten — slowly but surely.

Since 2021, nearly 762 million ounces have been drawn from global inventories.

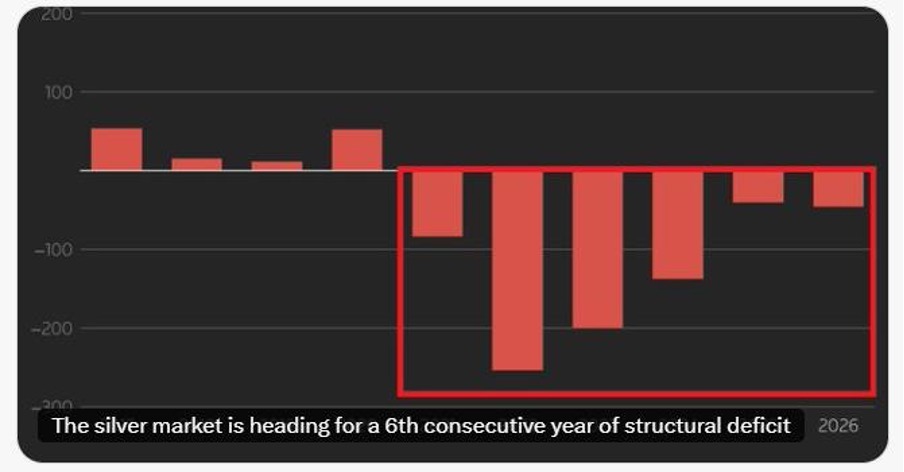

This erosion is by no means a cyclical phenomenon: it reflects a structural imbalance that is becoming entrenched over time. The year 2026 is expected to mark a sixth consecutive deficit, with an anticipated shortfall of 46.3 million ounces — a 15% increase year-over-year. In other words, the market consistently consumes more than it produces — and this trend persists.

This point is fundamental: unlike gold, silver is primarily a byproduct.

The key point — often underestimated — lies in the very nature of its production chain: indirect, fragmented… and dependent on a less visible yet critical link: sulfur.

In most cases, silver is not mined for its own sake. It is recovered during the processing of zinc and copper concentrates. However, this processing relies heavily on hydrometallurgical processes — particularly leaching — which require significant amounts of sulfuric acid.

Sulfuric acid is itself produced from sulfur, which often comes from oil and gas refining. This is where the link becomes systemic: any strain on energy supplies or crude oil flows (as we are currently seeing with geopolitical disruptions) directly results in a decline in sulfur production… and thus in sulfuric acid production.

In concrete terms, to simplify:

Less refined oil → less recovered sulfur → less available sulfuric acid → less ore processing capacity → less metal recovery… including silver.

But the problem doesn’t end there. Even when sulfuric acid is available, its price can skyrocket. In certain markets — particularly in South America — the cost of sulfuric acid has increased severalfold during periods of logistical strain. As a result, some operations become temporarily unprofitable or operate at reduced capacity. This further limits actual production.

This is where the concept of a supply disruption comes into play. We are no longer in a traditional scenario where rising silver prices automatically encourage increased production. The system is constrained at the upstream stage. Zinc or copper producers cannot simply “step up” silver production, as they remain constrained by:

- the availability of sulfuric acid

- the processing capacity of facilities

- and, upstream, the dynamics of the energy market

In other words, the price signal is no longer being transmitted correctly to the supply side. This represents a breakdown of the traditional adjustment mechanism.

And this disruption is all the more critical because it is invisible to most investors. On a screen, you see a price. But behind that price lies a complex industrial chain, dependent on chemical and energy flows. When this chain seizes up, production doesn’t slow down gradually — it can grind to a sudden halt.

It is precisely this type of scenario that transforms a “manageable” deficit into a potentially explosive shortage. When demand continues to rise (solar, investment, etc.) and supply can no longer keep up — not by choice, but due to physical constraints — the market enters a zone of non-linearity.

And in these phases, adjustments are never gradual: they are violent.

The silver market thus finds itself caught in an invisible squeeze, where its industrial dependence drastically limits its ability to adjust.

At the same time, demand is shifting. While certain industrial sectors are slowing slightly due to rising prices — particularly solar energy and jewelry — this decline is largely offset by a sharp acceleration in investment demand. Coins, bars, ETFs: flows are shifting toward physical metal, putting further pressure on available inventories.

This shift in demand is fundamental.

It is transforming a market historically driven by industry into one increasingly dominated by the logic of value preservation and hedging. Against a backdrop of supply chain tensions — energy, base metals, chemical inputs — this shift acts as an amplifier.

A particularly telling sign of this tightening is beginning to reappear: premiums on the Shanghai market are rising again. In other words, the price paid to obtain physical metal in China is once again significantly exceeding international benchmarks.

This type of trend is never insignificant. It reflects both local supply pressures and, more broadly, intensifying competition to secure available metal.

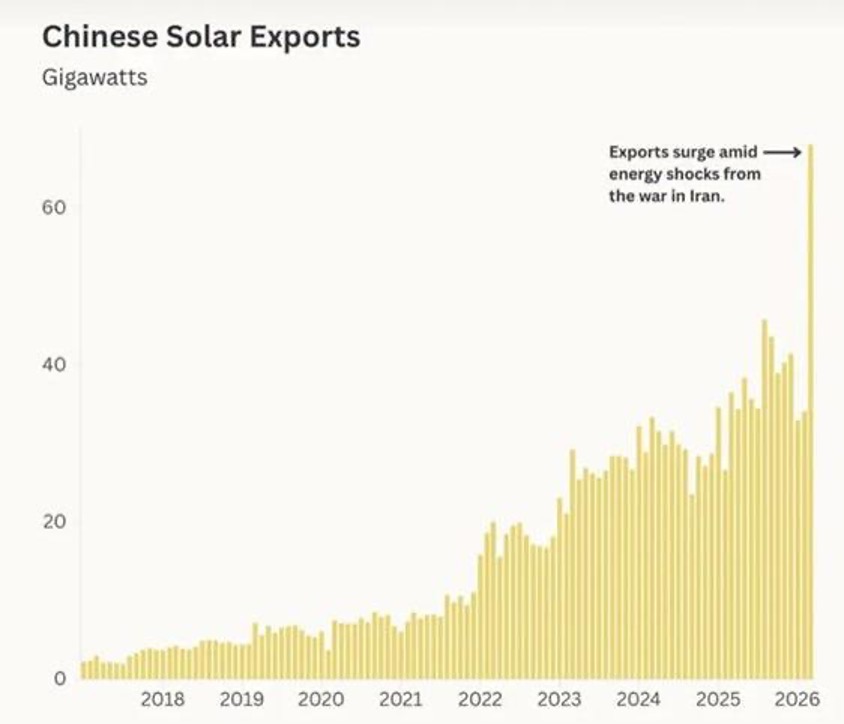

At the same time, another factor is exacerbating this structural pressure: Chinese industrial demand, driven by the solar sector, is accelerating significantly.

Chinese solar panel exports have literally doubled in just a few years, with a recent surge amid the energy crisis. However, this industry is extremely silver-intensive. This means that, even in a high-price environment, demand does not contract — on the contrary, it continues to grow.

This is precisely where the imbalance becomes critical. While demand is accelerating, the supply of silver from mining reacts very little to prices. Unlike other commodities, there is no rapid mechanism to increase production. The market therefore finds itself facing a rare situation: structurally expanding demand confronted with a rigid, even constrained, supply.

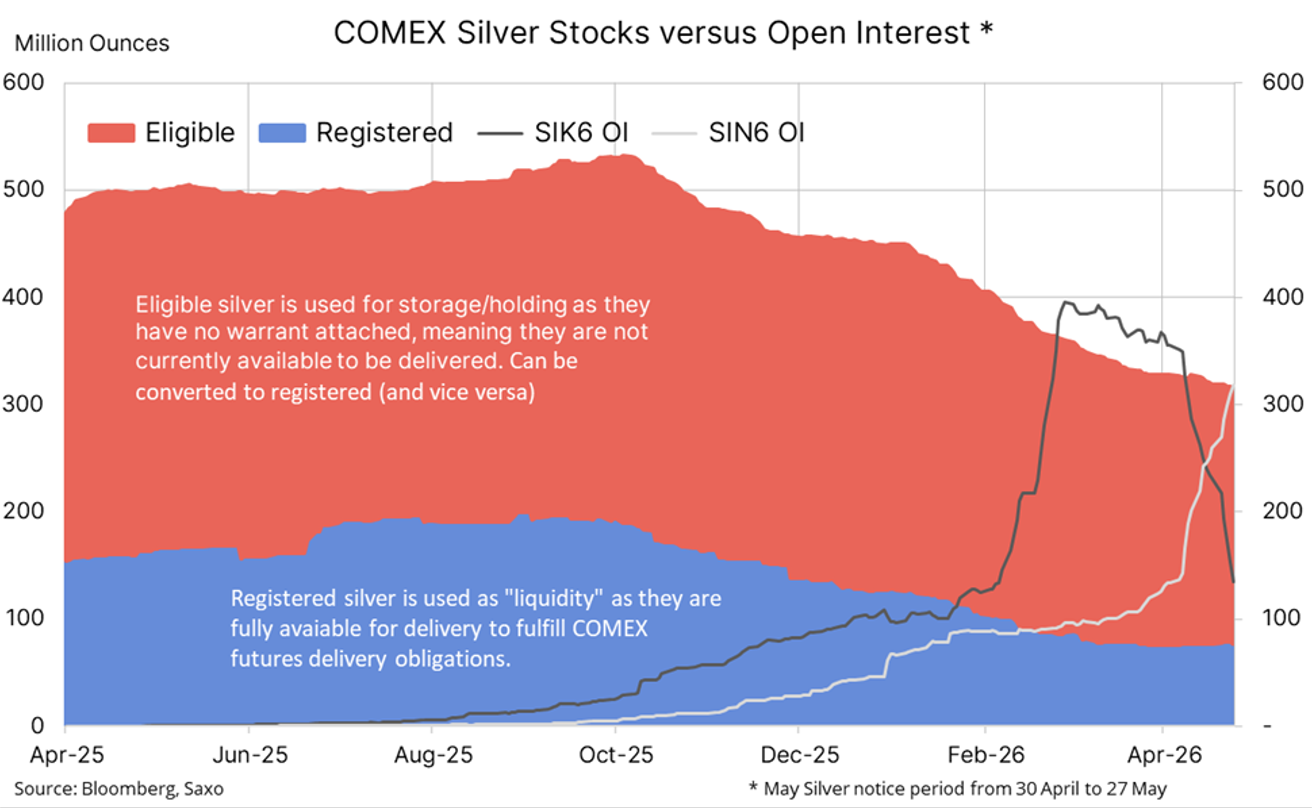

Added to this is a more technical aspect, yet one essential to understanding current tensions: the functioning of the COMEX futures market. Specifically, there are two types of silver stocks. “Registered” stock refers to metal actually available for immediate delivery. “Eligible” stock, on the other hand, is simply stored in vaults without being committed for delivery — it belongs to holders who are not necessarily sellers.

What is worrying the market today is the growing gap between actual available inventory and the volume of outstanding contracts — the open interest. As expiration dates approach — such as the recent March expiration and the upcoming May expiration — traders face a simple choice: accept physical delivery, “roll” their position to a later expiration date (such as July), or close it out.

For a layperson, it can be illustrated this way: it’s like booking airline tickets. As the departure date approaches, you either board the plane (delivery), change your flight (roll), or cancel. But if too many passengers want to board at the same time while seats are limited (restricted registered stocks), tension rises immediately.

This is precisely what we are seeing today. After the tensions surrounding the March expiration, attention is now focused on the May contract. As we approach the notice period (late April), open interest is declining rapidly — which is normal — as positions are rolled over or closed. But this mechanism masks a vulnerability: it postpones the problem of physical delivery without resolving it.

In other words, as long as the majority of market participants choose not to take physical delivery, the system holds. But in a context of growing scarcity and rising physical demand, this balance is becoming increasingly precarious.

The market then becomes extremely sensitive to minor shocks. As inventories shrink, even the slightest imbalance can trigger disproportionate price movements. This is exactly what is beginning to unfold: increased volatility, sharp spikes, and, above all, a growing disconnect between the paper market and physical reality.

This phenomenon is not unprecedented. The silver market has already experienced this type of dynamic: years of apparent control via futures, followed by a brutal readjustment when the physical market regains the upper hand.

Behind the scenes, the entire market structure is changing. Silver is no longer simply an industrial metal or a speculative asset. It is gradually becoming a strategic asset, shaped by considerations of scarcity, industrial sovereignty, and security of supply.

In this context, the idea that current price levels are sufficient to rebalance the market is likely an illusion. Historically, prolonged deficits are not resolved through simple normalization, but through a sharp — and often belated — revaluation when physical constraints become impossible to ignore.

The silver market may be shifting into a new phase. And as is often the case during these transitional phases, the signal will not come from models… but from reality.

Reproduction, in whole or in part, is authorized as long as it includes all the text hyperlinks and a link back to the original source.

The information contained in this article is for information purposes only and does not constitute investment advice or a recommendation to buy or sell.