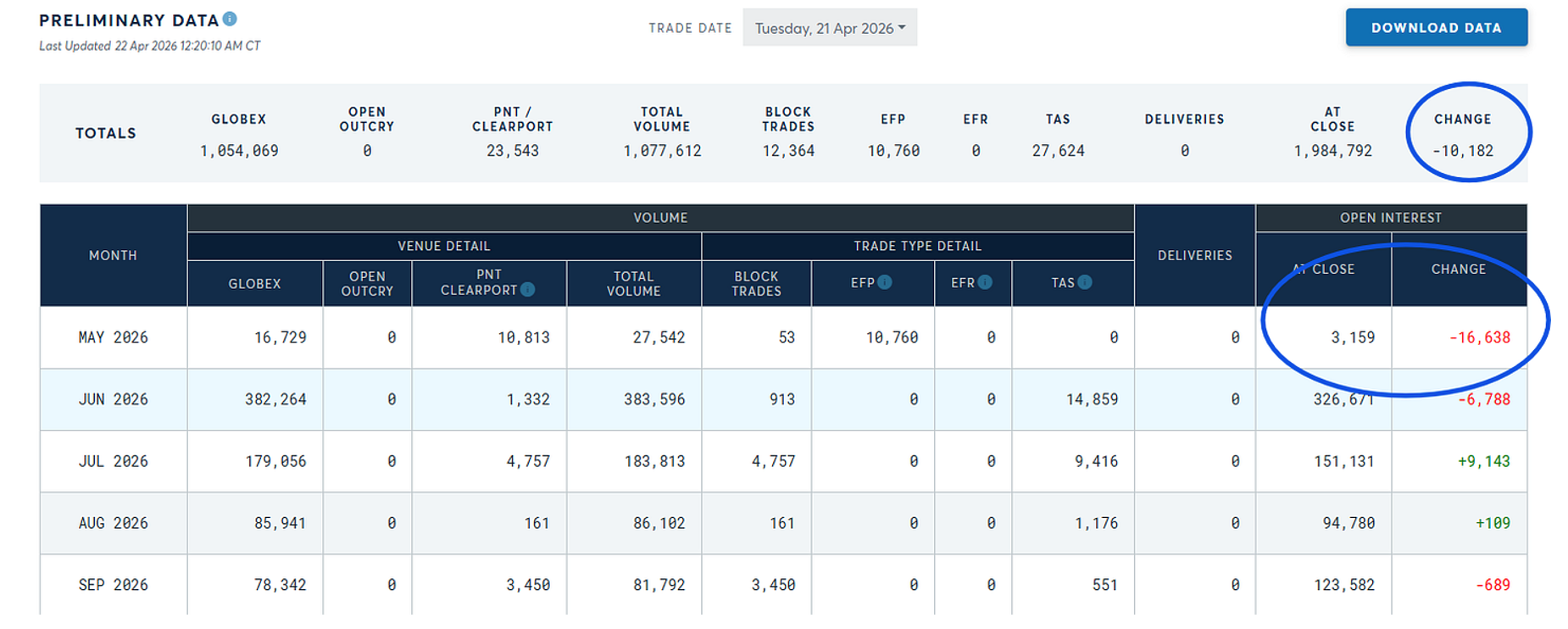

The latest NYMEX delivery data sends an extremely clear signal: the paper market is starting to crack. Specifically, only about 3,000 WTI contracts maturing in May 2026 will be delivered, compared to a historical average of nearly 90,000. To a novice observer, this may seem like a technical detail, but the implications are significant.

A crude oil futures contract is, in theory, a binding commitment: to deliver crude oil or take delivery of it at maturity. Under normal circumstances, a significant portion of contracts reach this stage, ensuring that futures prices remain tied to physical reality. But today, that link is weakening. Market participants are exiting en masse before expiration — not out of opportunism, but because they refuse to assume the risk of delivery in a market that has become too uncertain.

In other words, the market continues to display a price… but fewer and fewer participants are willing to honor it physically.

For those who have followed the silver market on COMEX for years, the current situation on NYMEX is troubling. We see similar dynamics there: a derivatives market that continues to set a price, even as the physical market tightens and participants capable of taking delivery withdraw. In the case of silver, this disconnect was able to persist for a long time — until the system finally collapsed.

It is through this lens that we must understand the current situation.

I am writing this report as a direct follow-up to my recent discussions in Hong Kong with executives from mining companies, hedge funds, and physical market operators. The disconnect between financial perceptions and logistical reality has never been more pronounced. We are no longer in a phase of tension; we have entered a phase of disruption.

The key point is simple, almost mechanical: the oil market crossed its tipping point in mid-April. The last barrels shipped from the Gulf have reached their final refineries. From now on, any supply shortfall — estimated at between 11 and 13 million barrels per day — can no longer be concealed. It must show up somewhere:

- either in inventories, which will begin to shrink rapidly,

- or in refined products, whose prices will adjust sharply,

- or in demand, which will have to be curtailed.

And yet, remarkably, the futures market remains surprisingly calm.

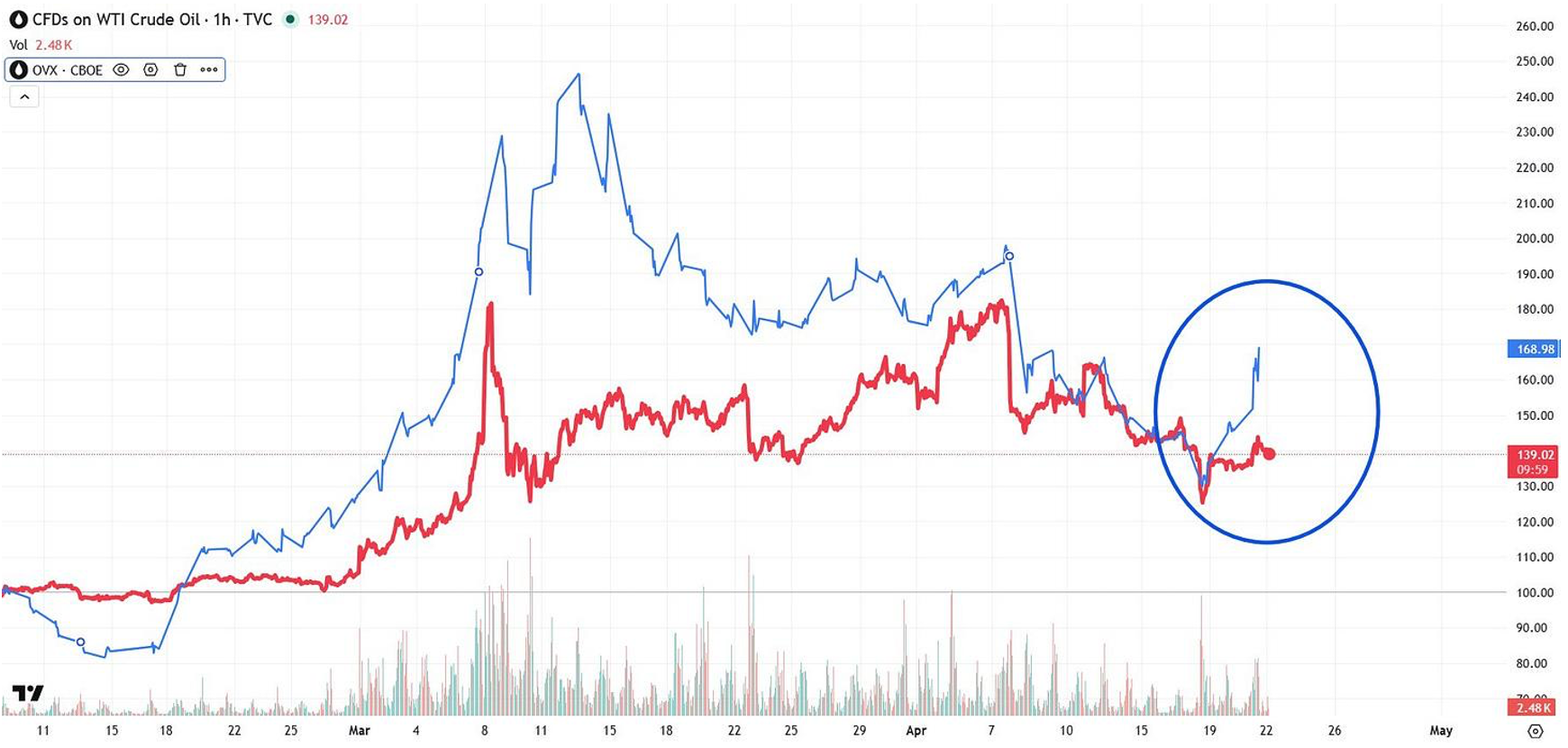

Another signal — more technical but just as telling — has emerged over the past 48 hours. Oil futures ($USOIL) and implied volatility ($OVX) are diverging sharply. In other words, prices remain relatively stable, but the cost of hedging against a sharp price move is on the rise.

This type of divergence is rarely insignificant.

It indicates that certain market participants — likely large ones — are no longer betting on the immediate direction of the price, but on the likelihood of an extreme move in the future. On the surface, the market remains calm. Beneath the surface, risk pricing is undergoing a shift.

This is precisely the type of pattern observed during critical transition phases: the price isn’t moving yet… but the market is already paying to protect itself from what might happen.

The market therefore does not reflect an absence of risk. It reflects an absence of participation.

This point is fundamental.

We are not facing a simple market lag. We are facing a market that has temporarily lost its ability to aggregate physical information. Arbitrage has become too complex, too risky, too capital-intensive. The link between paper and physical assets is fraying — and this disconnect may last… until it can no longer do so.

Meanwhile, the physical system continues to tighten.

The shock is primarily logistical. It is not merely a theoretical imbalance between supply and demand, but a concrete blockage of flows, particularly around the Strait of Hormuz. Even in an optimistic scenario of a rapid reopening, transportation delays introduce a lag that makes the shock inevitable.

This sets off a self-reinforcing dynamic: The shortage of crude reduces refinery throughput → This reduction lowers refined product inventories → The drop in inventories pushes margins higher, incentivizing an increase in throughput… → which further intensifies the pressure on available crude.

This type of loop is characteristic of physical markets under extreme stress. It is not resolved by prices alone, but by the destruction of demand.

And that is precisely where the market becomes unstable.

For while oil remains contained on the surface, tensions are building beneath the surface. Inventories are nearing critical levels. Supply flows are becoming fragmented. Market decisions are taking on a political dimension. The price is gradually ceasing to be a balancing factor and becoming a tool for rationing.

It is in this kind of environment that the gold market takes on a new dimension.

When energy prices become unpredictable, when derivatives markets no longer reflect physical reality, and when supply chains break down, gold once again becomes an anchor asset. Not just against inflation, but against a broader loss of confidence in the system itself.

The paradox of the moment is therefore as follows:

Oil is sending mixed signals.

The market appears calm on the surface, even as risks mount.

But gold is already beginning to reflect this turmoil.

If this phase continues, the recent rise in the price of gold will not be merely a short-term trend.

It will reflect a much more profound shift: that of a market that is gradually ceasing to believe that the listed price is still the true price of the world.

Reproduction, in whole or in part, is authorized as long as it includes all the text hyperlinks and a link back to the original source.

The information contained in this article is for information purposes only and does not constitute investment advice or a recommendation to buy or sell.