Major speculative bubbles often follow a remarkably similar psychological and financial pattern. It all begins with a genuine innovation that profoundly transforms the economy: the Internet in the 1990s, securitized real estate in the 2000s, and today, artificial intelligence and digital infrastructure.

This is followed by a phase of acceleration in which the market gradually ceases to take physical, operational, or financial constraints into account. Valuations expand, capital becomes abundant, and investors eventually come to believe that future growth justifies virtually any current price.

This is precisely the dynamic currently reflected in assets such as the Korean KOSPI or Micron Technology. The KOSPI, historically highly correlated with the global semiconductor and memory cycle, is entering a near-parabolic phase, driven by the euphoria surrounding AI, data centers, and demand for HBM.

For its part, Micron has emerged as one of the most striking symbols of this advanced stage of the bubble. The market no longer views the company simply as a cyclical firm exposed to the memory sector, but rather as a form of “essential infrastructure” for the AI revolution.

Investors are barely paying attention to the historical cycles of overcapacity specific to the memory industry anymore; they now anticipate virtually unlimited demand driven by GPUs, AI clusters, and hyperscalers.

The most interesting thing is that these two charts tell exactly the same story as previous episodes: it is no longer just the end product that is gaining value, but the entire upstream supply chain. HBM memory is becoming the modern-day equivalent of optical equipment in 1999 or construction materials in 2007. Prices are skyrocketing because every player in the system is seeking to capture a share of the speculative windfall created by AI.

Samsung, SK Hynix, and Micron are raising their prices, prioritizing HBM production lines, and massively reallocating their capacity. The entire Korean semiconductor supply chain is gradually being drawn into this dynamic.

But historically, it is precisely at this stage that imbalances begin to become dangerous.

Rising memory prices are gradually altering the economics of AI projects themselves. Cluster costs are skyrocketing. Energy expenses are rising. Capex requirements are becoming enormous. And, as is often the case, the price surge eventually attracts new capacity — sometimes economically marginal — financed primarily because the market continues to believe in linear demand growth.

It is precisely in this final phase that the same signal almost always appears: the explosion in input costs.

This dynamic generally follows a very specific pattern.

First, the entire upstream supply chain wants to “get in on the action.” When a sector is seen as the future, every supplier raises its prices and tries to capture a share of the speculative windfall.

Next, this cost inflation ends up profoundly altering the financial projections that had initially been used to justify the bubble. Growth models were based on assumptions of stable or even declining costs; inputs suddenly become inflationary.

Finally, the euphoria triggers a wave of overinvestment. Massive capacity is built everywhere, including on projects previously considered unprofitable. The system then ends up creating too much supply — often of marginal quality — precisely at the moment when real demand begins to slow.

In the final months of the dot-com bubble, it was no longer just the valuations of tech companies that were skyrocketing. Prices for optical equipment, routers, telecom components, and the entire infrastructure chain were also exploding. Telecom operators were engaged in a veritable race to buy fiber, Cisco equipment, optical lasers, and network capacity.

The logic seemed unstoppable at the time: Internet traffic would grow indefinitely.

But eventually, the entire upstream supply chain wanted a piece of the action. Component suppliers raised their prices. Equipment manufacturers expanded their production capacity. Fiber-optic projects were being financed around the world with increasingly lax financial discipline.

The problem is that this cost inflation eventually began to gradually undermine the very economics of the model. Capex spending was rising faster than actual revenue. The implied future margins built into valuation models were becoming increasingly unrealistic.

Then the system swung to the opposite extreme: massive amounts of network capacity were built, including in areas where demand would never have justified such investments.

The bubble didn’t burst because the Internet was a bad idea. It burst because the cost of the dream exceeded the cash flow it was actually capable of generating.

The pattern repeated itself in 2006–2008 with the U.S. housing market.

In the final euphoric phase, it wasn’t just house prices that were rising. Construction costs, wages, materials, land, and even building-related services were skyrocketing. The entire upstream supply chain in the real estate sector was seeking to capture its share of the windfall. Cement suppliers, builders, tradespeople, regional banks, mortgage brokers: everyone raised their prices or margins, convinced that the market would absorb any cost.

But once again, this cost inflation eventually eroded the real returns on new projects. The projections used to justify real estate developments gradually lost credibility.

Despite this, easy credit continued to fuel the machine. Increasingly speculative developers entered the market. Marginal land was developed. Entire neighborhoods were built without any real solvent demand to back them up.

As in all bubbles, rising prices eventually created an artificial supply that would never have existed in an environment of normal costs and disciplined financing.

In 2008, the phenomenon became even more visible in the energy sector. As oil approached $147, logistics costs skyrocketed across the board: trucking, diesel, ocean freight, storage, drilling, and pipelines. Energy-related companies entered a veritable race for equipment and capacity. Specialized oilfield transporters were charging record amounts. Operating and maintenance costs were rising so rapidly that they eventually destroyed demand itself.

Once again, the entire upstream sector sought to capture its share of the energy bubble. Oilfield service providers raised their rates. Rig costs skyrocketed. Marginal projects suddenly became “profitable” thanks to rising oil prices and abundant financing.

The system then generated a wave of excessive investment that ultimately resulted in massive capital destruction when prices turned downward.

Today, the market seems to be repeating a similar pattern with artificial intelligence.

The heart of the bubble no longer lies solely with Nvidia or the hyperscalers. The real warning sign lies in the skyrocketing physical costs required to support this trend.

HBM memory prices are soaring. GPUs are becoming scarce. There is a shortage of electrical transformers. Data centers are consuming massive amounts of electricity. Cooling costs are rising. Constraints related to helium, energy, power grids, and transmission infrastructure are gradually becoming critical.

And as with all previous bubbles, the entire upstream supply chain now wants to “get in on the action.”

Memory suppliers are raising their prices. Electricity producers are renegotiating their contracts. Transformer manufacturers are extending their lead times and widening their margins. Landowners near energy hubs are seeing their land become strategic assets. Even players in nuclear power, natural gas, and transmission infrastructure are beginning to be revalued through the lens of AI.

The problem is that the entire current argument is implicitly based on a future decline in the marginal cost of computing.

Yet it is precisely the opposite that seems to be happening in this advanced phase of the cycle.

Input costs are rising faster than actual monetization. Initial financial projections are becoming much more fragile.

Moreover, a significant portion of the revenue seen today has a circular dimension: AI labs raise capital from the very same tech giants that then sell them computing power. This creates the appearance of explosive growth, even though part of the flow circulates within the system itself.

At the same time, the euphoria is driving the construction of massive capacity. Data centers are popping up everywhere. Energy projects previously deemed insufficiently profitable are being revived. Marginal or less efficient forms of production become financeable simply because the market anticipates infinite AI-related demand.

Just like the unnecessary fiber-optic projects in 2000 or the excessive real estate developments of 2007, the system is beginning to create excess supply at the very moment when economic assumptions become most fragile.

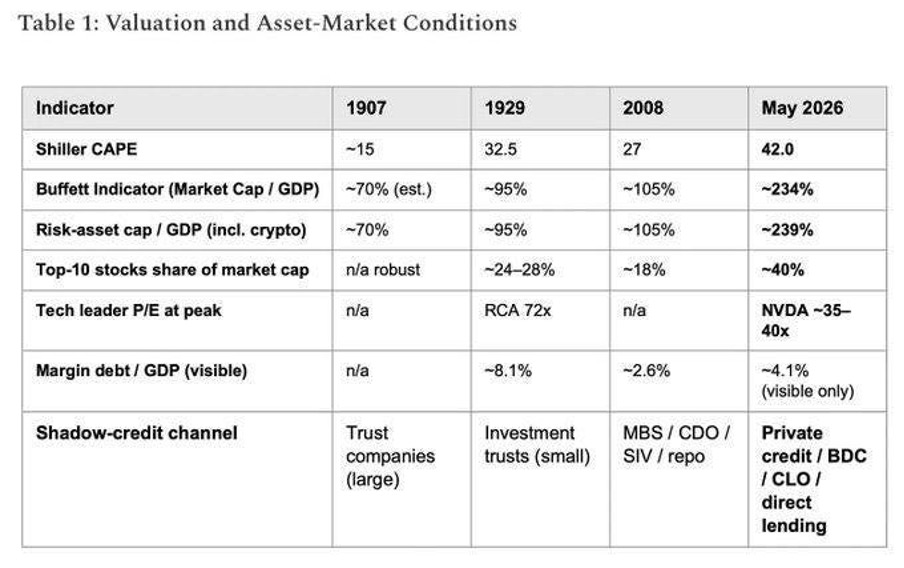

The table above shows just how much the current bubble already exceeds the major speculative episodes of the last century. In 1929, the U.S. market already appeared deeply disconnected, with a Shiller CAPE ratio close to 32 and an extreme concentration on a few industrial and radio leaders such as RCA, which was then trading at multiples that were astronomical for the time. In 2008, the credit bubble had pushed the U.S. market capitalization-to-GDP ratio to around 105%, fueled by real estate leverage and structured products.

But today, we are operating in a different dimension. The Buffett Indicator now exceeds 230% of GDP, a historically unprecedented level. The ten largest market caps account for nearly 40% of the entire U.S. market, meaning that a growing share of the indices relies almost entirely on a handful of companies linked to AI and digital infrastructure. Nvidia alone is trading at multiples reminiscent of the excesses of the tech leaders in 1999, even as the entire physical supply chain required for this revolution begins to come under strain: HBM memory, energy, transformers, power grids, cooling, helium, and data centers.

And as with all major bubbles, the real risk no longer lies solely in visible valuations, but in the less visible layers of credit that fuel the euphoria. In 1907, leverage was driven by trust companies. In 1929, on investment trusts. In 2008, on CDOs and shadow banking linked to subprime mortgages. Today, the momentum relies increasingly on private credit, CLOs, BDCs, and private financing structures that are quietly fueling the explosion in AI capex and energy infrastructure.

The market continues to celebrate a real technological revolution, but it seems to forget a historical constant: major bubbles do not burst when the narrative becomes false; they burst when the cost of financing and inputs makes that narrative economically unsustainable.

It is in these advanced phases that gold’s behavior becomes particularly interesting.

Historically, gold price does not react immediately to the onset of tech or financial bubbles. In the early phases of euphoria, capital favors high-growth assets, momentum strategies, and leveraged sectors. Gold then appears “useless,” yielding nothing, and often lagging behind.

But when input costs begin to skyrocket and physical constraints reemerge, its behavior gradually shifts. In the late 1990s, gold spent several years under pressure while tech stocks captured most of investors’ attention. Yet, as early as 1999–2000 — just as pressures on telecom infrastructure costs became extreme and central banks began to lose control of the liquidity cycle — gold stopped falling. The low point of its bear market coincides almost perfectly with the terminal phase of the Nasdaq.

In 2007–2008, the sequence was even more revealing. Gold and commodities initially rose together during the final inflationary phase of the credit bubble. Then, during the 2008 liquidity shock, gold corrected sharply along with the rest of the assets — not because its fundamental thesis was disappearing, but because the system had to sell everything it could to obtain dollars and collateral. Yet, unlike most cyclical assets, gold rebounded very quickly once central banks were forced to intervene on a massive scale.

This is often the classic sequence at the end of a cycle: first, a period of euphoria during which gold underperforms; then a phase where real costs begin to undermine the speculative narrative; followed by a liquidity shock where everything corrects simultaneously; and finally, a profound revaluation of gold when central banks are forced to monetize the imbalances stemming from the previous bubble.

The current period could follow a similar pattern. As long as the markets remain captivated by the growth of AI, mining stocks — and sometimes even physical gold — are underperforming relative to tech megacaps. But beneath the surface, the signals increasingly resemble those observed in the final stages of previous bubbles: rising cost of capital, energy strains, surging financing needs, inflation in critical inputs, and growing dependence on monetary liquidity.

The paradox is that rising costs initially fuel the euphoria. Investors interpret shortages as validation of demand. Prices accelerate. Companies increase their spending. Markets price in ever-more-optimistic future earnings.

Then, suddenly, the dynamics shift: costs erode margins, financing needs skyrocket, cash flows can no longer keep up, and the market realizes that the assumptions used to justify valuations were sustainable only in a world where inputs remained abundant and cheap.

And it is precisely at this moment that gold ceases to be perceived as a “useless” asset and returns to what it historically represents during regime shifts: a barometer of monetary credibility and real scarcity.

Reproduction, in whole or in part, is authorized as long as it includes all the text hyperlinks and a link back to the original source.

The information contained in this article is for information purposes only and does not constitute investment advice or a recommendation to buy or sell.