For several weeks now, the market has been behaving as if everything is finally going to “work out.” And this is no longer just the isolated view of a few sell-side strategists: it has now become a widely held consensus among global investors.

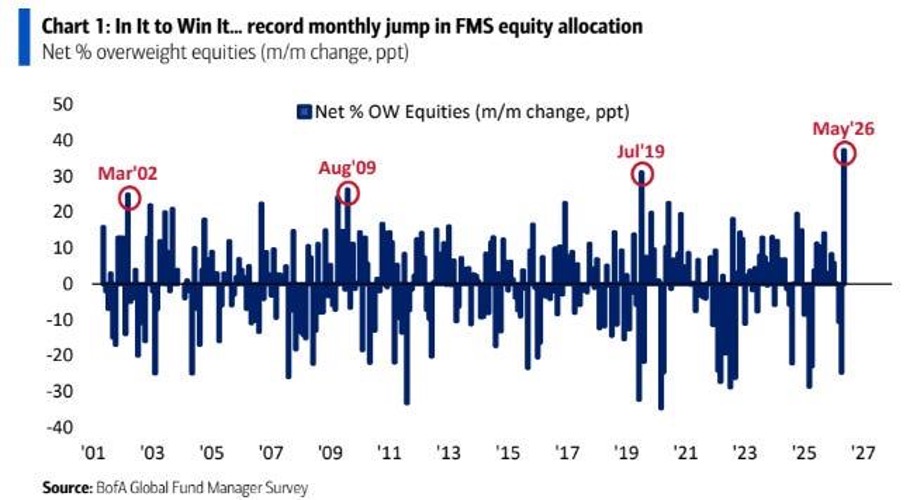

A recent study by Bank of America Global Research clearly illustrates this: in May, global fund managers made the largest monthly increase in their equity allocation in decades.

Market sentiment is now extremely bullish and reflects a prevailing view: the current energy and geopolitical crisis will remain contained, the Strait of Hormuz will reopen quickly, and central banks will eventually stabilize the situation.

The latest Fund Manager Survey shows just how extreme this bullish consensus has become. In May, global fund managers made the largest monthly increase in equity allocation ever recorded, raising their net overweight position from +13% to +50%.

At the same time, cash levels fell to 3.9%, officially triggering BofA’s historic sell signal. Speculative concentration has also reached remarkable levels: 73% of investors now consider “long semis” to be the most crowded trade in the market, compared to just 24% in April.

Finally, BofA’s Bull & Bear indicator has risen to 7.8 out of 8, a level close to historical extremes.

In other words, the market is now overwhelmingly positioned in the same direction.

This same survey also reveals the extent of this consensus on energy: 54% of investors anticipate the Strait of Hormuz reopening before the second half of 2026, with 44% expecting it as early as June. Conversely, only 5% foresee a prolonged blockade lasting until 2027 or beyond.

At the same time, the majority continues to anticipate Brent crude at around $80–90 by year-end, while only 7% of respondents expect oil prices to exceed $100.

In other words, the market is currently heavily positioned for a scenario of rapid normalization… which effectively amounts to a bearish medium-term view on oil. Most investors still believe that:

- SPR releases will be sufficient to cushion the shock,

- physical flows will eventually normalize,

- demand will slow,

- and that oil will gradually return to normal once the phase of geopolitical stress has subsided.

But this bullish consensus now extends far beyond the oil market alone.

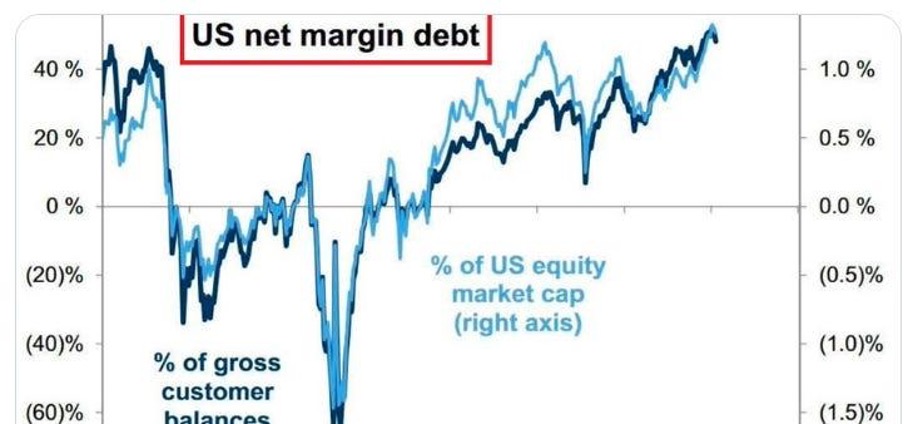

Speculation among retail investors has also reached levels rarely seen before. The net margin used by U.S. investors now accounts for nearly 50% of gross client balances, approaching all-time highs.

As a percentage of the total U.S. market capitalization, this margin debt is climbing toward 1.3%, again approaching all-time highs.

Speculation is even beginning to reach almost absurd levels in South Korea. Redemptions of life insurance policies from the country’s three major insurers jumped 16% in the last quarter, while deposits in savings banks fell below 100 trillion won for the first time in four years. Since February, term deposits at commercial banks have also fallen by 12 trillion won.

In other words, a growing share of the precautionary savings in the Korean financial system is now being redirected toward two themes: SK hynix and AI-related semiconductor giants.

The phenomenon becomes even more striking when we look at the profile of investors. Those over 50 now account for 62% of margin loans at the country’s top ten brokerage firms. Among investors in their 60s, margin debt has doubled in one year, rising from 3.9 trillion to 8 trillion won.

These are investors who have spent decades invested in bank deposits and real estate, and who are now — using leverage — entering a semiconductor boom nearing historic extremes.

Historically, when buying flows no longer come from disposable income but from the gradual liquidation of financial safety nets themselves, this rarely resembles the beginning of a cycle.

In other words, the stock market continues to operate under a regime of maximum risk-taking.

It is precisely this conviction that explains why every diplomatic statement, every rumor of negotiations, and every “TACO headline” — Trump Always Chickens Out — immediately serves as a pretext for aggressively shorting oil.

The intraday chart of WTI perfectly illustrates this dynamic: after several hours of bullish momentum fueled by rising volumes and aggressive buying, a single statement from Trump hinting at a possible postponement of military action against Iran was enough to trigger a vertical plunge in prices.

And it becomes even more striking when you look at the actual data.

Just yesterday, the API figures showed massive drawdowns:

- crude: -9.1 million barrels versus an expected -3.4 million barrels,

- gasoline: -5.8 million barrels,

- distillates: -1.0 million barrels,

- Cushing: -1.4 million barrels,

- SPR: -9.9 million barrels.

Even taking into account SPR releases, draws remain extremely tight, confirming that the physical market continues to tighten rapidly. Yet every headline suggesting a de-escalation continues to trigger aggressive selling in oil futures.

This disconnect between the paper market and the physical market is likely becoming the heart of the current debate.

For while equity markets are returning to euphoric levels and investors are massively increasing their risk exposure, a growing number of physical market analysts believe, on the contrary, that the global energy system has already entered a phase of disorganization far more advanced than financial prices currently reflect.

The argument put forward by HFI Research is relatively simple: the sell-side continues to operate on the assumption that the problem remains primarily geopolitical and financial, whereas the market has already entered a phase of physical disruption in global oil flows.

According to HFI, Goldman Sachs, JPMorgan Chase, and Morgan Stanley implicitly share a common assumption: the Strait of Hormuz will reopen soon — likely as early as June — and oil will remain near $100 through the end of the year. But HFI considers this scenario increasingly unlikely.

Their main argument is that the global logistics system has already crossed a critical threshold. Even if a diplomatic resolution is reached quickly, production is unlikely to resume in earnest before August due to logistical constraints.

A significant portion of ballast tankers has already been redirected to the United States to clear the last remaining storage surpluses. The time required to redeploy them to the Persian Gulf would ensure several additional weeks of disruption.

In other words, even in a scenario of rapid de-escalation, the physical market would not immediately return to normal.

HFI also emphasizes a more psychological dimension of the conflict. Since the crisis began, their reasoning has been based on a simple idea: every day without a resolution increases the likelihood that no rapid resolution will ultimately occur.

For the United States, a rapid withdrawal would now appear to be a major strategic defeat. For Iran, with the costs of the conflict already largely incurred, the logic is gradually shifting toward endurance and attrition.

In this context, HFI believes that the current consensus significantly underestimates the risk of the conflict becoming bogged down.

The figures reported for May give an idea of the scale of the shock:

- approximately 12 Mb/day of disrupted production,

- partially offset by 2 Mb/day of demand reduction,

- and 2.5 Mb/day from strategic reserves.

The implied deficit would therefore remain close to 7.5 million barrels per day.

But perhaps the most significant aspect of this argument concerns the SPRs themselves. According to this interpretation, U.S. strategic reserves are no longer used merely as an emergency tool designed to temporarily cushion a supply shock. They have reportedly gradually become a financial stabilization tool aimed at preventing oil from further fueling inflation and inflationary expectations.

Since the start of the conflict, several large-scale SPR leasing operations have been launched. Yet, tellingly, these volumes have not been fully absorbed by physical traders, despite sometimes attractive terms.

For proponents of the physical thesis, this signal is significant: it suggests that market participants anticipate significantly higher future prices and fear they will not be able to repurchase these barrels at a lower cost later to return them to the Department of Energy.

Approximately 133 million barrels have reportedly already been allocated for deliveries from May through July. If these volumes are indeed drawn down, U.S. strategic reserves could fall to new historic lows near 282 million barrels.

And yet, despite these massive drawdowns, oil futures remain under steady pressure.

Just yesterday, a massive order in Brent options shook up the energy desks: the equivalent of 134 million barrels was traded via a very short-term $91/$90 put spread.

Officially interpreted as a bearish bet, several traders see it instead as a volatility-selling strategy aimed at capitalizing on the exceptional premiums generated by geopolitical headlines.

The troubling detail lies elsewhere: this notional amount corresponds almost exactly to the volume of Strategic Petroleum Reserve (SPR) released by the United States since the start of the conflict with Iran. Who is really behind this order?

For now, volatility sellers, CTAs, and macro desks clearly retain control over the pricing of the paper market. The consensus remains that oil prices will eventually peak and then gradually return to lower levels once geopolitical tensions subside.

But the risk raised by the physical thesis is that at some point, the market will no longer be able to mask the reality of logistical constraints and tensions surrounding refined products.

Once readily available stocks are truly depleted, the problem would no longer be merely one of crude oil prices, but one of the physical availability of diesel, jet fuel, and distillates.

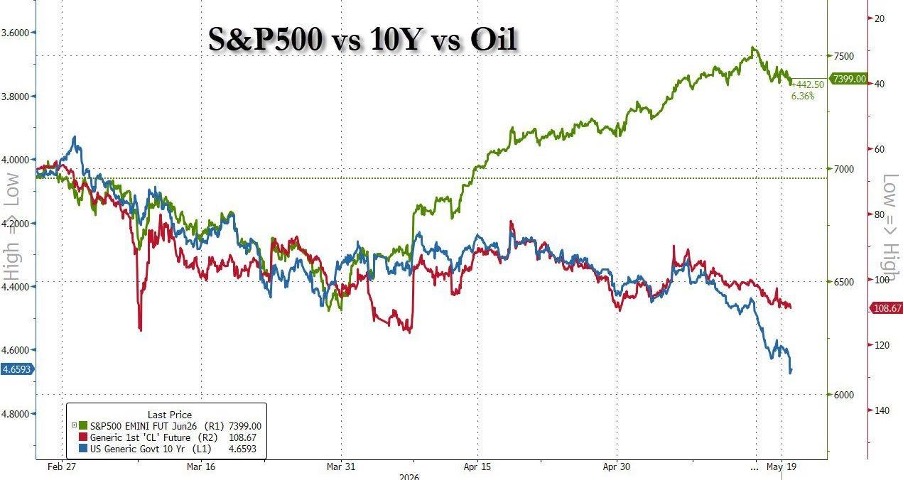

And as this energy crisis gradually takes hold, another sign is becoming increasingly difficult to ignore: the growing divergence between the stock and bond markets.

The S&P 500 continues to hover near its highs, driven by speculative flows, gamma-driven flows, and extremely aggressive investor positioning. At the same time, however, long-term U.S. interest rates continue to rise, while oil remains structurally tight.

Historically, this type of divergence between stocks, bonds, and commodities rarely occurs during periods of sustained stability. The bond market is beginning to send a very different message from that of the stock indices: more persistent inflation, a deficit that is harder to finance, rising costs of capital, and growing pressures on global liquidity.

And this is likely where the signal for gold consolidation becomes particularly interesting.

As was the case before 2008, gold today seems to be reacting less to simple inflation than to a gradual strain on the quality of global liquidity and on confidence in the sovereign collateral system. Before the financial crisis, gold had begun to diverge downward well before equity markets truly recognized the mounting stress in the system.

Even today, stocks seem to be ignoring much of the message sent by:

- long-term interest rates,

- bond spreads,

- energy,

- and now gold itself.

In other words, the real risk may no longer be just higher oil prices. The risk is that a prolonged energy shock will gradually expose much deeper liquidity strains in the global financial system — just as began to emerge before 2008.

Reproduction, in whole or in part, is authorized as long as it includes all the text hyperlinks and a link back to the original source.

The information contained in this article is for information purposes only and does not constitute investment advice or a recommendation to buy or sell.