The oil market is currently focusing on the wrong metrics. As is often the case during periods of transition, attention is centered on visible volumes — the so-called “lost barrels” — while the true disruptive factor lies elsewhere, far more insidious: time. As long as the disruption is perceived as short-lived, the system remains stable. Prices adjust, flows reorganize, and market participants bide their time. But as soon as the outlook becomes unclear, and the duration of the disruption ceases to be manageable, the nature of the problem changes. We are no longer talking about a tight market, but about a system that is beginning to crack.

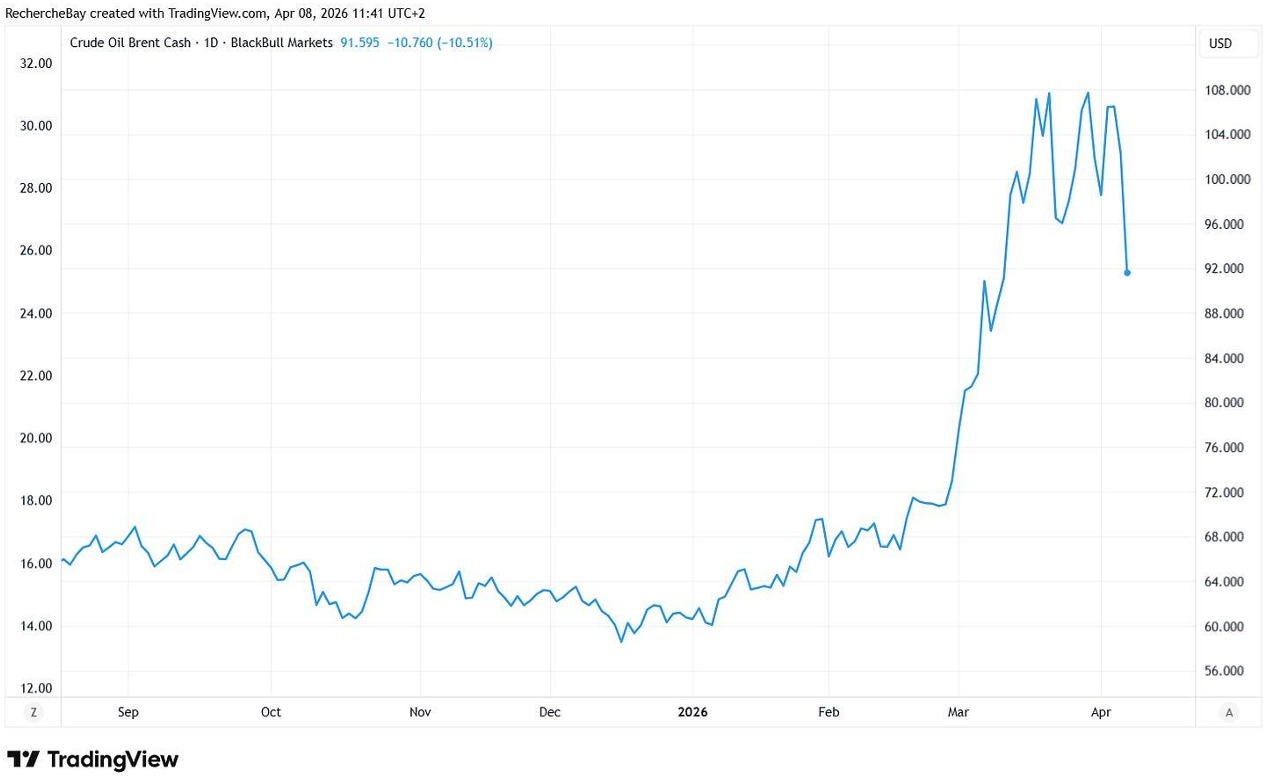

Last night, in fact, gave the market the opposite illusion. In just a few hours, oil prices plummeted by nearly 20%, triggered by a political sequence — a message from Trump referring to “constructive” discussions, followed by a verbal agreement for a 15-day ceasefire.

The market immediately interpreted this as a de-escalation, and thus as a rapid return to normal trade flows. But this reaction is typical of a market that confuses media hype with physical reality.

Because nothing, absolutely nothing in these announcements solves the core problem. A temporary ceasefire does not repair damaged infrastructure, does not instantly secure shipping routes, does not eliminate insurance premiums, and above all, does not restore visibility on future flows.

This is where the bakery analogy helps us understand what is really at stake. In a bakery operating normally, the baker receives his flour every morning at a set time. His entire business relies on this certainty. If a delivery is missed one day, he adapts: he produces a little less, notifies his customers, and then makes up for it the next day. This is a one-off shock, one that can be absorbed.

But if he is told that the flour will return… without being able to specify when, the situation changes immediately. He reduces his production, raises his prices, and becomes more cautious. His customers, for their part, begin to anticipate: they buy more than necessary and change their habits. Very quickly, the problem becomes a matter of trust rather than available quantity.

And if, in a third scenario, he is told that deliveries could resume as early as tomorrow, but that the truck has been damaged, the road remains uncertain, transportation costs have risen sharply, and no regularity is guaranteed, then the system does not return to normal.

Flour supplies may return temporarily, but trust is not so easily restored. The baker continues to play it safe, customers remain cautious, and prices stay high and volatile.

This is precisely the situation facing the oil market today. The ceasefire acts as a promise of resumed flows, the opening of the Strait of Hormuz as a temporary logistical reopening, but nothing guarantees continuity.

The strait has become a wild card, not because it is permanently closed, but because its ability to remain open in the long term is uncertain. Added to this is an even deeper uncertainty, linked to the very state of the infrastructure.

Strikes on oil and petrochemical sites do not merely destroy capacity at a given moment; they also make their return to service unpredictable. Each damaged facility becomes an additional time variable, an uncontrolled delay in a system that relies precisely on the regularity and reliability of flows.

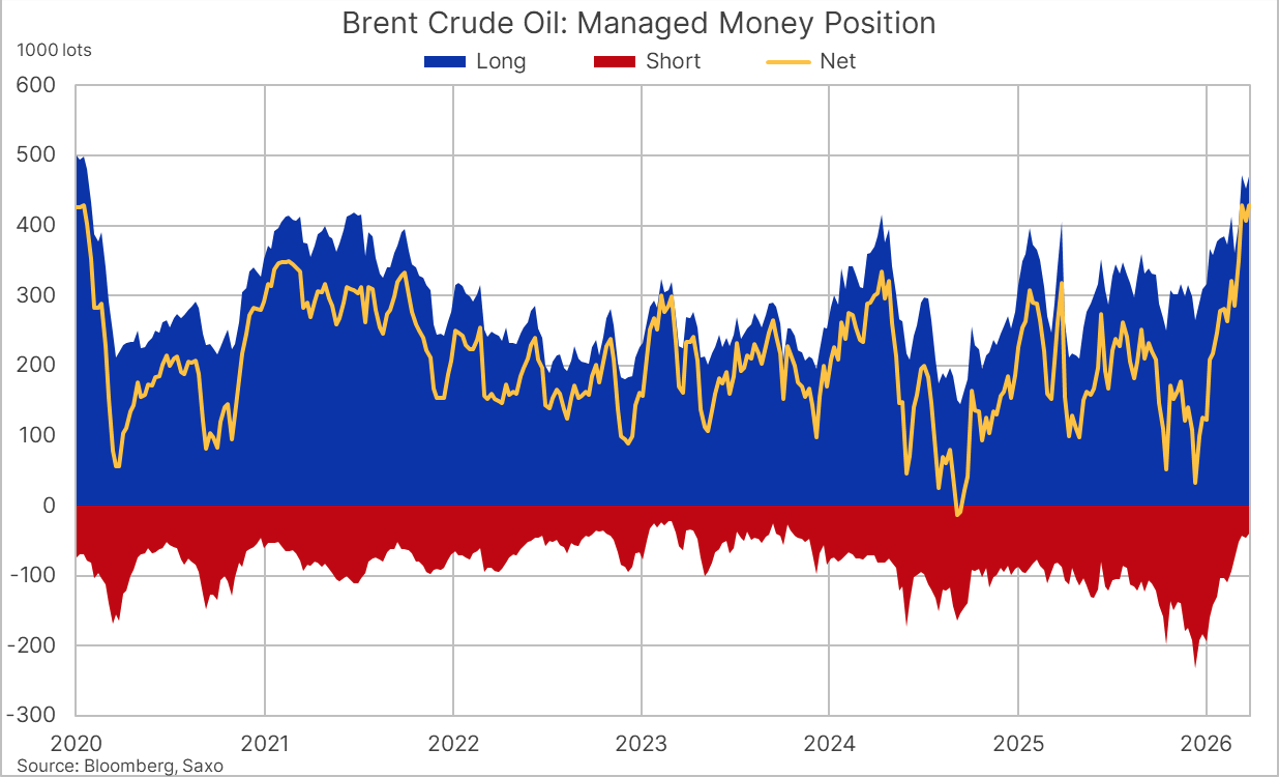

The sharp decline observed is therefore less a fundamental adjustment than a repositioning movement. The market was heavily exposed to long positions, built on the assumption of a lasting supply shock.

The sudden reversal in the market narrative triggered a classic cleansing process: long positions must be unwound, stop-loss orders are triggered, and market participants reduce their exposure. This flush of long positions can be rapid and chaotic, giving the impression of a regime shift, when in fact it is often merely a technical adjustment in a market with limited liquidity.

But once this cleansing is complete, the market is left facing an unchanged reality. Supply flows remain uncertain, infrastructure is weakened, logistics routes are under strain, and confidence in the system’s continuity has been deeply eroded. In other words, the current decline solves nothing; it merely reconfigures short-term positioning.

From this point on, the price of oil ceases to be a simple function of supply and demand. It becomes a risk premium on uncertainty — logistical, industrial, and geopolitical uncertainty. And this premium can be triggered abruptly as soon as the market realizes that the problem has not disappeared, but has simply been masked by a temporary narrative. As is often the case, the market treats the symptom and ignores the underlying structure. It reacts to the announcement but does not price in the duration. Yet, in a system based on continuous flows, it is not the interruption that is fatal — it is the impossibility of knowing when, and under what conditions, they will actually resume.

This is where we must bring in one final, often underestimated factor: the power of the derivatives markets. In the short term, it is these markets that set the visible price, regardless of the underlying physical reality. They can amplify price movements, trigger dramatic crashes, and, above all, trigger sell-offs that have nothing to do with fundamentals.

This phenomenon is nothing new. Those who follow the silver market have been accustomed to it for years.

The silver market offers a particularly illuminating precedent. For years, its price remained largely constrained by the structure of the futures markets: recurring sales of futures contracts stifled every attempt at a rise, even as the physical market was already showing signs of strain. This mechanism maintained a form of artificial price anchoring, in which “paper” liquidity dominated the reality of physical flows. But such a regime could not be sustainable.

Since last year, we have been witnessing precisely the end of this phase of control: the technical resistance levels that had built up over more than a decade were breached one after another, not as a result of a mere speculative surge, but because pressure from the physical market eventually prevailed. The imbalance between growing real demand and a price kept artificially low has finally been resolved, leading to a sharp price surge and a shift in the market dynamics. This movement took years to build, amid relative public indifference, but it perfectly illustrates what happens when the “paper” price can no longer contain physical reality — a process slow in its gestation, but rapid and chaotic in its expression.

The difference today with oil is speed. Whereas the silver market took years to reveal these tensions, oil — due to its universal use and central role in the global economy — cannot absorb these imbalances for nearly as long. Derivatives markets can contain, distort, or delay the signal — but they cannot cancel it out indefinitely. And the longer the gap between the “paper” price and the reality of physical flows persists, the more brutal the final adjustment has the potential to be.

As is often the case, the market today gives the illusion of control. But beneath the surface, the mechanisms of imbalance continue to accumulate. And when the reality of flows reasserts itself, it does not happen gradually — it happens in fits and starts, in movements that can only be explained by the structure of the derivatives markets.

Reproduction, in whole or in part, is authorized as long as it includes all the text hyperlinks and a link back to the original source.

The information contained in this article is for information purposes only and does not constitute investment advice or a recommendation to buy or sell.