Global gold production has never been higher than it is today, and yet gold prices are reaching record highs. In 2025, production exceeded 3,600 tons. This apparent paradox can be explained by sustained structural demand, driven primarily by central banks, institutional and retail investors, and, to a lesser extent, by the jewelry and technology sectors.

However, the supply side appears more fragile than production levels suggest. Since 2018, global production has tended to stagnate, while the sector faces a deep exploration crisis. Major discoveries have become increasingly rare over the past decade, and developing a new deposit from discovery to production generally takes between fifteen and twenty years.

The consequences of this exploration deficit will not be immediate, but supply pressures could become apparent within the next decade. In this context, is the gold market heading toward a shortage?

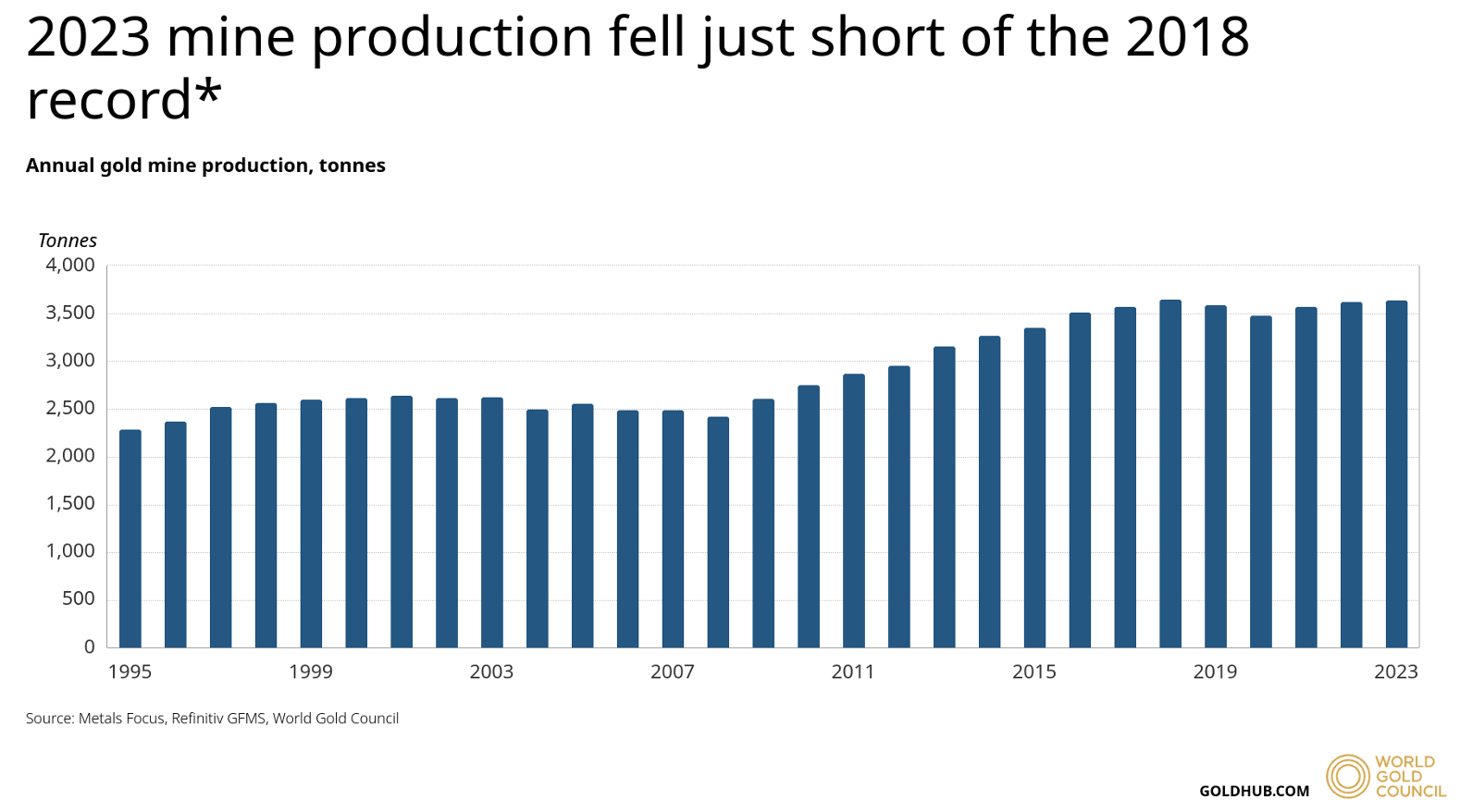

Mining production at an all-time high

According to the World Gold Council, global gold production reached 3,671 tons in 2025, setting a new all-time record. The previous record stood at 3,663 tons in 2018.

Graphic source: Supply | World Gold Council

This record level is actually part of a long-term trend. Following a period of stagnation between the early 2000s and 2010, the sharp rise in gold prices led to a massive influx of investment in new mining projects. Exploration budgets thus increased tenfold, rising from approximately $1 billion in 2000 to nearly $10 billion in 2011.

This influx of investment helped increase annual gold production by more than 1,000 tons. However, the plateau reached since 2018, at around 3,600 tons, now appears difficult to surpass, even as gold prices are projected to reach historic highs.

A reduction in exploration spending

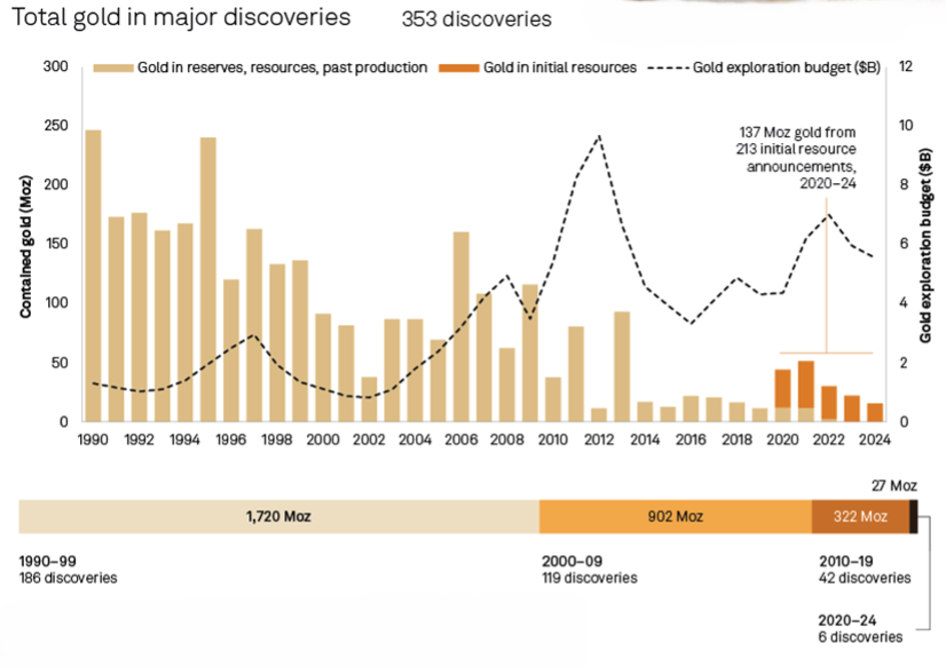

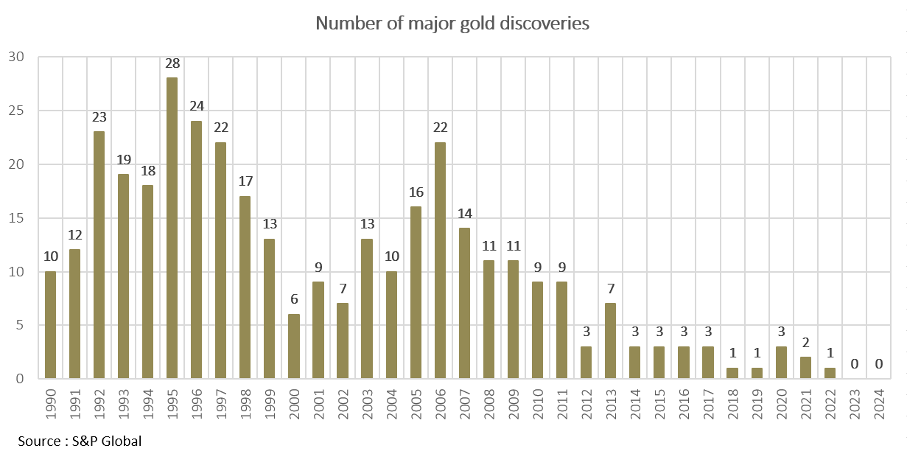

Since the 2000s, gold production has been following a dual trend that is cause for concern. On the one hand, there is a scarcity of major discoveries and a decline in available resources. These are currently estimated at approximately three billion ounces, representing nearly 25 years of production at the current rate. They fall into three distinct categories:

- economically recoverable reserves, still in the ground;

- geologically identified resources, but whose economic viability has not yet been established;

- a marginal fraction of past production, already mined, which represents only a negligible portion of the total.

Compounding this decline in resources is a sharp drop in exploration investment. Budgets allocated to this area fell by 15% in 2023, then by 7% in 2024, despite the sharp rise in gold prices. This anomaly reflects a structural disengagement from the sector rather than a mere cyclical adjustment.

Source: New finds remain scarce despite gold from major discoveries at 3 Boz | S&P Global

The impact on reserve replenishment is already evident. According to S&P Global, “no major discoveries occurred in 2023–2024.” Since 2020, “only six major discoveries have been made, contributing a total of 27 million ounces (Moz) in reserves and resources.” Furthermore, “recent gold discoveries have become increasingly scarce and smaller, with an average size of 4.4 Moz in 2020–2024, down from 7.7 Moz in 2010 to 2019.”

In total, discoveries made since 2020 account for barely three months of annual global production, underscoring the severity of the ongoing exploration crisis and the threat it poses to future market supply.

What impact does this have on the price of gold?

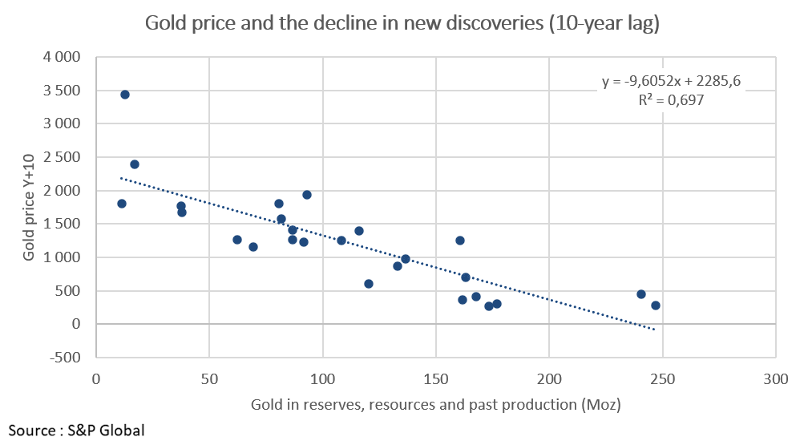

Over the past twenty years, the price of gold has shown a negative correlation with the pace of new discoveries. This correlation is particularly pronounced, with a lag of about ten years — the time it takes for discoveries to gradually translate into actual production. The lack of major discoveries in recent years thus helps explain, at least in part, the significant rise in prices observed recently.

Given the scarcity of new deposits, mining companies are prioritizing the expansion of existing sites. In 2024, so-called “brownfield” exploration — conducted around mines already in operation — accounted for 80% of exploration spending. This choice reflects a growing difficulty in exploring new territories rather than mere financial prudence.

The cost of exploration per ounce of gold bears this out. It has risen from around $100 in the 2010s to an estimated $1,000 to $3,000 today. Even when a deposit is identified, only 10% of discoveries contain enough gold to justify bringing the site into production. Added to this are increasingly long delays in obtaining permits, and projects that are often located in geographically isolated areas.

The United States and Canada, which have historically been at the forefront of gold exploration, are seeing their ability to open up new fronts diminish. A resurgence in exploration in other regions could theoretically offset this decline. China is often mentioned in this context, but it remains a net importer of gold despite already significant domestic production, which limits the scope of this scenario.

Mining companies' profitability on the rise

Operating mines are currently benefiting from a significantly more favorable environment than they were a few years ago. In 2022, a significant number of mining companies were struggling because gold prices were too low to cover their costs. Since then, the sharp rise in prices has restored significant financial flexibility across the entire industry.

According to S&P Global, “margins are expected to grow at a compound annual growth rate (CAGR) of 18.41% in the United States and 14.12% in Canada.” These projections, however, assume the absence of an oil shock — an assumption being put to the test by the current situation. Yet the main cost items for mining companies — such as labor, energy, and maintenance — are structurally inflexible and difficult to reduce.

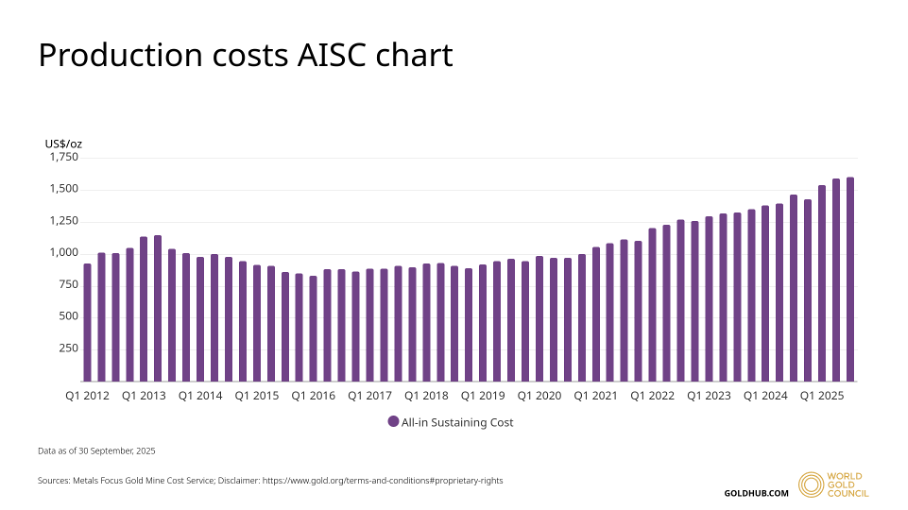

Furthermore, the difficulty of extraction is continuously increasing. Declining gold grades in mined deposits and rising site maintenance costs are weighing on productivity. Since 2015, soaring production costs have significantly slowed the expansion of global production.

Source: AISC Gold | Gold Cost Curve | World Gold Council

The sharp rise in prices, particularly since 2025, could certainly generate sufficient margins to revive exploration. But this short-term improvement in profitability faces a deeper structural constraint: the lack of sustainable exploration, which poses a risk of tightening supply in a market that absorbs nearly 5,000 tons of gold each year.

Ultimately, only companies with the most profitable assets and sufficient reserves will be able to grow sustainably. While most players currently favor organic growth by optimizing or expanding their existing sites, the scarcity of new discoveries could force them to turn more toward external growth. The risk, of course, is that the sector will consolidate without resolving the structural shortage of reserves.

The major mining companies (Newmont, Barrick, Agnico Eagle) have, in fact, already largely adopted this strategy, as acquiring identified reserves is often faster and less risky than discovering them.

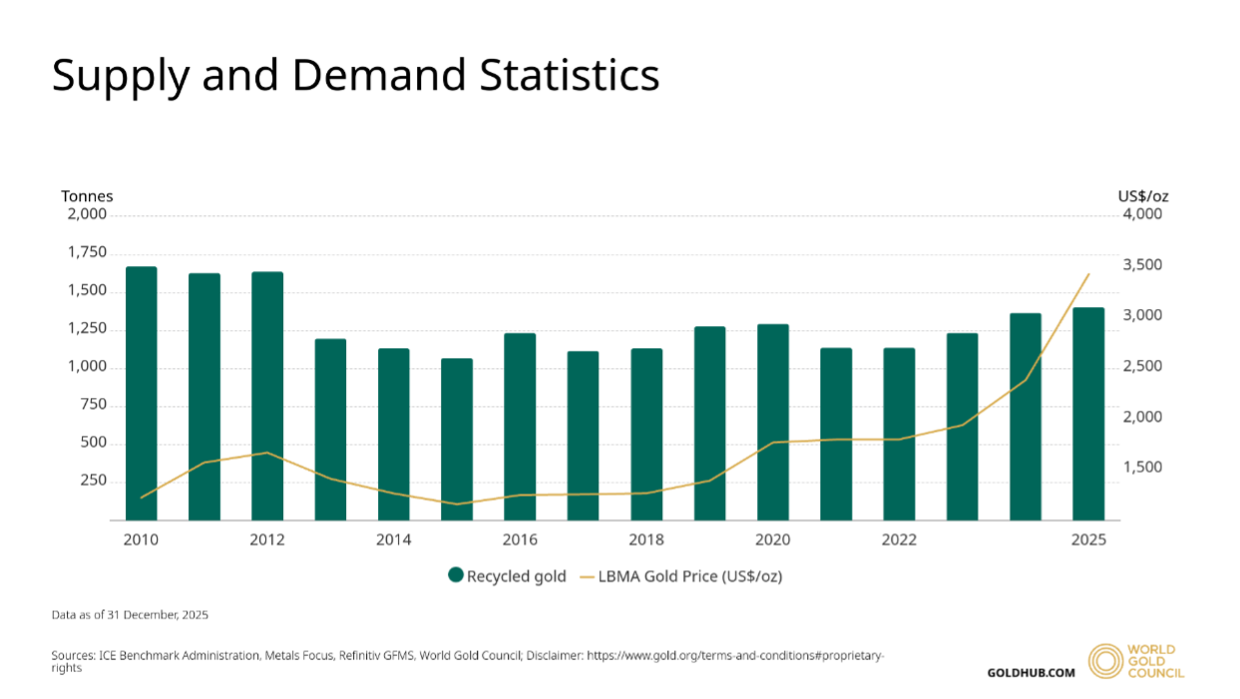

Gold resales are plateauing

Despite the sharp rise in gold prices in recent years, the volume of recycled gold has remained remarkably stable. In 2025, resales accounted for 28% of total supply, or approximately 1,400 tons. This figure is lower than the peak reached in 2010, which exceeded 1,670 tons.

Source: Gold Demand & Supply by Country | World Gold Council

Some might have expected that rising prices would prompt gold holders to sell off their holdings en masse. This has not been the case. This reluctance to sell reflects an underlying trend: gold holdings tend to be held for the long term, or even indefinitely. The metal is withdrawn from the market almost systematically, thereby reducing the supply of recyclable metal available to the market.

In this context, resales cannot serve as a buffer against sustained demand. A structural crisis in gold exploration and production would therefore have direct and tangible consequences for the availability of the metal.

Gold: an essential metal for technology

In 2025, technological demand accounted for 6.5% of global gold demand. While this share may seem modest, it encompasses highly critical applications. 84% of the gold used in this segment is destined for electronics.

Gold owes this role to its exceptional physical properties. It conducts electricity with remarkable efficiency, does not oxidize, and remains stable in extreme environments. These characteristics make it irreplaceable in the most sensitive components, such as connectors, microcircuits, and precision contacts. Gold is thus found in smartphones, computers, satellites, electric vehicles, and medical equipment.

Gold is therefore not limited to being a financial asset or a simple store of value. It is also a strategic material, for which no substitute currently possesses all the properties necessary for technological applications. The expected growth of the technology sector over the coming years could therefore generate new demand.

Conclusion

The gold market is undergoing a transformation that remains largely unnoticed. The sharp decline in the number of major discoveries raises a critical question: will mining companies be able to secure tomorrow’s gold production?

The sharp rise in prices does not seem, for the time being, to be enough to boost exploration budgets or spur new large-scale projects. Several factors explain this reluctance.

On the one hand, the continuous rise in costs and production difficulties over the past decade has eroded the incentive to expand exploration. On the other hand, the growing complexity of remaining deposits, combined with stricter regulations and higher exploration costs, has significantly slowed the pace of exploration.

While rising prices improve mining companies’ margins, the current energy crisis and inflationary pressures are already eroding part of them. In this context, industry players are prioritizing the expansion of existing sites — an organic growth strategy that nevertheless shows its limitations in the long term — at the expense of riskier and more costly “greenfield” projects.

The lack of major discoveries since 2023, combined with the diminishing potential of known deposits, confirms the gradual drying up of gold exploration. This phenomenon has likely contributed, with a certain time lag, to the price increases observed in recent years.

If this trend continues, the very structure of global gold supply could be undermined, calling into question the balance of a market that absorbs nearly 5,000 tons of the metal each year.

Reproduction, in whole or in part, is authorized as long as it includes all the text hyperlinks and a link back to the original source.

The information contained in this article is for information purposes only and does not constitute investment advice or a recommendation to buy or sell.