The conflict in Iran reminds us that the world has truly entered a new era. The upcoming meeting between China and the United States in April seems, more than ever, to crystallize growing geopolitical tensions. The recurrence of wars is accompanied by persistent inflationary risks and a profound redefinition of global balances.

Faced with the shock caused by the war in Iran, should we expect a return of inflation? How might financial markets and gold prices react? Will the dollar manage to maintain its position, and how far could the economic consequences extend? We analyze the ongoing shock.

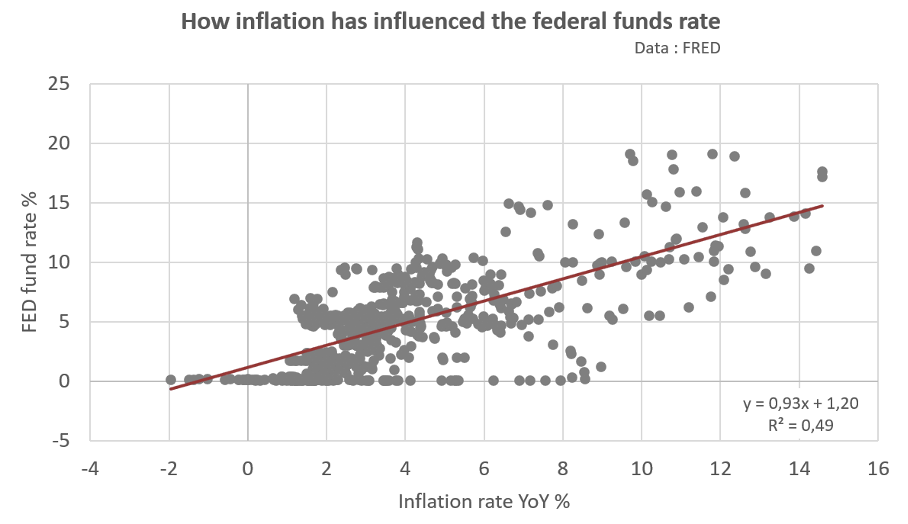

Could inflation start rising again?

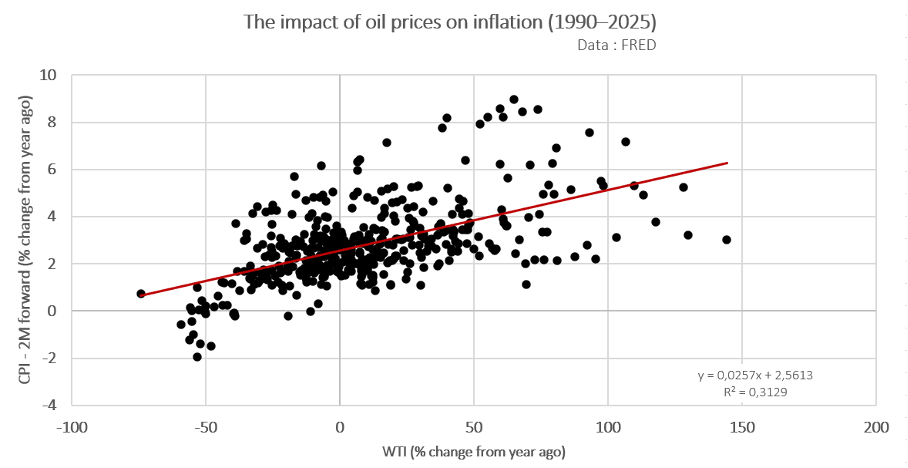

Despite technological advances in recent decades, our economies remain largely dependent on hydrocarbons. Since the 1990s, for example, we have seen that the impact of oil prices on inflation is strongest around two months after a rise in the price per barrel.

A sustained rise in oil prices, which have increased by nearly 40% over the past year, could therefore lead to inflation significantly above 2%, with a target likely to be between 3% and 4% initially. Given that inflation is already above 2% in the United States, the risk of a new inflationary surge could be more pronounced than in 2022 (due to the heteroscedastic and partially autocorrelated nature of inflation). But for now, maritime freight rates are only experiencing a limited rebound, which is preventing inflation from spreading rapidly.

However, this scenario depends largely on the duration of the ongoing conflict in the Middle East. This is because a rapid rebound in oil prices over a period of four to eight weeks tends to trigger a mechanical rebound in cyclical inflation. Conversely, a rapid de-escalation of the conflict would eliminate much of the inflationary risk within two to three months.

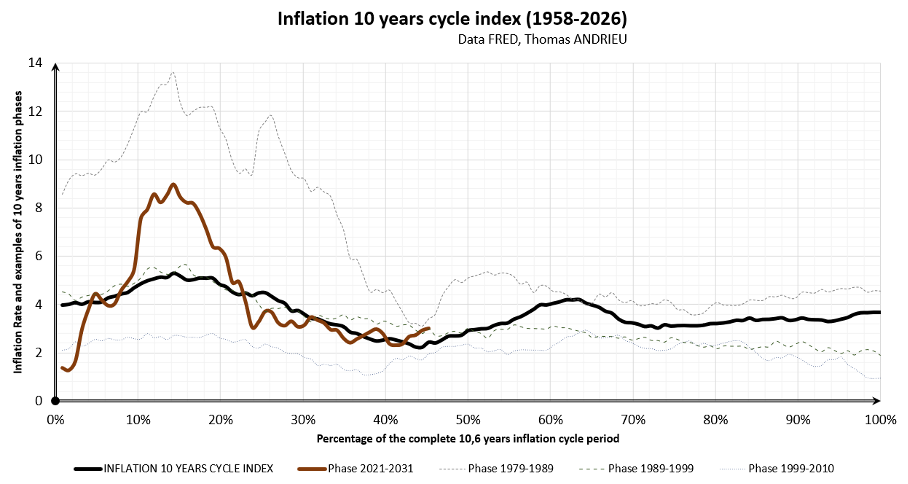

More broadly, this phenomenon may be part of a characteristic manifestation of the long economic cycle, or Kondratiev cycle. The upward phase of this cycle is generally characterized by more frequent conflicts, higher inflation, accelerated innovation, and increasing scarcity of capital.

Even more striking, at least by coincidence, is the symmetry between the recent trajectory of inflation and that observed in the 1970s. As early as 2022, we warned of the risk of a second inflationary phase starting in 2026, linked to the trajectory of the main cycle observable on inflation, lasting approximately ten and a half years.

Although this second wave is often more moderate than the first, it can nevertheless pose a significant threat, particularly during the upward phases of the long economic cycle. Finally, the persistence of higher unemployment in the United States and Europe could limit a return to inflation at this stage.

What reactions can we expect on the stock markets?

We have shown that the economic threat posed by the conflict in Iran depends above all on its duration. The already sharp rise in oil prices suggests further pressure on inflation. In the event of a prolonged conflict (Polymarket currently anticipates a possible extension until April or May), a rise in inflation would have mechanical effects on many macroeconomic variables.

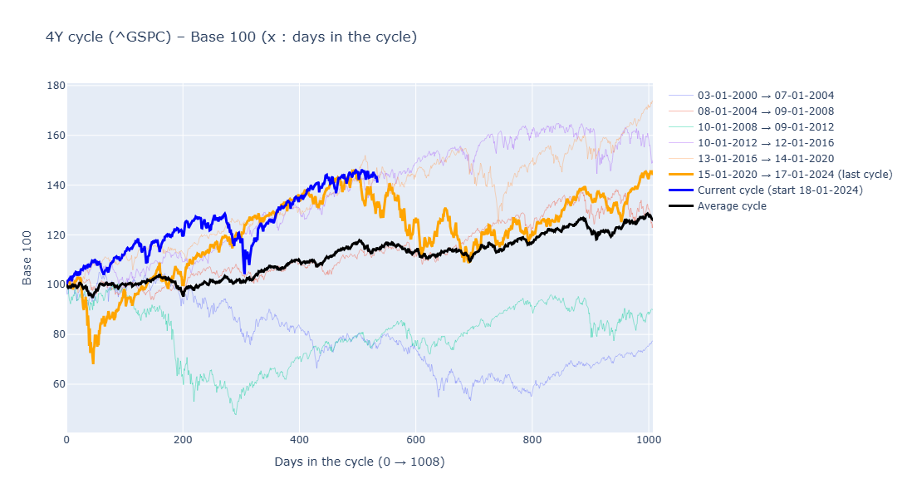

In recent weeks, we have already warned of the risks of market consolidation, due in particular to the US presidential cycle and the Kitchin cycle, which is already observable in bitcoin. It is indeed common to see a period of stagnation in stock market indices during midterm election years in the United States, as suggested by the chart below.

Furthermore, a certain parallel can be drawn with the Kitchin cycle, which lasts around 3.5 years. In both cases, these dynamics could lead to a period of uncertainty potentially extending until the midterm elections. The sector rotations observed at the beginning of the year and the rise in volatility seem to support this scenario.

Data source: yfinance

In this context, we will pay particular attention to the response of central banks. If inflation rebounds, key interest rates could remain high for longer, or even be raised. Such a prospect could support a period of market consolidation lasting several months. Conversely, if inflation proves to be transitory and the labor market continues to deteriorate without a recession, this downward bias could be limited.

Finally, we are seeing a gradual return to normal for the S&P 500/gold ratio. In an extreme scenario, it would not be impossible to see the S&P 500 return to a level close to the price of gold, as has been seen in the past.

The gold price at the heart of expectations

There is generally some confusion about how the gold price behaves during periods of war, inflation, and rising interest rates. Gold tends to benefit from a weakening dollar or escalating geopolitical tensions. To a certain extent, one might even question the role that rising gold prices could play in weakening the dollar and reflecting emerging geopolitical tensions.

Consequently, the trajectory of gold prices depends mainly on several factors depending on the time horizon considered: the evolution of the stock markets in the very short term, that of interest rates in the medium term, and that of inflation in the longer term. We have observed that the shock linked to Iran has triggered widespread selling of most assets, including gold and bonds. The return of a period of market stress could therefore be accompanied by increased volatility in gold prices.

Gold prices are relatively insensitive to short-term inflation, although there is a negative correlation with real rates, particularly when they fall. This short-term phenomenon can be explained by the fact that while inflation contributes to lowering real rates, the anticipated rise in key rates can offset or even exceed the effect of the inflationary shock.

While gold appears to be less sensitive to short-term inflation, data shows that inflation has a more positive effect on its performance about a year and a half after the onset of an inflationary wave. This phenomenon is particularly noticeable when inflation exceeds 6%. On average, inflation therefore tends to support the rise of gold prices in the long term, but this effect is much less pronounced in the short term.

After a considerable rise in the price of gold in 2025, followed by a further upward trend in February, we note that the war in Iran has caused a period of stagnation. This could continue if we see a rebound in inflation and the prospect of stabilization or even an increase in interest rates.

We are also seeing a decline in trading activity in gold, marked by a decrease in the number of open positions since the end of February.

The hypothesis of a widespread revaluation of raw materials

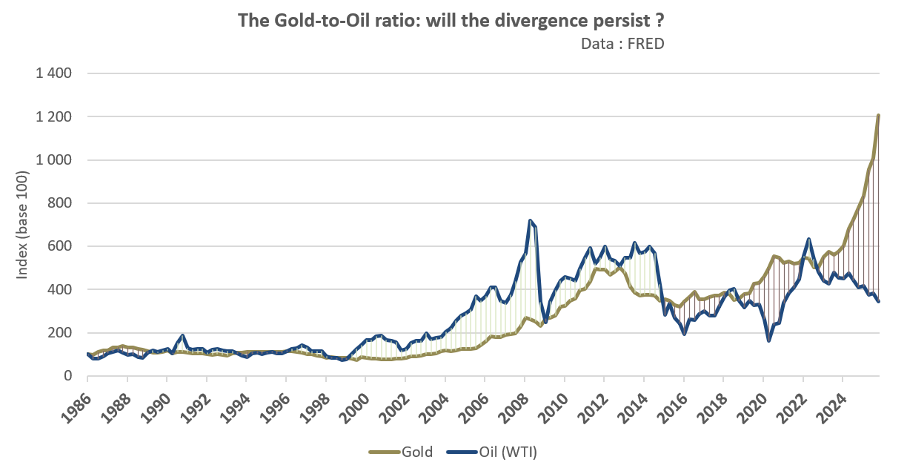

Since the end of World War II, gold and oil have shown a certain degree of convergence. Historically, the gold-oil ratio has fluctuated between 10 and 30. However, in 2020 and more recently in 2025, this ratio skyrocketed to nearly 75. More broadly, gold often seems to precede a more generalized rise in commodity prices.

Thus, the hypothesis of a renewed interest in commodities appears entirely plausible. Since January 1, wheat prices have rebounded by more than 20% on the CBOT, while aluminum prices have risen by around 14%. This significant recovery in commodities suggests that inflationary pressures are not yet over.

If inflation returns to around 3%, the US Federal Reserve may decide to keep its key rates stable. However, if inflation rises above this threshold and commodity prices continue to rise over several quarters, further rate hikes cannot be ruled out. That said, this outlook will largely depend on the duration and scale of the conflict.

Can the dollar remain a safe haven currency?

The war in Iran undoubtedly marks a return of the United States to the international stage, helping to isolate another strategic partner of China.

In the wake of the conflict, the dollar index rebounded, but without returning to its levels of a year ago. At the same time, Treasury bonds do not seem to be fully playing their role as a safe haven. The yield on the 10-year T-Note rose by nearly 20 bps during the first week of the conflict.

Geopolitical clarity could come during the meeting between Donald Trump and his Chinese counterpart Xi Jinping, scheduled to take place in China from March 31 to April 2. A preliminary meeting could also be held in Paris between the US Treasury Secretary and the Chinese Vice Premier, a sign of particularly important financial stakes.

Since the start of the war in Ukraine, we have seen a broader trend towards diversification away from the dollar. Central banks now hold more gold than US Treasury bonds in their reserves. The mistrust of the dollar by certain countries is reflected in significant gold purchases by central banks.

Beyond market developments and inflation, we will be paying particular attention to the behavior of central banks in the coming quarters. New gold purchases could play a decisive role in keeping the precious metal at high levels.

Above all, it should be remembered that the already high level of interest rates, particularly in the United States but also, to a lesser extent, in Europe, could further increase the burden of already significant debt. At the same time, the need for technological, military, and financial spending has never been greater, clearly illustrating the power of long economic cycles.

Conclusion

The world is once again facing the threat of a return to inflation. The extent of this risk will depend above all on the duration of the conflict in the Middle East. A prolongation of hostilities over two to three months could have more or less lasting effects on prices. In addition, changes in maritime freight costs and raw material prices in general will be a determining factor in the intensity and speed of the potential inflationary shock.

These events share certain characteristics with the upward phase of the long economic cycle described by Kondratiev nearly a century ago. In particular, we can observe, at least coincidentally, the importance of the timing of inflation in relation to these long-term economic cycles.

Furthermore, this conflict comes as the US midterm elections approach, following a particularly favorable upward phase in the short economic cycle. The return to a volatile environment could be long-lasting if the conflict continues for at least a few weeks. It is therefore possible that a period of uncertainty could take hold in the markets until the fall.

The decline in open positions on gold at the end of February already reflects a climate of caution. Beyond the role of inflation and interest rates in the evolution of the gold price, it will be particularly interesting to observe the evolution of the dollar and the strategy of central banks.

The scale of global debt levels, against a backdrop of potential inflationary pressures and rising public spending, is also contributing to heightened tensions. The upcoming meeting between the United States and China could provide some major clarity.

Reproduction, in whole or in part, is authorized as long as it includes all the text hyperlinks and a link back to the original source.

The information contained in this article is for information purposes only and does not constitute investment advice or a recommendation to buy or sell.