For those uninitiated in finance, a "short squeeze" refers to a situation where an individual or legal entity sells an asset in the future without owning it first, in the hope of buying it back later at a lower price in order to make a profit. However, if the price of this asset increases instead of falling as expected, this individual or legal entity is forced to buy it quickly to honor the delivery of their forward sale. This hasty buying movement then contributes to accentuating the rise in prices.

Isn't this precisely what gold prices have been reflecting for several months?

The world's main gold market is the London Bullion Market, where 18.6 million ounces of gold are traded daily. It is an over-the-counter market between members of the London Bullion Market Association (LBMA), managed by 11 major banks considered to be the market makers for the spot market. Some of these banks also manage the forward market and the options market.

On the spot market, the minimum quantities per contract is 5,000 ounces, and delivery must be made within a maximum of two days.

In the forward market, transactions are made in lots of 500,000 ounces for delivery in the future, ranging from 3 months to one year. As for the options market, it allows its holder to buy gold at a fixed price on a given date, without being obliged to do so, in exchange for the payment of a premium. The basic contract is 1 million ounces for delivery that can extend over a period of one week to one year.

In the forward and options markets, traders use leverage because they are initially required to put down a margin deposit representing a small percentage of the total value of the contract. This percentage varies, but is usually around 5%. When the price of gold is volatile, as it is currently, these transactions become extremely speculative and risky, especially if the positions taken go against the direction of the price.

The London gold market is supported by the Bank of England (BoE), which has managed one of the largest gold stocks in the world since 1815.

Although the Bank of England only has 2 gold bars, both on display in its museum, it holds the UK's 310 tonnes of gold reserves on behalf of Her Majesty's Treasury and is the custodian of 400,000 400oz gold bars (each weighing 12.5kg), equivalent to 5,000 tonnes of gold, most of which is held by foreign central banks.

The invention of “unallocated” gold

Peter Hambro is a leading figure at the LBMA. From 1983 to 1990 he was managing director of Mocatta & Goldsmid, one of London’s oldest gold banks, before becoming a director of Montagu, another legendary institution in the precious metals trade. He also co-founded the Anglo-Russian Gold Mining Company. In the 1980s Mocatta & Goldsmid was the USSR’s main interlocutor for gold and silver trading. Peter Hambro comes from a long line of precious metals bankers.

In a surprising interview with Reaction-life on July 4, 2022, Hambro discusses the manipulation of the price of gold through derivatives, calling it a “powder keg.” According to him, it was the Bank for International Settlements (BIS) in Basel, the central bank of central banks, that orchestrated this maneuver, dating back to the London Gold Pool of the 1960s.

“The financial stability offices of the world’s central banks followed the instructions of the BIS to mask the perception of inflation by rigging the gold market. But since central banks cannot be accused of rigging the price of gold, the only way to change the price of physical gold was through the alchemical production of paper gold.”

“With the help of the futures markets and the connivance of the bullion banks—yes, that includes me, since I was deputy managing director of Mocatta & Goldsmid—they managed to create an unshakable perception that the ounces of gold credited to a bullion bank’s bullion account were actually physical gold. And it was much easier. You didn’t have to buy it, store it, or insure it.”

In this interview, Hambro explains the evolution of the London paper gold market and details the workings of his fractional reserve paper-gold system, which has developed from the 1980s to the present day.

The Bank of England and the LBMA are closely linked, particularly through the ultra-secretive London gold lending market, in which central banks lend physical gold to the LBMA’s bullion banks. This global paper gold system allows for an unlimited supply since, as Hambro puts it, governments and central banks and the BIS “can print at will.”

The Gold ETF

The SPDR Gold Shares ETF (GLD) was launched in November 2004 with the World Gold Council sponsorship. This financial product is designed to follow the price of gold and can be bought or sold with a few clicks from a computer. The objective is to divert investors from buying real physical gold to sell them paper-gold instead, entirely virtual.

The statutes stipulate that no one can request an audit of the stocks, nor demand delivery of shares of gold bars purchased online. If we examine Peter Hambro's statements above, this only confirms the strategy secretly implemented by bullion banks since the 1960s.

This financial product has been a huge success, leading to the sale of a considerable number of shares of virtual gold bars. The funds from these sales have allowed the managers to acquire an impressive stock of gold, which is said to have peaked at 3,400 tonnes in 2020. However, it is important to note that these are actually shares equivalent to tonnes of gold. I have never been convinced that these thousands of tonnes of gold exist, even if some of it is actually there.

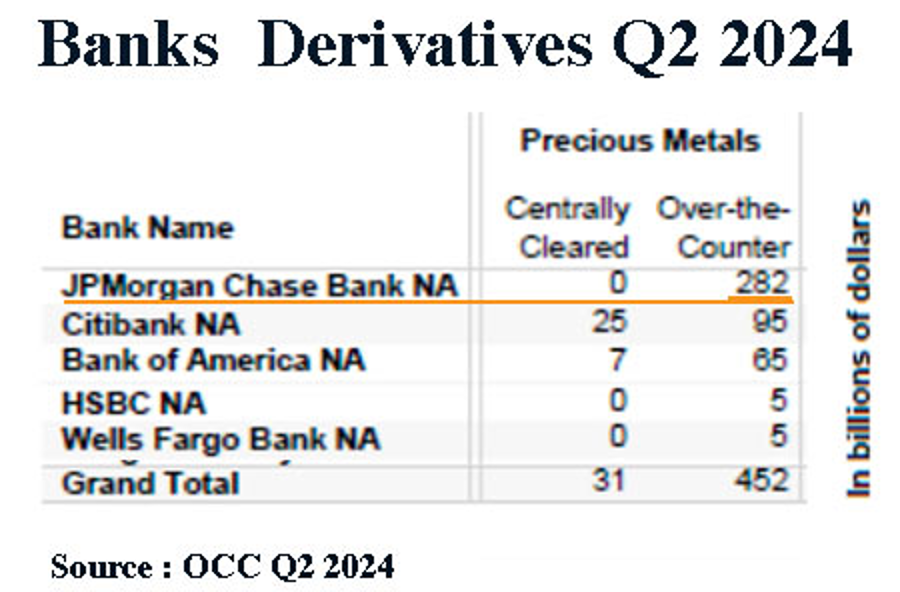

The existing ETF stocks are split between the LBMA, the COMEX and JPMorgan’s vaults, which is the official custodian of this treasure. JPMorgan is also the largest trader and dominant market maker in the paper-gold market and its derivatives, as indicated in the latest report from the Office of the Comptroller of the Currency (OCC).

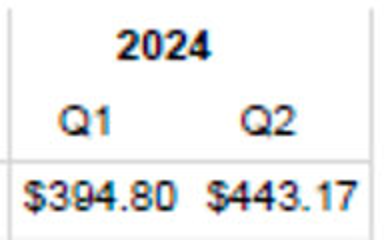

The 12% increase in precious metals derivatives from Q1 to Q2, coinciding with the sudden break of the $2,000 resistance, clearly indicates the emergence of a major problem at $49 billion.

Since gold repeatedly ran into the $2,400 resistance during Q2, if we divide that $49 billion by $2,400, assuming that it is 400oz LBMA bars, this single increase in derivatives in Q2 could equate to about 51,000 12.5kg bars, or 637 tonnes or 20 million ounces.

If all of the $443 billion in precious metals derivatives were gold alone, that would be 5,643 tonnes of gold.

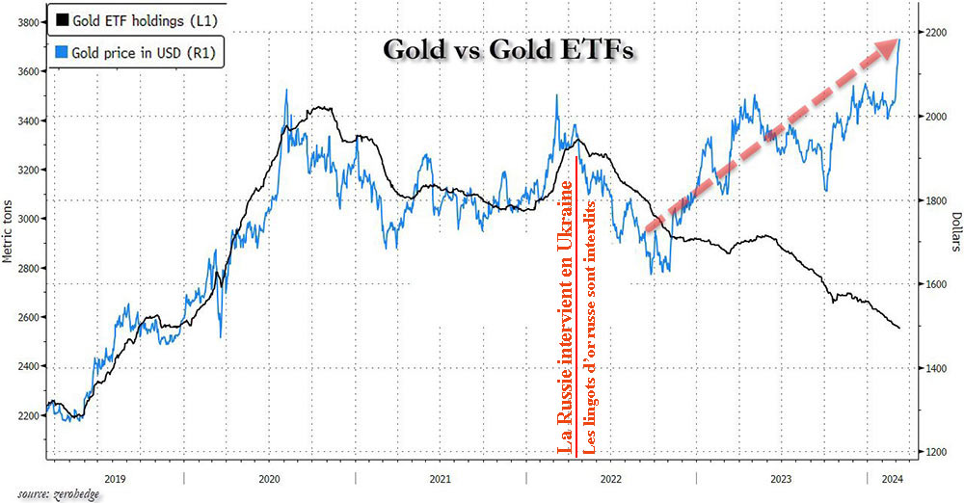

What is particularly striking about the chart above is that since 2020, the reported tonnage of Gold ETFs has been steadily declining, even as the price of gold has soared. Logically, investors and hedge funds are supposed to put their capital into a bull market to ride the trend.

Did the stocks of Gold ETFs have to be delivered in place of the COMEX or LBMA reserves, which were unable to supply the quantities demanded?

The history of ETFs is bound to turn into scandal and bankruptcy, abruptly, at some point.

Basel III Rules

While the Bank for International Settlements (BIS) in Basel had orchestrated the gold prices control for 50 years, it is important to note that it also created the Basel III rules that were implemented in January 2023. To do this, the BIS spent many months untangling a tangle of gold swaps that it had itself created over the previous five decades to contain rising prices. This work was completed in November 2022, just two months before gold was classified as Tier One in bank capital, provided that this gold is not encumbered by any mortgages. And this is where Basel hurts.

Since 1971, and even before, central bank gold has been repeatedly mortgaged and sometimes sold several times by bullion banks, which had leased these bars. This situation had already led to a major systemic shock in 1999, when the LTCM hedge fund sold the Italian Treasury's gold reserves on the market, hoping to buy them back more cheaply. However, Russia's default on its debt caused a sharp rise in the price of gold, forcing the LTCM hedge fund into bankruptcy.

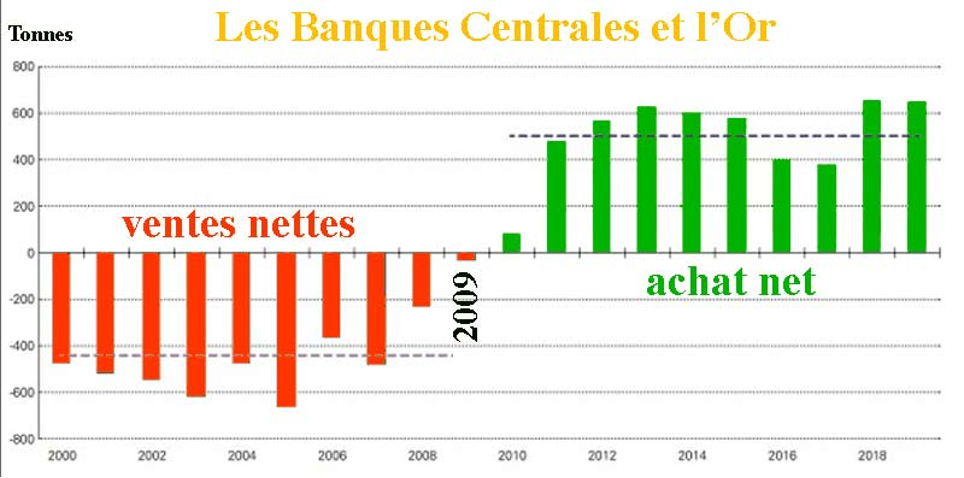

Until the G20 in November 2008 in Washington, where the various states demanded a reform of the monetary system. The G7 central banks had concluded an agreement, the Washington Gold Agreement, which committed them to selling gold regularly on the markets in order to stabilize the rate of fiat currencies.

The year 2009 was a significant turning point. It took time for commitments made earlier to be either fulfilled or reversed. It remains uncertain whether all the bullion borrowed by central banks has been returned to the vaults from which it should never have come, and whether it is truly free of any mortgage.

A bank that holds an unmortgaged gold bar in its vaults sees its bank security rating upgraded. On the other hand, if the bank holds a mortgaged bar, ETF shares or gold positions in futures or options, its rating is downgraded.

Gold moves from West to East

In March 2009, China published an essay entitled “Let’s Change the Monetary System,” in which it proposed a model in which gold and certain commodities would play a role in backing currencies. This idea had been put forward by Keynes at the Bretton Woods conference in 1944.

Since 2009, China has encouraged its citizens to invest in precious metals and has developed the Shanghai Gold Exchange. Unlike Western markets, where transactions can take time, the SGE allows for same-day transactions, although a futures market has also been created.

Since 2009, China required delivery of large quantities of gold purchased on the London Bullion Market. Aware that the bars received could be encumbered by multiple mortgages, it systematically refined them, transforming the 12.5 kg bars into 1 kg bars.

This meant that the old bars lost their identity and the history of their previous owners. The new gold bars, on the other hand, acquired their own identity, which no one could contest any longer.

The Shanghai market has been booming, with volumes steadily increasing since 2009. According to Jan Nieuwenhuijs at the end of 2022, China held approximately 28,054 tonnes of gold, split between the central bank and the private sector. Meanwhile, Russia and India continued to convert their monetary reserves into gold, importing significant quantities of the precious metal.

All of these countries, whether China, India, Russia, Turkey or Singapore, are benefiting from the efforts of bullion banks for years to contain the rise in the price of gold. Moreover, many central banks of less influential countries have also strengthened their gold reserves by liquidating their dollar holdings, following the seizure by the Fed and the ECB of Russia’s currency reserves in 2022.

Since confidence is no longer as it used to be, many countries no longer want to leave their gold in custody at the Bank of England or the US Federal Reserve. They now prefer to demand the delivery of their reserves in order to store their gold on their own territory. Even Austria has demanded the repatriation of its gold.

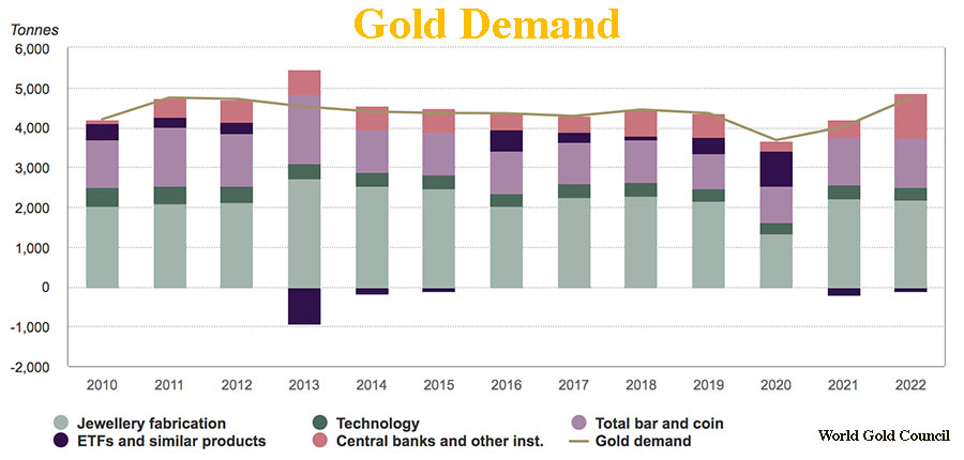

According to the US mining services, the USGS, global gold production reached 3,000 tonnes in 2023, while demand for the previous year was 4,448 tonnes according to the World Gold Council. Central banks acquired 1,037 tonnes of gold, resulting in a deficit of about 1,400 tonnes on the market. In 2022, mine production was 3,100 tonnes, while demand reached 4,741 tonnes according to the WGC, which represented a deficit of 1,600 tonnes.

The chart below shows that demand has almost always exceeded 4,000 tonnes of gold:

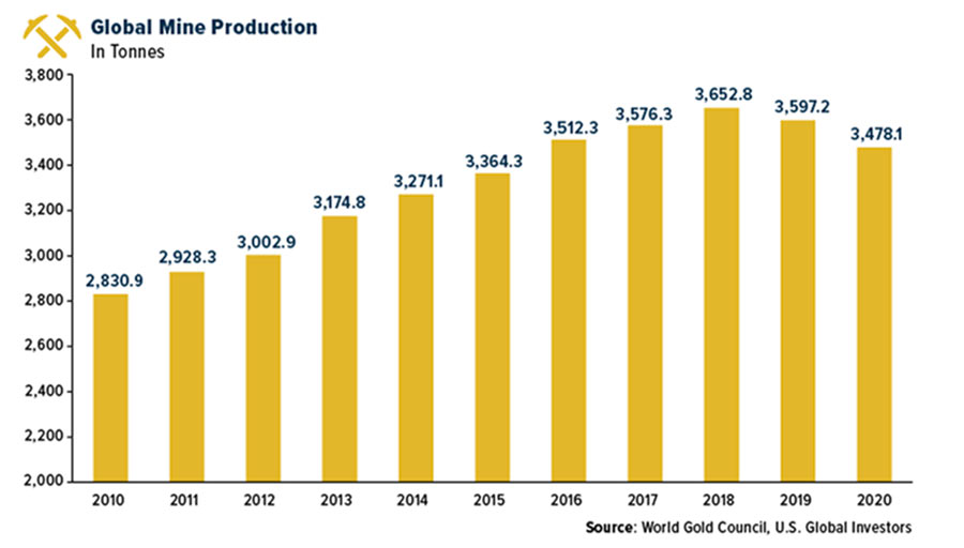

And that mining production has never managed to satisfy demand over the past 12 years.

Deficits of more than 1,000 tonnes have accumulated year after year, which explains the continued rise in the price of gold since its low point in 1999.

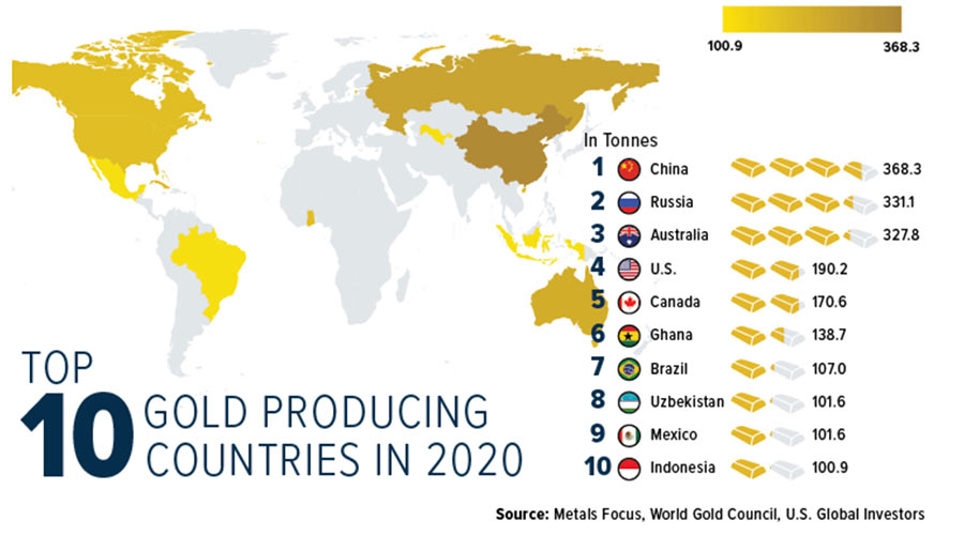

Looking at the map of major gold producing countries below, we see that China and Russia stand out as the two largest producers. Together, they account for 25% of global gold production. Since August 2009, China has banned the export of gold extracted from its mines, which must theoretically transit through the Shanghai Gold Exchange (SGE).

Following the outbreak of war in Ukraine, the US and European authorities imposed various sanctions on Russia. The LBMA and COMEX acted quickly by withdrawing their LBMA approvals from the country's main refineries.

The market therefore has a much larger deficit than the WGC data indicates, to which must be added at least 331 tonnes produced annually by Russia.

Officially, the New York Federal Reserve, which held 12,000 tons of monetary gold in 1973, now holds 6,331 tons, or 507,000 bars in 2024. None of these bars belong to the New York Fed or the Federal Reserve System.

The New York Fed acts solely as a custodian of gold on behalf of various owners, including the U.S. government, foreign governments, central banks, and official international organizations. No individuals or private sector entities are permitted to store gold in this vault.

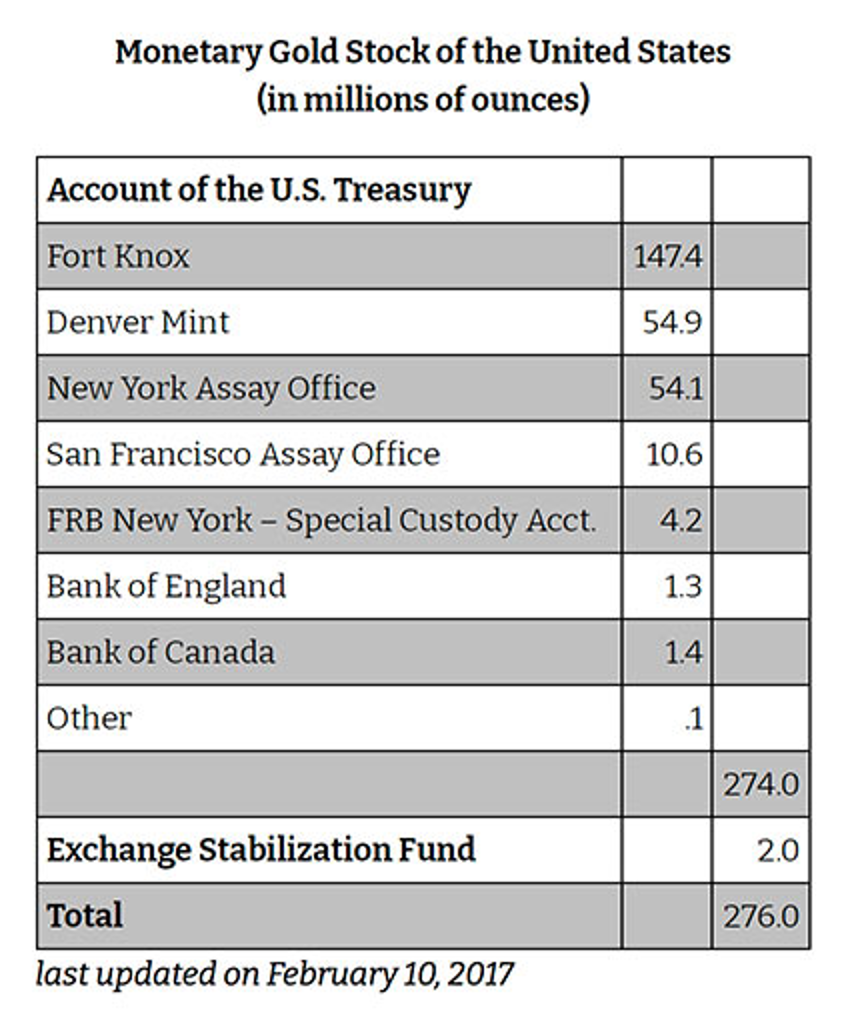

Beside of that, according to an audit conducted on September 24, 1974, Fort Knox officially held 147.4 million ounces of gold, which equals 4,167 tons, with the remainder distributed as follows:

The total monetary gold reserves of the United States stand at 276 million ounces, or 7,824 tonnes, and are still valued at $42.2222 per ounce. That’s $11.7 billion on the books of the US Treasury, when at current prices they would be worth $739 billion.

But in the end, how much does this accounting difference matter when you consider the US debt of $35 trillion, $10 trillion of which matures in 2024, when there is not a cent in the till? They will still have to flood the world with dollars at the push of a computer button, which promises to be the largest quantitative easing (QE) in history.

Do these 276 Moz of gold really exist? Are they free of any mortgage?

It will be recalled that in 2013, when Germany wanted to repatriate 300 tons of gold held by the Federal Reserve Bank of New York, German experts were first forbidden from inspecting their reserves. Then, the Fed announced that this repatriation would take 7 years. In the end, the Bundesbank got its 300 tons of gold back 3 years earlier than expected, but this story raises doubts about the trust that can be placed in the Fed.

It is also important to remember that the Bank of England refused to return 31 tons of gold to Venezuela, arguing that it did not recognize the legitimacy of its president, Nicolas Maduro. More than 4 years later, this gold reserve remains frozen in Britain. This situation raises serious concerns about the solvency of the Bank of England.

The LBMA boasts that it has 8,663 tonnes of gold in its various approved vaults. However, the LBMA does not specify whether this gold is “eligible” or “registered” – that is, whether it is for sale or not – nor who owns it. It is also worth noting that the Bank of England is one of the LBMA’s approved vaults. The 5,000 tonnes of gold entrusted to the BoE by many foreign central banks are not for sale, right? A large portion of the 2,600 tonnes of gold in ETFs is also included in this 8,663 tonne figure, which is intended to impress.

In short, if we add up the 5,000 tonnes of the Bank of England and the 2,600 tonnes of ETFs, from which we should subtract what is Russian, we only have about 1,000 tonnes left, part of which belongs to individuals or legal entities who simply benefit from the security of the vaults.

Is the float actually available for sale on the London Bullion Market limited to a few hundred tonnes?

We remember that Chinese banks have bought some of these vaults. For example, in January 2016, the Chinese ICBC Bank bought the Deutsche Bank vault in London, which has a storage capacity of 1,500 tons of gold. In May 2016, the Chinese ICBC Bank bought the Barclays vault in London, which can store 2,000 tons of gold. And these banks have been very active in this market since they were approved as members of the LBMA.

Is the gold that they have bought and stored in their vaults actually available for sale? I don’t think so.

LTCM bankruptcy to the power of 10?

The deficit that has been accumulating every year for 15 years, and probably even longer, threatens to explode the paper gold Ponzi scheme, which has existed for more than 50 years. The Bank for International Settlements (BIS) cleverly got out of this circus in 2022, two months before the implementation of the new banking safety rules, which require banks to divest themselves of the various forms of paper gold.

While in 2022, central banks acquired a record 1,082 tons of gold, and they bought another 1,037 tons in 2023, followed by 472 tons in the first half of 2024, many central banks have also requested the repatriation of their gold reserves. In a market already in deficit of over 1,000 tonnes per year, one may wonder whether the Bullion Bank Cartel has sold the gold stocks that were secretly leased by the Bank of England and the Federal Reserve.

Doesn’t the rise in the price of gold suggest that the Gold Cartel is trying to buy back the gold it borrowed and sold on the markets?

This huge paper gold bubble is about to burst, and short sellers are caught in a short squeeze. This is the phenomenon that has driven the price of gold steadily higher for the past year and will continue until gold reaches multiples of its current price.

Hold on to your physical gold!

Reproduction, in whole or in part, is authorized as long as it includes all the text hyperlinks and a link back to the original source.

The information contained in this article is for information purposes only and does not constitute investment advice or a recommendation to buy or sell.