Obviously, such a scenario may seem completely unrealistic, and attempting to replicate it is strongly discouraged. However, it remains worthwhile to take a step back and analyze the dynamics at play in the markets.

Refinery closures

Starting in 2020, numerous oil companies closed a large number of refineries, either temporarily or permanently, in the United States, Australia, and Europe (France, the United Kingdom, Norway, Finland, Denmark, the Netherlands, Italy, Portugal, Spain, Croatia, Poland, and Israel). These closures created an artificial shortage of refined petroleum products (gasoline, heating oil, and kerosene), leading to a sustained increase in pump prices worldwide. Since these facilities cannot be brought back online quickly, these price pressures have become entrenched.

In November 2021, at COP26 in Glasgow, the Financial Alliance for Net Zero was launched. All the major banks and insurance companies of the G7 pledged to cease financing the exploration and development of new oil and gas projects. What might have appeared to be a radical decision is, in reality, a continuation of the refinery closures mentioned earlier.

In 2022, the United States, followed by the European Union, banned the purchase of Russian oil and gas as part of sanctions imposed after the outbreak of the conflict in Ukraine. This decision profoundly altered the world global energy balance.

In September 2022, the Russian-German Nord Stream 1 pipeline was destroyed, depriving Europe of direct access to cheap gas. It is worth noting that Nord Stream 2 remains intact and, for several years, has been awaiting potential political approval to begin operations.

At the same time, several European countries banned the installation of new oil-fired boilers. Meanwhile, governments strongly encouraged the development of electric vehicles, in anticipation of an oil shortage and rising prices.

In May 2025, the United States intervened in Venezuela, the country with the largest oil reserves in the world. The likely objective: to deprive China of one of its main oil suppliers.

In February 2026, the escalation of tensions surrounding Iran, notably involving Israel and the United States, rekindled fears of a major conflict, further increasing pressure on global energy markets.

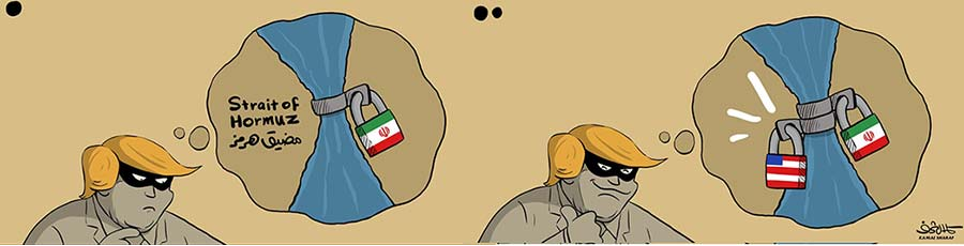

In March 2026, major reinsurance companies began refusing to cover war risks in the region. In practice, this amounts to preventing ships from crossing the Strait of Hormuz, which has become economically and insurably unviable. So it is not just a military decision: financial players have effectively turned off the tap of cheap oil.

Officially, Iran stated that it was restricting passage to vessels linked to the United States, Israel, and their allies.

For the mass media:

Iran closes the Strait of Hormuz…

Trump closes the Strait of Hormuz, via an attempted blockade in the Gulf of Oman.

Without even mentioning the destruction of oil and gas infrastructure in Saudi Arabia (Ras Tanura refinery), in Iran (South Pars gas field), in Qatar (Ras Laffan), in Bahrain (Bapco), in Kuwait (Mina al-Ahmadi), or in the United Arab Emirates…

- March 1: Refinery fire in Ecuador

- March 12: Oil processing unit fire in Texas

- March 23: Refinery fire in Texas

- April 3: Major pipeline terminal fire in Russia

- April 4: Oil facility fire in Russia

- April 7: Thermal power plant fire in India

- April 9: Refinery fire in Mexico

- April 15: Refinery fire in Australia

- April 20: Oil facility fire in Russia

- April 21: Oil installation fire in India

- April 21: Thermal power plant fire in Romania

- April 21: Oil platform fire in Texas

And let's not forget the Russian oil tankers set ablaze in the Mediterranean, the Black Sea, or others in the Gulf, or the 10 oil tankers burned in Myanmar.

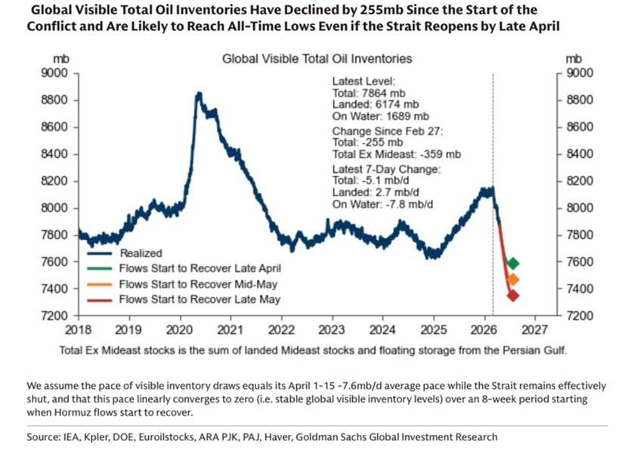

The outcome of all these events is already visible: oil and refined product inventories have dropped sharply, reaching concerning levels — and the situation could deteriorate further.

Lufthansa has canceled 20,000 flights to save jet fuel. For its part, the IEA has warned that Europe may have only six weeks of aviation fuel reserves left.

On March 11, 2026, a spokesperson for Iran’s Revolutionary Guard set the tone: “Get ready for oil at $200 a barrel!”

But ultimately, Iran has only openly expressed a dynamic that has been underway for a long time: the closure of numerous refineries, underinvestment in oil exploration, notably driven by the Financial Alliance for Net Zero. Since 2020 — or even earlier — major powers have been aware that a sharp rise in the price of oil was coming.

As early as January 2014, IMF Managing Director Christine Lagarde was already referring to the idea of a “reset” at the Davos forum. The fact that this message came from the International Monetary Fund suggests that it was a monetary event of global significance. This thinking actually dates back to discussions held after the financial crisis, particularly during the November 2008 G20 summit in Washington, sometimes referred to as “Bretton Woods 2.”

In November 2008, gold was at $700, silver at $8.75, and oil at $46.

By March 2026, gold has reached $5,400, silver $97, and oil $119.

The purchasing power of currencies has therefore significantly eroded over the years, notably due to the massive expansion of the money supply and global indebtedness. This trend of monetary devaluation could accelerate further by the end of the year.

On April 10, 2026, Donald Trump announced his intention to launch the “world's most powerful reset”.

Yet the outlines of this reset had already been sketched well in advance. As early as September 2025, the prospect of a revaluation of gold by presidential decree was being discussed, drawing in particular on certain Federal Reserve publications. My article “China and the Revaluation of Precious Metals” showed how China had anticipated this move as early as June 2025, notably by issuing instructions to its ministries in preparation for the reset. “Concerted Revaluation of Strategic Minerals” reveals that G7 countries had also, during that same period, implemented measures granting silver and other critical resources a special status.

Energy prices — and oil in particular — have already played a decisive role on the monetary front, especially after August 15, 1971, when Nixon ended the gold standard established at Bretton Woods in 1944. The first oil shock then triggered high inflation, leading to a sharp rise in gold and silver prices.

The petrodollar agreements have allowed the monetary system to function until now.

The reset announced by Trump on April 10 would therefore not come as a real surprise to government, monetary, and banking authorities.

The question — one that only a minority closely following monetary issues and precious metals seems to be asking — is now the following: at what price will these metals be revalued?

Those who closely follow international developments know that certain members of Trump’s circle have carried out leveraged stock market operations just minutes before the announcement of decisions likely to trigger significant market movements.

These practices, considered insider trading and involving individuals who are difficult to hold accountable, are said to have contributed to the resignation of the Chair of the Securities and Exchange Commission on April 16.

These repeated instances of insider trading, however, offer valuable insights for us.

On “X” (formerly Twitter), on March 9, 2026, Francis Hunt wrote:

“Someone with incredibly deep pockets is buying call options on gold expiring in December 2026, with strike prices of $15,000 and $20,000, and on a completely absurd scale. These bettors will only start making money on their calls once they exceed these levels.”

“Given the industrial scale of these purchases, it looks like someone who knows something is taking a position on what appears to be a crazy bet, wagering on the price of gold multiplying by at least four.”

“What has happened before to make this seem remarkable?”

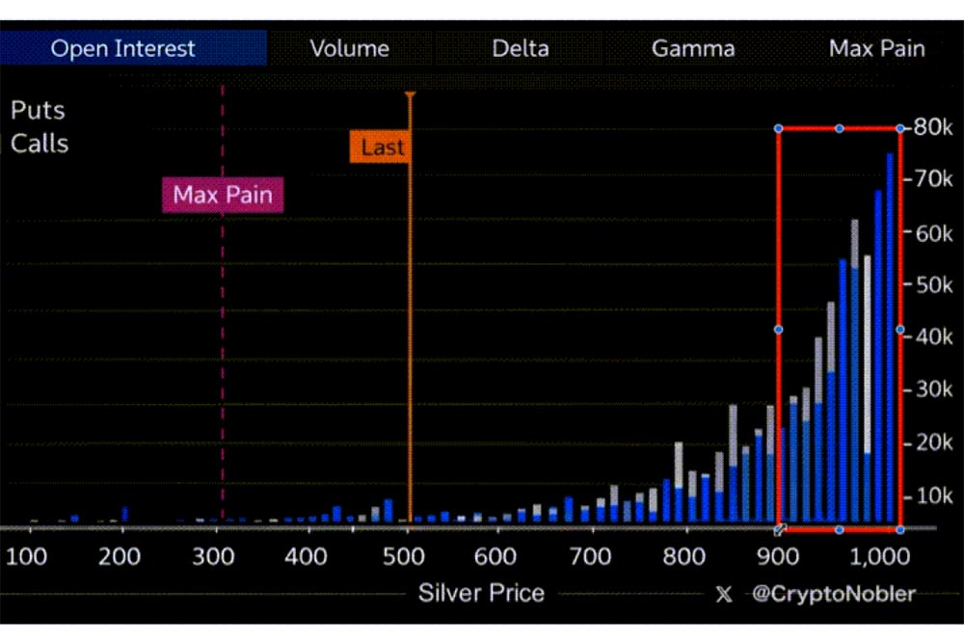

“The same thing happened in the silver market: when prices were hovering around the end of $30 and the beginning of $40, around February-March, there were massive purchases of call options targeting $80 to $85, in absolutely insane volumes.”

“And that’s exactly what happened the following December…”

Since Francis Hunt’s statement on March 9, it appears that highly aggressive traders—or insiders betting on confidential information—have taken out around 500,000 call options, wagering on a silver price between $900 and $1,000 by the end of the year.

You may consider them reckless traders and dismiss this information… that is the stance taken by Neils Christensen at Kitco.

Does $1,000 per ounce of silver seem completely absurd to you?

Not at all, in my view.

In my book “Silver Throughout History," published in 2012, I already explained — through various lines of reasoning — that this level could correspond to its value in a scenario where gold, remonetized, would be revalued to $10,000. I have always advocated a 1-to-10 ratio between gold and silver: a level consistent with both underground reserves, mining production, and the volumes of derivatives as measured by the BIS.

In this context, seeing some traders today — or insiders betting on confidential information — predicting gold to $20,000 an ounce doesn't surprise me.

A video published in August 2025 had already mentioned this scenario, detailing the accounting mechanism that could be used by the U.S. Treasury and the Federal Reserve to carry out such a revaluation. Moreover, on August 1, 2025, the Fed published a document on its website titled “Gold Reserve Revaluations: International Experience.”

And last April, Donald Trump himself claimed he was launching “the most powerful reset in the world.”

It is difficult not to connect these developments.

Such a reset would make global debt levels sustainable again, particularly that of the United States.

Time will tell!

Reproduction, in whole or in part, is authorized as long as it includes all the text hyperlinks and a link back to the original source.

The information contained in this article is for information purposes only and does not constitute investment advice or a recommendation to buy or sell.