The oil market is entering a phase where volatility is no longer a mere hiccup but a direct consequence of its structure. Recent price movements — both sharp and contradictory — do not reflect a linear improvement or deterioration in fundamentals, but rather a growing inability of prices to simultaneously reflect both physical realities and financial dynamics.

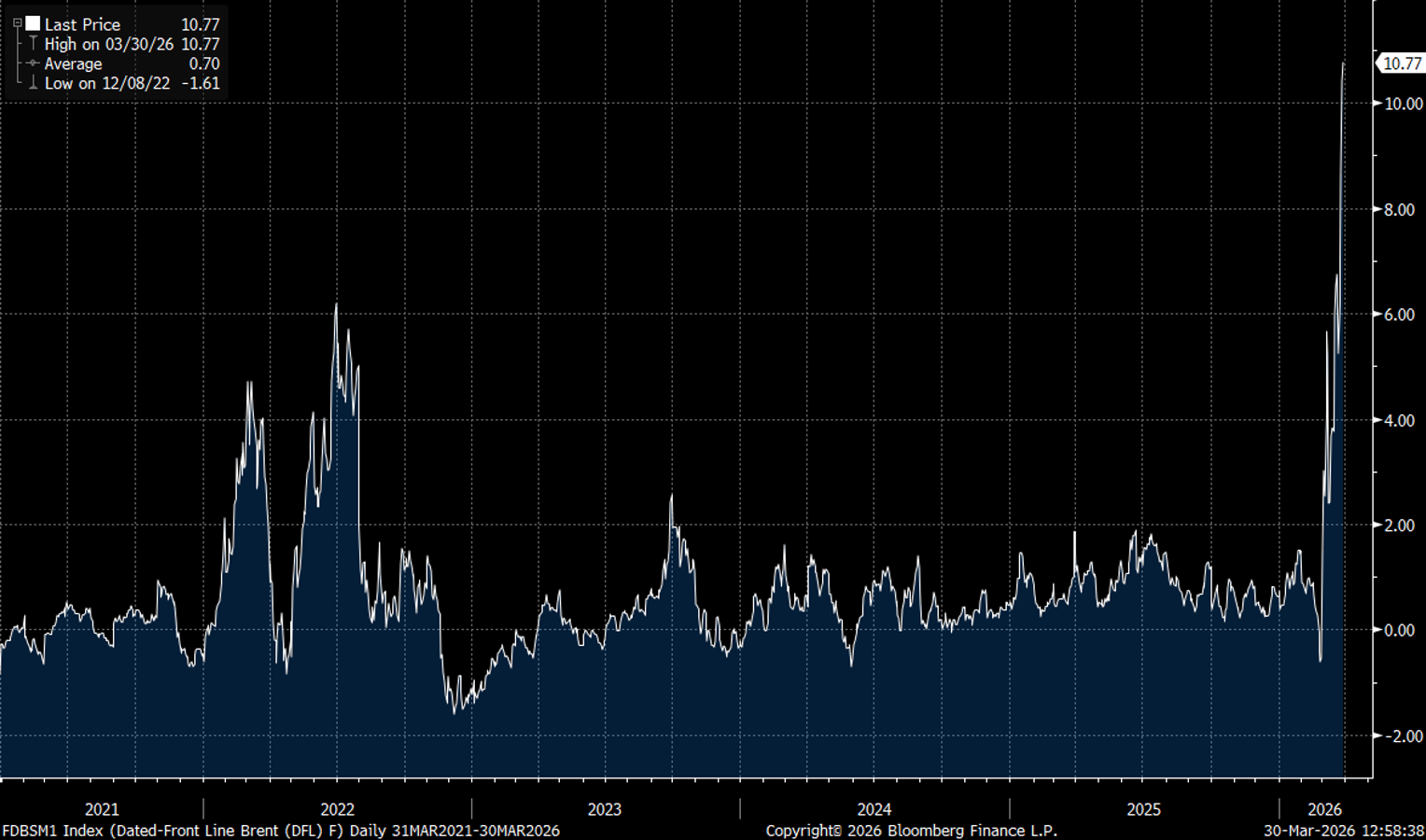

On one hand, the physical market is sending signals of tension rarely seen before. The spread between spot Brent and futures contracts — the Dated-to-Frontline spread — has skyrocketed, indicating that buyers are willing to pay a significant premium to secure oil available here and now.

This physical premium, which is approaching the extreme levels seen during previous energy crises, reflects a simple reality: oil exists on paper, but it is becoming difficult to obtain in the real world.

This tension is consistent with the documented deterioration of energy infrastructure in the Middle East. More than forty sites have been affected, including critical nodes of the system — processing facilities, export hubs, LNG terminals, and integrated power grids. These are not peripheral assets but nerve centers. Their partial or total shutdown simultaneously affects production, processing, and logistics. In other words, the shock is systemic.

And yet, at the same time, futures prices have remained contained since the start of the war, fluctuating around levels that do not reflect this physical constraint.

This discrepancy is not due to a misjudgment but to market dynamics. Today, the price of oil is increasingly determined by positioning, liquidity, and derivative flows, rather than by a direct reading of supply and demand.

Recent events illustrate this perfectly. A simple shift in the political narrative is enough to trigger movements of several dozen percent in a matter of minutes. Not because the situation on the ground has changed instantly, but because the market was already positioned in one direction. The catalyst merely reveals a latent imbalance. Stops are triggered, systematic models are reversed, liquidity vanishes — and the price plummets or soars into thin air.

This reflexive behavior is amplified by the rise of algorithms. A growing share of trading volume is now driven by models that react to volatility and momentum. Once the movement begins, these players do not stabilize it — they amplify it. The market then becomes self-referential, capable of producing extreme fluctuations without immediate fundamental justification.

Added to this is a factor that few markets have yet fully factored in, and which economist Thierry Bros explicitly points out: we are facing a supply shock of unprecedented magnitude. Approximately 20 million barrels per day typically pass through the Strait of Hormuz. Even taking into account rerouting capacity (about 6 Mb/d) and releases from strategic reserves (about 3 Mb/d), the shortfall would still be in the order of 11 million barrels per day, or nearly 11% of global consumption.

Such a shock, he emphasizes, has simply never been observed on this scale. For the market to absorb it, it would require a massive collapse in demand. Based on historical elasticities, this could necessitate prices close to $300 per barrel.

In other words, the price level needed to rebalance the market is incomparable to the level currently reflected in futures prices.

Moreover, this shock remains partially invisible, as physical shipments dispatched before the crisis continue to arrive. But this inertia is coming to an end. As he clearly summarizes: “Until now, we hadn’t yet seen the shock, but the energy crisis is beginning now.”

The market is therefore shifting from a time lag to a direct confrontation with the reality of supply. Until now, part of the shock has been absorbed by logistical inertia: shipments dispatched before the crisis continued to arrive, strategic reserves acted as a buffer, and above all, the reference price — that of futures — maintained a semblance of normality. But this phase is reaching its limit. As these “legacy” flows disappear, the market can no longer avoid coming face-to-face with a genuinely constrained supply.

At the same time, the role of derivatives markets becomes central. In theory, futures are supposed to reflect market expectations. In practice, they are now largely influenced by positioning, liquidity, and, increasingly, by short-term dynamics linked to systematic flows and arbitrage. This mechanism acts as a signal delay: as long as the paper market remains contained, it prevents the physical shock from immediately impacting visible prices.

But this implicit price control comes at a cost. By artificially suppressing apparent volatility and delaying adjustment, it fosters an accumulation of imbalances. Demand does not adjust in time, economic behavior remains based on an underestimated energy price, and market positions are built on a misperception of actual risk. In other words, the system buys time — but at the cost of a potentially much more brutal future adjustment.

When reality finally sets in, it does not do so gradually. The market does not quietly “catch up” with the physical market: it does so urgently, under pressure, often in an environment of reduced liquidity. It is precisely this type of scenario that transforms an energy shock into a financial shock. It is not so much the absolute level of prices that creates instability, but the speed at which they must adjust after having been artificially suppressed.

This view is reinforced by the analyses shared by Tsvetana Paraskova, who points out that despite short-term reactions to political statements, physical constraints are building inexorably. Every week, massive volumes — on the order of 100 million barrels — are no longer being transported. In a scenario where this situation persists, projections point toward prices of $150 to $200 per barrel, or even higher, if the disruption continues for several weeks.

In other words, the market is currently oscillating between two realities: an immediate reality, dominated by narrative and financial flows, and a deferred reality, where the physical contraction of supply inevitably prevails.

This price fragmentation has direct implications for all financial markets. Stock indices continue to rely on a “visible” oil price that remains contained, fueling the illusion of a controlled environment. But this stability rests on an increasingly distorted signal.

At the same time, the market structure is becoming increasingly fragile. The decline in gamma — the mechanism that allowed dealers to cushion price fluctuations — means that markets no longer have their primary technical stabilizer. When gamma disappears, capital flows become procyclical, amplifying price movements instead of absorbing them.

It is precisely this combination that makes the current situation explosive: a major physical shock not yet fully reflected in prices, and a financial structure incapable of absorbing its consequences.

And this is where the link to gold becomes crucial.

Initially, as is often the case during periods of stress, gold may face forced selling. Investors sell off the most liquid assets to meet margin calls or immediate cash needs. This movement may give the impression of weakness in the metal, when in reality it is a technical phenomenon.

But once this liquidation phase has passed, gold returns to what it fundamentally is in this type of environment: not merely a hedge against inflation, but a safeguard against the breakdown of the price system. When oil ceases to have a credible price, when energy signals become indecipherable and stabilization mechanisms disappear, gold becomes one of the few assets capable of absorbing this uncertainty.

In a world where oil can no longer be properly priced, gold is no longer an option — it becomes an anchor.

Reproduction, in whole or in part, is authorized as long as it includes all the text hyperlinks and a link back to the original source.

The information contained in this article is for information purposes only and does not constitute investment advice or a recommendation to buy or sell.