In 2024, the US Federal Reserve is operating in a complex economic landscape, marked by persistent inflation, stagnant economic growth and several geopolitical conflicts that are reigniting international tensions.

For the time being, the Fed is maintaining a firm stance on interest rates, but remains attentive to developments in the job market.

We saw this with the release of NFP (Non Farm Payrolls). In April, the US economy created just 175,000 jobs, the lowest figure since the 2020 recession. In addition, the unemployment rate has risen by +0.4% since April 2023, highlighting a slight deterioration in the job sector.

Why is a rate cut unlikely for the time being?

As we saw in a previous article, financial conditions continue to ease, fuelling the rally in risk assets. As evidence of this, technology stocks recorded their biggest rise since 2021.

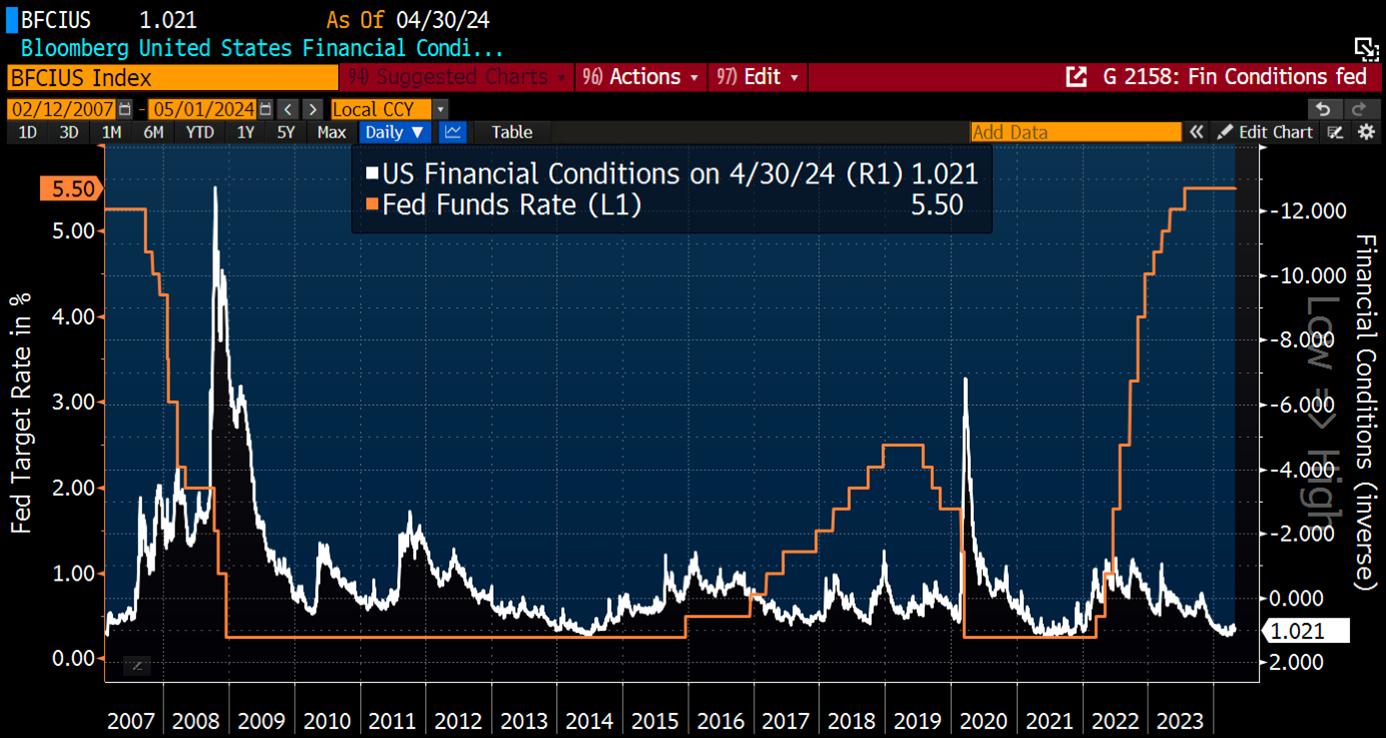

Financial conditions continue to ease, despite the Fed's declarations concerning its fight against inflation:

Financial conditions and interest rates | Bloomberg

As illustrated in the chart above, financial conditions are easing to such an extent that they are back to where they were in 2021, i.e. before the first interest rate hikes.

How can the Fed really fight inflation while allowing financial conditions to ease so much?

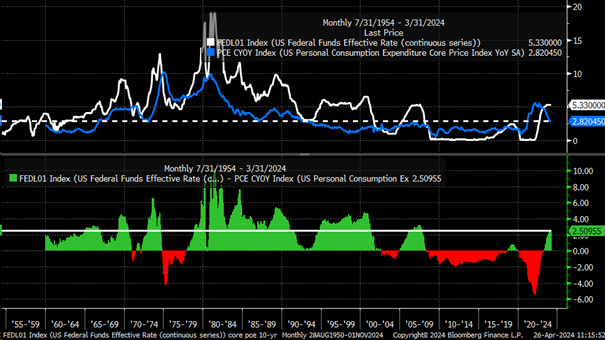

In my opinion, interest rates could remain high for some time until there are any real indicators of recession. For now, it's important to understand that the current tightening cycle is less pronounced than previous average interest rate hike cycles.

In fact, this is what can be observed by subtracting PCE inflation from federal interest rates.

It is entirely conceivable that the Fed will decide to raise interest rates if the next inflation data reveal negative signals, even in the context of a stagnant economy such as the one we are currently experiencing.

Federal interest rates + PCE | Bloomberg

Furthermore, since January we have seen the market completely change its rate cut expectations, going from four rate cuts to less than one.

Stagflation – a positive environment for gold?

Let's start with a simple definition of stagflation. Quite simply, it's an environment in which:

- Economic growth is stagnant

- Unemployment on the rise

- Inflation remains high

This stagflation is particularly problematic for the Fed, as it complicates its action. It will be difficult to raise rates too quickly, at the risk of further deteriorating the economic situation. It will be even more complicated to lower them to prevent a new inflationary surge. There is a risk of a double-wave scenario emerging, similar to that experienced in the 1970s/1980s. It is therefore important to keep this scenario in mind in the event of a Fed rate cut between now and the end of the year.

GPD and PCE estimates (Stagflation) I Bloomberg

Another indicator that can highlight a tense economic climate is the Economic Surprise Index.

Firstly, what is the Economic Surprise Index (CESIUSD)?

This index measures the difference between actual economic data and the forecasts of economists and market analysts.

When data exceeds expectations, the index rises, while it falls when data falls short of expectations.

It's important to note that most of the time, when economic news is bad, many traders anticipate economic stimulus measures from the central bank (such as quantitative easing, rate cuts, etc.), which currently explains the continuing rally in risk assets.

Oil on the fire?

New monetary policy measures are planned. According to Fed Chairman Jerome Powell, starting in June, the Federal Reserve will slow the pace at which it allows Treasury securities to expire, from $60 billion to $25 billion per month, while keeping the pace of reduction for mortgage bonds constant at $35 billion per month (tapering).

This policy will maintain an abundance of liquidity in the market, which could potentially increase inflationary pressures.

Instead of moderating inflation, the Fed seems to be stoking the inflationary "furnace" by injecting more dollars into the economy and allowing financial conditions to ease. Although inflation seems somewhat subdued at the moment, the latest PCE inflation indicators suggest persistent inflation.

It's like throwing paper on a fire: it only fans the flames of inflation. What's more, it's likely to drive down the value of the dollar and prove favorable to gold.

Conclusion

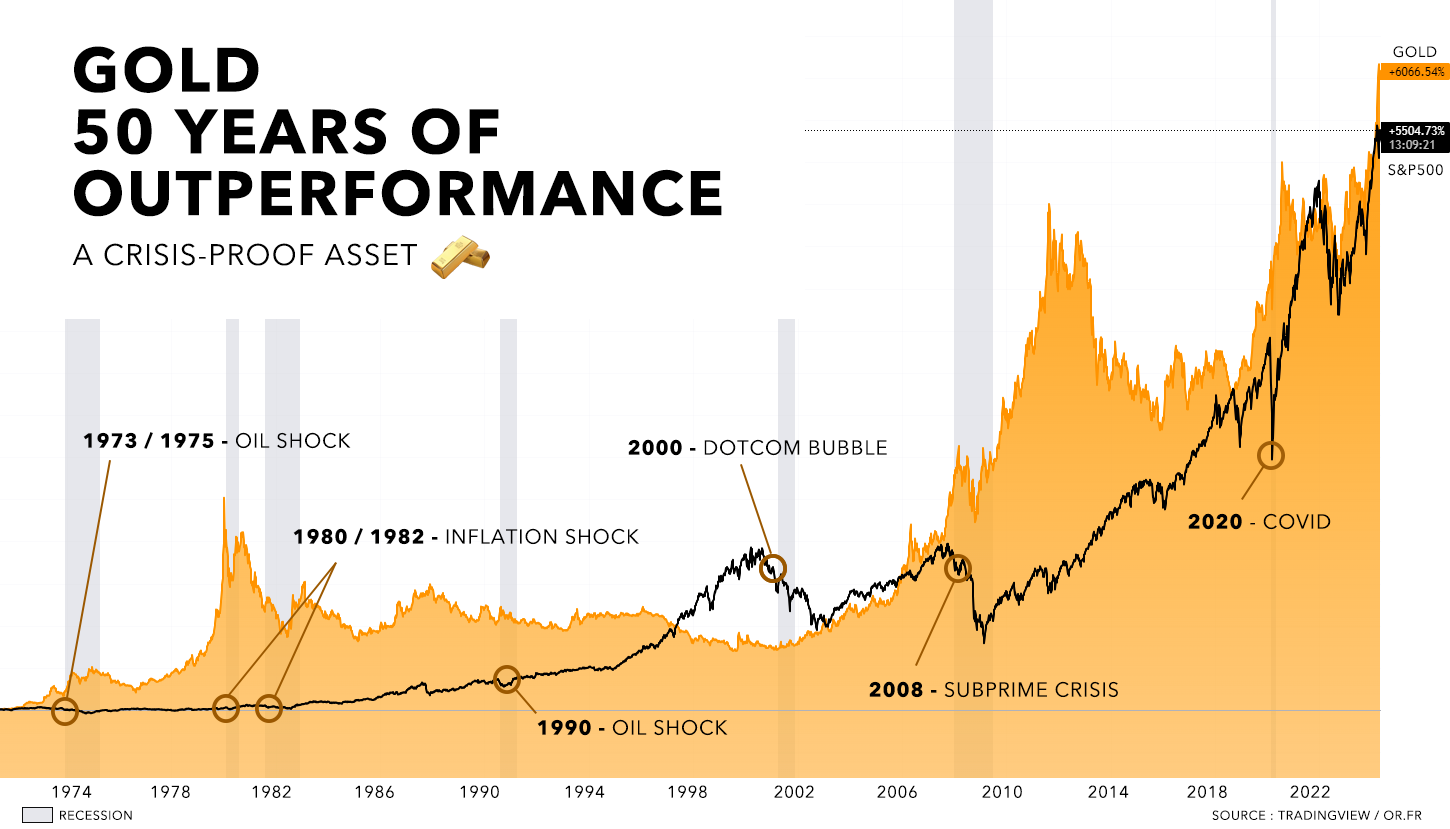

Since the beginning of the year, the performance of the gold price has been quite interesting. What's more, the asset has so far significantly outperformed the S&P500, a trend that could continue in an environment where the risk premium is still largely unfavorable to equities. Gold is perfectly fulfilling its role as a store of value. I think it's still worth taking a position in this precious metal, even if it has already moved away from $2,000. It's not certain that we'll return to this price zone. What is certain is that the dollar will continue to fall over the long term, monetary injections will continue and your purchasing power will continue to erode over time.

Over the past fifty years, gold has demonstrated its resilience in the face of some of the most severe crises to hit the financial world. The data speak for themselves: gold has clearly outperformed the S&P500 over this period.

Gold is a diversification asset par excellence, a thousand-year-old store of value whose performance is the envy of even the S&P500.

Reproduction, in whole or in part, is authorized as long as it includes all the text hyperlinks and a link back to the original source.

The information contained in this article is for information purposes only and does not constitute investment advice or a recommendation to buy or sell.