The sharp fall in the share price of Sumitomo Mitsui Financial Group, Japan's second-largest bank, following the revelation of its exposure to the British company Market Financial Solutions (MFS), may at first glance appear to be an isolated incident. On March 3, the stock lost more than 10%:

However, this is probably a broader signal about the state of global credit. MFS was a real estate lender specializing in rapid short-term financing, known as bridge financing. In concrete terms, these companies lend funds to real estate developers who need immediate liquidity to acquire an asset or launch a project, pending subsequent refinancing via a bank or the bond markets.

This model works very well when real estate prices are rising and credit remains abundant. However, when interest rates rise or liquidity becomes scarce, it becomes much more fragile. This is because it relies on short-term financing to support assets that are often riskier and relatively illiquid.

The failure of such a player does not directly threaten the global banking system. What really worries the markets is who lent it money — and in what form. In modern finance, balance sheets are deeply interconnected: a bank may finance a specialized lender, which in turn lends to real estate developers, who in turn depend on other investors.

When one of these links breaks, losses can gradually spread up the financial chain. This is precisely why the collapse of Sumitomo Mitsui Financial Group immediately led to the collapse of other major Japanese banks such as Mitsubishi UFJ Financial Group and Mizuho Financial Group. Investors do not react solely to the potential loss associated with a specific case; they seek to identify where hidden exposures lie.

Since the 2008 financial crisis, much of the world's credit has shifted away from traditional banks to what is known as shadow banking. This parallel system includes private funds, specialized lenders, securitization vehicles, and various complex financing structures. Today, it finances a significant portion of real estate, private equity, and corporate credit.

Unlike banks, these players are much less regulated and significantly less transparent. However, banks often remain indirectly exposed: either because they finance these structures or because they hold the securities they issue.

In this context, another segment of the credit market is attracting increasing attention: collateralized loan obligations (CLOs). These are financial products that pool hundreds of loans granted to already heavily indebted companies and then transform them into bonds that are resold to investors.

These structures are often highly leveraged. In some cases, the loan portfolio can be financed with leverage of close to ten times the initial capital. In other words, a relatively modest increase in defaults among the underlying companies can quickly amplify losses.

Many banks, particularly in Japan, have accumulated these products in recent years in order to generate returns in an environment of extremely low interest rates. As long as defaults remain limited and credit markets remain liquid, these portfolios appear relatively stable.

But if the economy slows or financial conditions tighten, these assets can quickly become difficult to value — and even more difficult to sell.

At the same time, another segment of the financial system is attracting increasing attention: private credit. These are loans granted directly by investment funds to companies, outside the traditional banking system. This market has expanded dramatically in recent years and now represents nearly $1.8 trillion in outstanding loans.

Former Goldman Sachs CEO Lloyd Blankfein recently warned that this sector has several worrying characteristics: often hidden leverage, assets that are difficult to value, and limited liquidity. In other words, investors may feel that they hold relatively stable investments, when in reality the underlying assets are highly sensitive to an economic downturn.

Much of this market is based on structures called Business Development Companies (BDCs). These companies lend directly to businesses often owned by private equity funds and use debt themselves to amplify their loans.

The model is relatively simple: raise capital from investors, then borrow more in order to lend even more. U.S. regulations generally allow leverage of about two dollars of debt for every dollar of capital. On paper, this level seems reasonable. But if defaults start to rise, this leverage can quickly amplify losses.

For now, the prevailing narrative is reassuring. Many players claim that private credit is contained and that the system is sound. However, some analysts who are closely examining the balance sheets of Business Development Companies (BDCs) and the composition of their loan portfolios are beginning to produce significantly less optimistic simulations.

In several scenarios, the recovery value of loans could be much lower than current models assume if the companies being financed begin to default. Another striking factor is that, despite the economic slowdown and the rise in the cost of financing, very few of these loans have yet been downgraded to speculative grade, or junk status. Rating agencies tend to be relatively lenient as long as defaults remain limited and assets are not truly tested by the market.

For some investors, the situation is reminiscent of the years leading up to the 2008 crisis. At that time, too, many claimed that the risks were “contained.” Structured products appeared robust as long as defaults remained low. It was only when losses began to appear that the true extent of leverage became apparent.

What is striking today is that despite these warning signs in the credit market, financial markets seem to be looking elsewhere. Since the outbreak of the geopolitical conflict this weekend, investors' attention has largely shifted to the possibility of a rapid resolution to the crisis.

The prevailing scenario in the markets remains that of a limited military episode, quickly absorbed by the global economy. In this context, risk appetite remains particularly high.

The flows observed in the options market clearly illustrate this optimism. More than $74 million worth of call options with maturities of 90 days or less were purchased in a single session on the SPDR S&P 500 ETF Trust, the ETF that tracks the S&P 500. This is the highest level of call buying activity since the beginning of 2026. In other words, investors are betting heavily on a rapid continuation of the stock market rally.

This phenomenon is particularly visible among retail investors, but it is not limited to them. Many institutional managers also appear to be maintaining very aggressive positions on risky assets. Market sentiment has become extremely bullish. For several months now, optimism has perhaps never seemed so widespread.

Another striking factor is the reaction of the volatility market. Since hostilities began this weekend, implied volatility has been crushed session after session. The VIX has fallen by around 20% for three consecutive days, a sign that investors are aggressively selling protection on the equity markets.

In other words, despite rising geopolitical tensions, the market is betting on a quick resolution and continues to monetize volatility by selling it off massively.

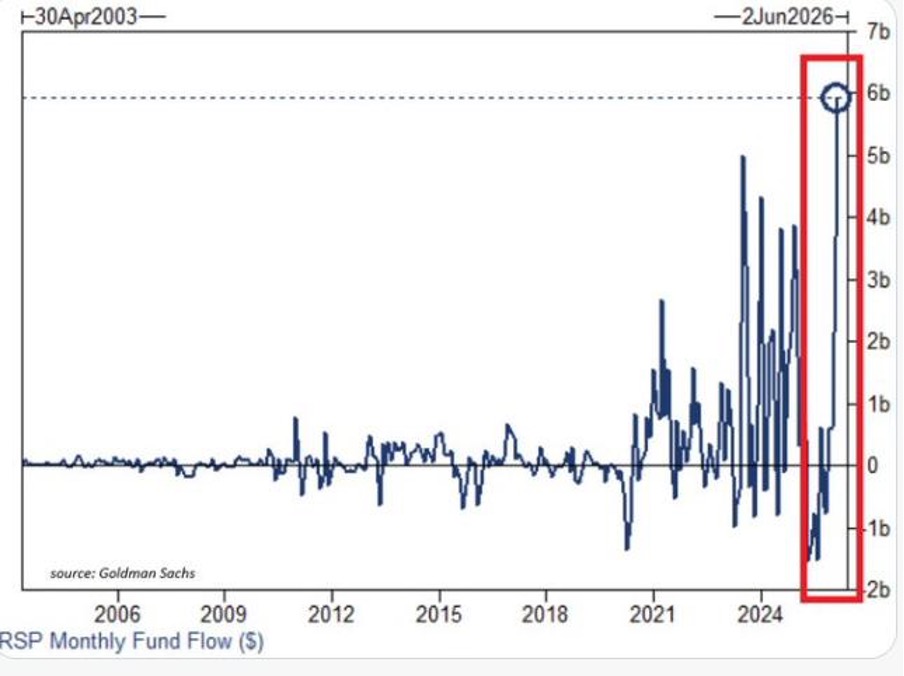

This optimism is also reflected in investment flows. The leading equal-weight ETF tracking the S&P 500, the Invesco S&P 500 Equal Weight ETF (RSP), recorded $5.9 billion in capital inflows in February 2026, the highest monthly level in its history.

The previous record, set in 2023, stood at $5 billion. In other words, investors are no longer content to buy the big tech stocks that dominate the index; they are now repositioning themselves across the entire U.S. market, including more cyclical and economically sensitive stocks. This type of flow generally reflects a phase of advanced optimism, in which investors believe that the market rally can broaden and continue.

The gap between the euphoria in the equity markets and the first cracks emerging in certain areas of credit is striking. However, financial history shows that credit tensions often precede stock market corrections. Equity markets may continue to rise for some time, supported by liquidity and investor sentiment, even as fragilities begin to form in the background.

For now, these cracks remain limited. But their appearance serves as a reminder of a simple reality: the global financial system is still based on a huge volume of credit and leverage. As long as liquidity remains abundant, these structures appear solid. However, when financial conditions tighten, points of tension quickly emerge.

History also shows that when the first cracks appear in credit, they rarely herald an isolated event. They are often a prelude to other tensions elsewhere in the system, sometimes where markets least expect them.

In this context, the evolution of the gold price deserves special attention. Contrary to what one might think, the resilience of the yellow metal does not seem to be solely linked to the geopolitical tensions that arose over the weekend. Historically, short military episodes often cause temporary reactions of the gold price, which tend to dissipate when markets anticipate a de-escalation. What is supporting the metal today is more of a structural factor: the growing perception of fragility in the credit system.

The most attentive investors know that when tensions emerge in shadow banking, private credit, or certain structured products such as CLOs, financial stability can quickly become a crucial issue for central banks again. In this type of environment, gold plays less of a role as a geopolitical hedge than as insurance against a financial accident or a sudden reversal in liquidity.

In other words, while equity markets seem to be ignoring the cracks forming in credit for now, part of the market already appears to be guarding against the opposite scenario. And it is probably this silent dynamic — rather than current military developments — that explains the yellow metal's current resilience.

Reproduction, in whole or in part, is authorized as long as it includes all the text hyperlinks and a link back to the original source.

The information contained in this article is for information purposes only and does not constitute investment advice or a recommendation to buy or sell.