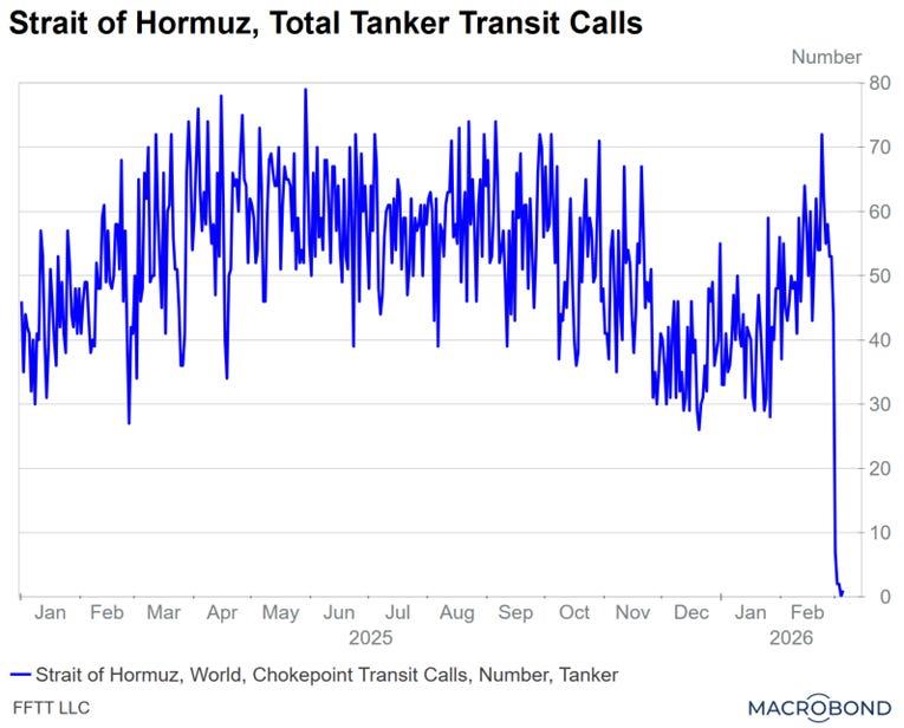

The current situation on the oil market borders on the absurd. Maritime traffic data shows a sharp decline in traffic in the Strait of Hormuz:

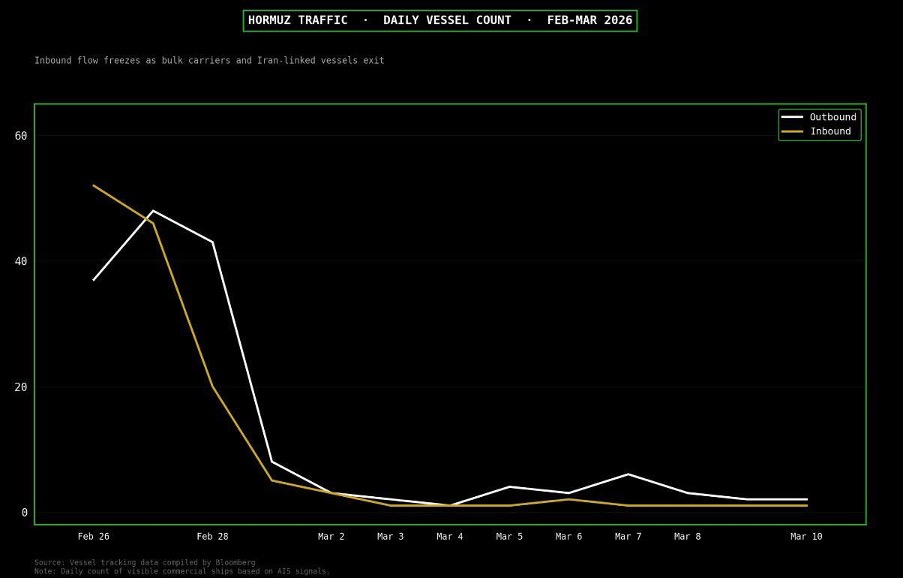

Within a few days, the number of ships entering and leaving this energy corridor had virtually come to a standstill:

Bulk carriers, huge cargo ships that transport bulk goods such as iron ore, coal, and grain, and tankers, which carry crude oil and petroleum products, are the two main types of ships that typically pass through the Strait of Hormuz. Under normal circumstances, dozens of ships, sometimes more than a hundred, pass through this particularly narrow maritime corridor every day. It is the main outlet for oil produced in the Persian Gulf to Asia, Europe, and America.

However, in recent days, maritime tracking data has shown a sharp decline in these flows. Several bulk carriers have left the area, while some ships linked to Iran are also withdrawing from normal traffic. Above all, the major shipping companies are now reluctant to send their tankers through this strategic passage. Shipowners — i.e., the companies that own the vessels — must now weigh the profitability of transport against the considerable risks involved in crossing: potential strikes, drone attacks, the presence of sea mines, soaring insurance premiums, and even the immobilization of the vessel.

In this type of situation, the strait does not even need to be officially closed for traffic to come to a halt. The mere perception of military risk is often enough to paralyze maritime traffic. Companies therefore prefer to keep their ships waiting outside the Gulf or divert their routes to other ports, rather than expose themselves to a major incident.

This is how one of the most strategic maritime passages on the planet can become virtually deserted in a matter of days.

However, the Strait of Hormuz accounts for nearly 20% of global oil flows. Estimates now circulating on trading desks suggest that around 6.7 million barrels per day of supply have been disrupted — a considerable amount. Added to this is the shutdown of the Sitra refinery in Bahrain, operated by Bapco Energies. On the Saudi side, Saudi Aramco has issued a series of cautious statements regarding the evolution of maritime security in the region and the need to closely monitor the Gulf's logistics routes. Its CEO, Amin Nasser, has warned that continued disruption in the Strait of Hormuz could have “catastrophic consequences” for global oil markets. According to him, the crisis not only threatens maritime transport and insurers, but could also cause a domino effect in many sectors of the global economy, from aviation to agriculture to the automotive industry.

Nasser also pointed out that global oil stocks are currently at their lowest level in five years, making the energy system particularly vulnerable to any sustained disruption in supply. Under these circumstances, he insisted, it is critical that maritime traffic resumes quickly in the strait in order to avoid an accelerated decline in available reserves.

In other words, one of the main energy arteries of the global system is now partially paralyzed. Historically, such a shock would have caused oil prices to skyrocket.

And yet, Brent crude has fallen by nearly 30% from its peak:

This paradox perfectly illustrates a phenomenon that we regularly discuss in these columns with regard to precious metals: derivatives markets can influence prices far beyond any immediate physical considerations.

The oil market is now largely dominated by futures contracts, options, systematic strategies, and flows from quantitative management. In an environment dominated by these instruments, the price does not necessarily reflect the instantaneous state of physical supply and demand. Above all, it reflects financial flows and the collective expectations of investors.

Trading volumes on the United States Oil Fund (USO) reached a record high of $12.4 billion on Monday. This represents an increase of more than 1,000% since the beginning of the year.

These volumes also exceed by more than 200% the peaks observed during the oil crash of 2020, during the war between Russia and Ukraine in 2022, and even during the peak volatility of 2025.

This explosion in activity is fueled by both institutional and retail investors seeking to take advantage of the high volatility in oil prices.

The spectacular fall in crude oil prices seems to correspond in part to the liquidation of highly leveraged positions. Once the initial movement has begun, these speculative positions are forced to unwind, which mechanically amplifies the decline and accelerates price movements on the futures markets.

This decline in oil prices is now fueling a very optimistic narrative in the markets. The drop in prices is interpreted as proof that the energy crisis will be short-lived. The dominant narrative is simple: the war is nearing an end, shipping routes should quickly return to normal, and global supply will once again be abundant. The easing of oil prices is acting as a powerful catalyst for risky assets. Equity indices are rebounding sharply, buoyed by the idea that the energy shock may ultimately be only temporary.

In this context, the behavior of retail investors is particularly striking:

Flow data shows that retail investors consistently buy on every correction. In 2026, average daily stock purchases- by individuals on days when the S&P 500 falls- have reached a historic high. These purchases are now twice as high as during the meme stock frenzy in 2021.

In February, purchases made on down days were 4.3 times higher than those made on up days, compared to only 2.1 times in January. At the same time, the average daily volume of options traded by retail investors in 2026 exceeds that of 2025 by 14% and the average observed between 2020 and 2025 by 47%. In other words, individual investors continue to buy every market dip.

Behind this apparent euphoria, however, certain signals from the credit market deserve special attention. Historically, credit has often proven to be more sensitive to real economic risks than equity markets. Bond investors focus primarily on one fundamental question: will the debt be repaid?

Several recent indicators suggest growing caution in the most fragile segments of the credit market. The leveraged loan market — loans granted to highly indebted companies, often as part of LBO transactions — has undergone a sharp correction in recent weeks. The ETF that tracks this segment, the Invesco Senior Loan ETF, has experienced an unusually rapid decline for an asset generally considered to be relatively stable.

At the same time, certain listed companies specializing in direct corporate financing, such as Ares Capital, have been showing a gradual downward trend for several months.

More interestingly, certain ratios comparing different layers of the credit market are deteriorating. When leveraged loans begin to underperform high-yield bonds, it often means that financing for the most indebted companies is becoming more fragile. This phenomenon directly affects private equity-backed companies and part of the private credit market.

The current situation does not yet resemble a credit crisis. High yield spreads remain contained and the financial system's “plumbing” is functioning normally. But a divergence is beginning to emerge between the very optimistic behavior of the equity markets and the growing caution observed in certain pockets of credit.

In this context, another factor is worth noting: the price of gold is ultimately reacting relatively little to the extreme volatility of oil. Despite the apparent chaos on the Gulf's energy routes, the yellow metal remains remarkably stable:

The gold market seems to be looking elsewhere. Rather than reacting to oil price fluctuations, it remains focused on a deeper dynamic within the financial system: credit.

Reproduction, in whole or in part, is authorized as long as it includes all the text hyperlinks and a link back to the original source.

The information contained in this article is for information purposes only and does not constitute investment advice or a recommendation to buy or sell.