Despite the relative resilience of the markets, it is becoming increasingly difficult to conceal the onset of a slowdown in the US real economy. Wall Street is breaking records, Main Street is taking a nosedive.

The Dow Jones US Trucking Index reflects this change in trend:

The US Railroad index also experienced a similar downward breach:

Main Street is showing signs of slowing at the beginning of May.

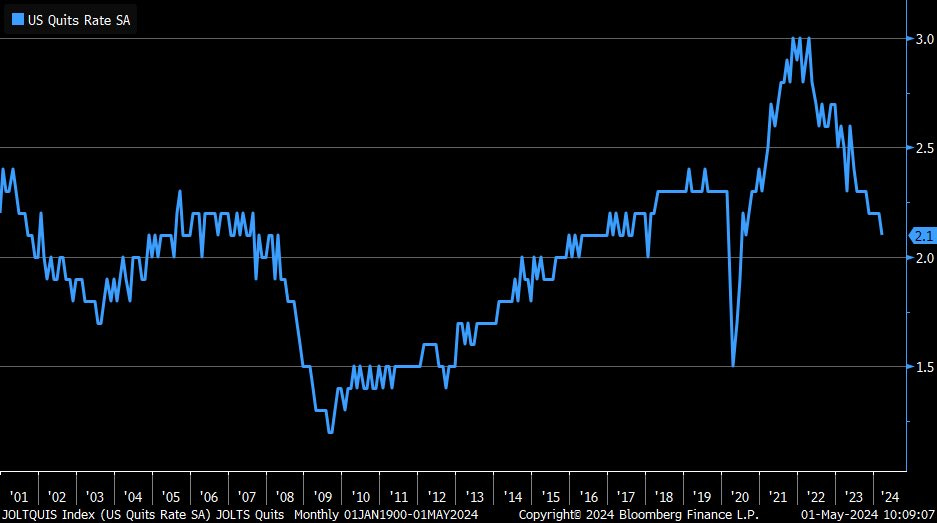

The job market is now a long way from the post-Covid euphoria. We're back where we were before the health crisis, as far as hiring and resignations are concerned:

The resignation rate is returning to the more traditional levels seen since the turn of the century:

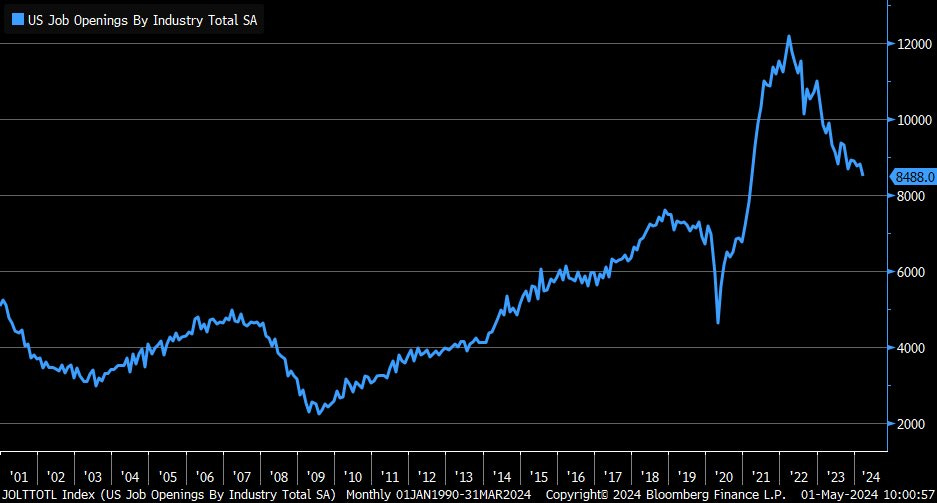

The job market is clearly cooling. March JOLTS job vacancies fell to 8.488 million, compared with 8.69 million expected and 8.813 million the previous month, the lowest level since the post-pandemic recovery:

Another unpleasant surprise: the PMI manufacturing index fell again. The US ISM manufacturing survey for April fell to 49.2, below expectations of 50.0 and the previous figure of 50.3:

The construction sector is suffering the sharpest decline, with an unprecedented collapse in job vacancies. April's figure is the lowest ever recorded for this sector:

We all know how important the construction sector is to the American economy as a whole. As the saying goes, "When construction goes, everything goes". But what happens when it collapses?

The economy slows down, but probably not enough for the Fed to act.

The Fed's decision to keep rates unchanged at 5.50% doesn't really come as a surprise, in line with very recent projections.

But these projections have been heavily modified in recent months!

It's important to remember that last January, the market was anticipating three rate cuts of 0.25% in the first six months of the year:

The expectations of the major banks were completely modified just four months after the Fed's "psychological" pivot:

The Fed plans to keep rates higher and for longer than expected, due to the persistent inflation problem in the USA.

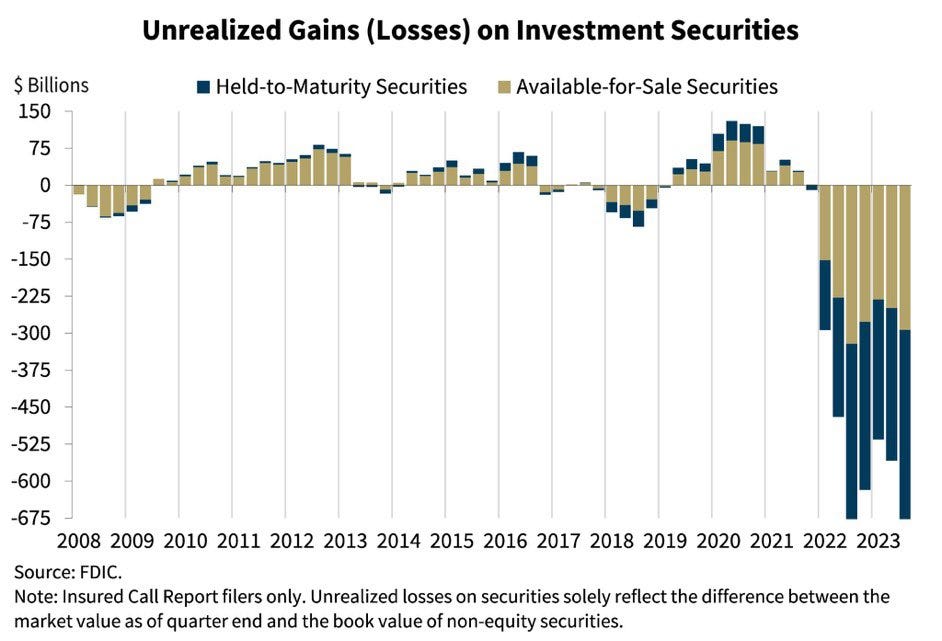

This situation is not good for banks' balance sheets, which continue to face mounting unrealized losses. As long as interest rates remain high, bond portfolios will continue to accumulate losses, weakening bank balance sheets.

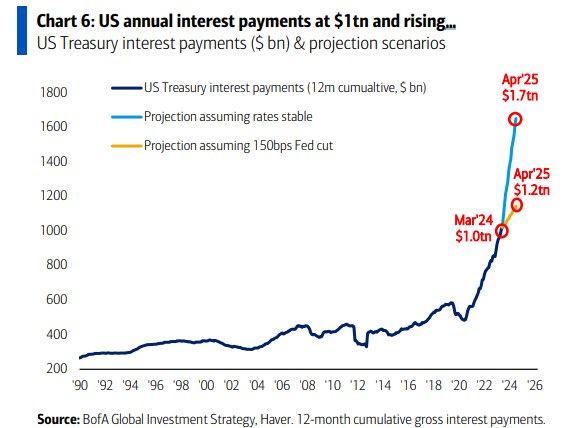

For the US Treasury, keeping rates above 5.5% represents a real challenge for refinancing US debt.

If the Fed doesn't act soon to cut rates, annual interest payments on the debt could reach $1.7 trillion. This is of course inconceivable, but this prospect alone is a guarantee that the Fed will cut rates, even if inflation starts to rise again.

With a 150 basis point rate cut, interest payments on debt would still amount to around $1.2 trillion, according to a Bank of America study:

Against this backdrop, it is clear that the Fed will not be able to stand idly by for much longer.

The fact that the price of gold remains above its break line is a signal that the Fed will not be able to keep rates at this level for very long without jeopardizing the refinancing of US debt.

Reproduction, in whole or in part, is authorized as long as it includes all the text hyperlinks and a link back to the original source.

The information contained in this article is for information purposes only and does not constitute investment advice or a recommendation to buy or sell.