Warning signs are piling up, but the markets continue to ignore what is unfolding deep within the global supply chain.

The breaking point now lies in the Middle East. The situation in the Strait of Hormuz, a vital artery for global energy trade, has deteriorated sharply. It is now part of a widespread military escalation that directly affects critical infrastructure.

The island of Kharg — the logistical hub of Iranian oil exports — has been bombed.

This is far from a minor incident. Kharg accounts for between 85% and 95% of Iranian crude exports, making it a true single point of transit for the entire national production. The island is connected by pipeline to most major onshore and offshore fields and has infrastructure capable of simultaneously loading several supertankers in deep water — an advantage the rest of Iran’s coastline lacks.

In other words, Kharg is not merely a strategic infrastructure: it is a true single point of failure in the energy system.

Significant damage to the island could remove between one and two million barrels per day from the market, representing a significant share of global supply. But beyond the volume, it is the very nature of the disruption that matters: it would be a concentrated, immediate shock, difficult to offset in the short term.

Unlike other Gulf producers, Iran has few credible alternatives for exporting its crude oil outside of Kharg Island. The other terminals remain marginal and can absorb only a fraction of the flows. A disruption, even partial, of the island would therefore automatically result in a rapid drop in exports.

This risk is all the more critical given that Kharg has historically been identified as the Achilles’ heel of Iran’s energy system. As early as the 1980s, during the Iran-Iraq War, the island was targeted on several occasions for this very reason: striking Kharg amounts to directly targeting the regime’s financing capacity.

But it is primarily in terms of Iran’s response that the risk becomes systemic. Tehran has made it clear that any sustained attack on Kharg would trigger a broader retaliation, potentially extending far beyond its own territory. The threats explicitly target the Gulf’s energy infrastructure — oil fields, terminals, refineries — as well as maritime traffic itself.

In other words, striking Kharg is not limited to reducing Iranian supply: it greatly increases the likelihood of widespread disruption to regional supply.

We would then move from a targeted shock to a systemic shock.

This is precisely what analysts fear: an escalation scenario in which the loss of Iranian production would be amplified by secondary disruptions across the entire Gulf, in a context where the Strait of Hormuz is already under strain.

Finally, a point that is often underestimated: even in the event of limited strikes, restoring Kharg’s infrastructure could take time. The island is home to heavy-duty facilities — terminals, pipelines, storage facilities — whose repair is a slow process and depends on security conditions that, in a context of escalation, cannot be guaranteed.

In other words, Kharg introduces a major asymmetry:

- easy to disrupt

- difficult to replace

- time-consuming to repair

- and highly escalatory

In a market already divided between physical and financial sectors, this represents a potentially decisive destabilizing factor. The port of Fujairah, the UAE’s only outlet from the Persian Gulf, has now come to a standstill following several drone attacks. The Shah gas field in the United Arab Emirates was also hit, marking a turning point: it is no longer just the flow of goods that is being targeted, but production capacity itself. In Iraq, the Majnoon oil field was targeted, while the Bushehr power plant was also bombed.

The pressure is now spreading to logistics hubs as well. A new barrage of Iranian missiles targeted Dubai on the night of March 17–18. Earlier in the week, a drone attack on the international airport’s jet fuel reserves had already sparked a fire. Each time, traffic is temporarily halted, then resumes. But the real question now is whether the system can function sustainably under constant stress.

Meanwhile, the United States is hardening its stance. Donald Trump is threatening to destroy all Iranian oil facilities in the event of prolonged disruption to shipping. Tehran is responding by promising to strike energy infrastructure in the Gulf in the event of further attacks. The logic of escalation is now fully in place.

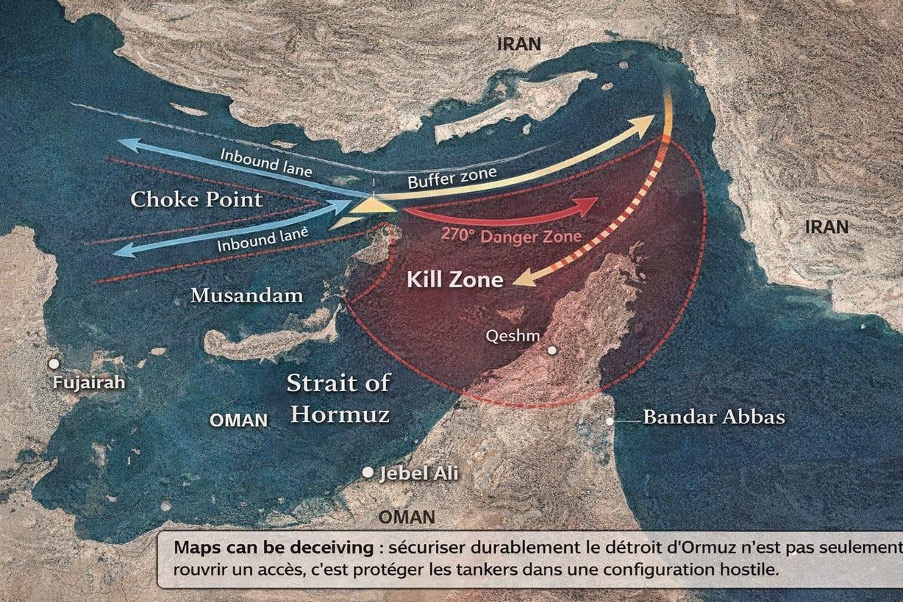

One crucial point, however, remains largely underestimated: even if the West holds military superiority, securing the Strait of Hormuz in the short term poses an extremely complex operational challenge. The strait functions as a congested maritime highway, where supertankers, regional traffic, and a multitude of hard-to-identify local vessels all coexist. In this environment, distinguishing normal commercial activity from a threat becomes particularly difficult.

Geography further exacerbates this vulnerability. The passage around the Musandam Peninsula exposes ships to fire from nearly 270 degrees, originating from Qeshm, the coastal terrain, and positions further inland. Iranian systems now combine missiles, drones, and asymmetric capabilities, making any escort mission risky.

*Ensuring the long-term security of the Strait of Hormuz is not just about reopening access; it is about protecting tankers in a hostile environment

Escorting tankers does not solve the problem: the convoys move slowly, in a tight formation, which makes them predictable and therefore vulnerable. The military vessels themselves become targets in a congested environment where their maneuverability is limited.

Above all, Iran does not need to completely close the strait. It need only turn certain sections — particularly around Musandam — into high-risk zones and control traffic flows by diverting them away from the main corridors. In other words, it can exert control over this strategic chokepoint without resorting to a complete blockade, thereby introducing structural uncertainty that is far more difficult to contain or neutralize.

And yet, despite this rapid deterioration, the markets continue to look the other way.

The impact is already visible in the real world. The shutdown of the Shah gas field, combined with disruptions in Qatar, is beginning to remove a significant portion of industrial derivative production from the market. Air transport is affected, as evidenced by the suspension of Cathay Pacific flights to the region. In India, steel mills are closing and sugar refineries are suspending operations. In Australia, some mining companies are scaling back or halting operations due to a lack of diesel.

In other words, the tightening of the energy supply chain is already underway.

However, this is not yet reflected in prices.

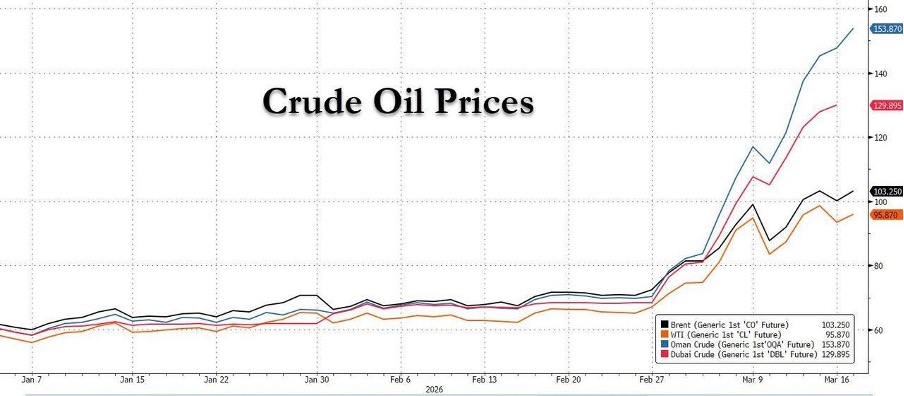

This disconnect is now clearly evident in the oil market itself. We are seeing a growing divergence between the prices of financial products — such as the Brent and WTI futures — and the actual price paid per barrel of physical oil in Asia.

While futures markets remain partly constrained by volatility and positioning dynamics, the physical market is beginning to reflect the actual tightening of supply.

This type of divergence is rarely sustainable over time. It tends to resolve itself in several ways — all of which are potentially uncomfortable:

- either financial markets abruptly catch up with the physical market, with a rapid rise in future prices;

- or demand is destroyed through a forced economic slowdown;

- or a reorganization of flows takes place, with a lasting fragmentation of the global energy market.

In any case, this reflects a profound misalignment between perception and reality.

Another signal, far more revealing than the price of Brent itself, is emerging in distillates — that is, refined products such as diesel, kerosene, or marine fuel.

The levels reached are exceptional.

Kerosene is now trading at around $200 a barrel in several hubs, with diesel following the same trend, particularly in Singapore, while marine fuel has surpassed $160 in Fujairah. These price movements are much more volatile than those seen in crude oil.

This discrepancy is key. It indicates that the problem lies not only in the supply of crude oil, but also in its processing and distribution.

In other words, the system is beginning to break down where it is most vulnerable: refining capacity and supply chains.

Under normal conditions, a rise in crude oil prices gradually feeds through to refined products. Here, the opposite is true: distillates are surging much more rapidly, a sign that certain parts of the system can no longer absorb the shocks.

Several factors are at play.

First, disruptions in the Gulf directly affect physical flows to major Asian refining hubs. Second, certain facilities are themselves exposed — directly or indirectly — to geopolitical tensions. Finally, logistical constraints (maritime transport, insurance, rerouting of flows) lengthen lead times and increase costs.

The result is a classic phenomenon, though rarely so visible: prices must “do the work” in place of volumes.

In other words, due to the inability to rapidly increase available supply, the prices of finished products adjust sharply to ration demand.

The implications are immediate.

Jet fuel priced at $200 calls into question the very viability of the airline industry. Airlines can temporarily absorb the shock, but beyond a certain threshold, adjustments become inevitable: capacity cuts, route cancellations, and higher ticket prices.

The same logic applies to diesel, which powers the real economy: trucking, agriculture, and industry. Its price increase quickly ripples through the entire production chain.

Finally, marine fuel — at the heart of global trade — is seeing costs skyrocket, which automatically makes freight transport more expensive.

This point is fundamental: the cost of movement is rising everywhere.

And it is precisely this type of shock — diffuse, logistical, difficult to model — that financial markets tend to underestimate.

This is no longer simply a rise in the price of oil. We are facing a gradual breakdown of the energy transformation and distribution system.

This also explains the fragmentation observed in the oil market. Crude oil may still give the illusion of some control, but refined products tell a different story: that of a system under strain, where certain key capacities are becoming bottlenecks.

And as is often the case in this type of scenario, it is not the point of origin of the shock that matters most, but where it spreads and where it eventually comes to a standstill.

Today, that point of blockage is at the refining stage.

There is also a significant divergence in the perception of risk. In Europe, this impending inflationary shock remains largely underestimated. The consensus continues to be that of a managed slowdown, and the prevailing mindset remains “buy the dip,” based on the expectation of a swift resolution to the conflict and a return to normalcy.

In Asia and Australia, the view is different. Authorities are beginning to factor in a scenario of higher and more persistent inflation. The Australian Treasurer explicitly mentions inflation potentially reaching the 4% range, or even higher, depending on the scenarios considered. Where Europe is hoping, Asia is beginning to anticipate.

Another factor reinforces this view of a deeply desynchronized market: the recent drop in crude oil prices does not reflect an improvement in fundamentals, but primarily technical flows.

The U.S. Department of Energy has in fact launched an operation involving the Strategic Petroleum Reserve (SPR) covering approximately 86 million barrels. But contrary to what one might think, this is not a simple sale: it is an exchange mechanism. Participants who receive oil today will have to return more in the future, with a premium of up to 20%.

In practical terms, this amounts to a high-interest oil loan. Participants are incentivized to sell the barrels they receive immediately — which puts downward pressure on prices in the short term — by betting on the possibility of repurchasing them later at a lower price.

This mechanism creates an artificial distortion: the short-term price of crude is pulled down, not because supply is abundant, but because concentrated technical flows are exerting pressure at the front end of the curve.

And this is precisely what makes the current divergence even more striking.

While crude oil appears to be under control, refined products — diesel, kerosene, and marine fuel — are skyrocketing. This decoupling indicates that the problem lies not in oil production, but in its processing and distribution.

In other words, crude oil tells a “technical” story, while distillates reflect the physical reality of the energy system.

In this context, the drop in crude oil prices may prove misleading. It does not reflect an easing of tensions, but rather a temporary effect linked to market mechanisms. Meanwhile, the real constraints — refining capacity, logistics, and securing supply flows — continue to deteriorate.

The behavior of European fund managers is, in this regard, particularly revealing. The prevailing scenario is based on the assumption of rapid U.S. intervention to reopen the Strait of Hormuz, followed by an almost immediate normalization of flows. But this view ignores industrial timelines. Even if hostilities were to cease in the very short term, the damaged infrastructure — Kharg, Fujairah, Shah, Majnoon — requires inspections, repairs, and logistical security. Physical flows do not resume instantly. There is an unavoidable lag time, which is completely absent from current pricing.

At the same time, the market remains dominated by technical dynamics linked to option expirations — in particular VIXpiration (expiration of volatility contracts) and OPEX (monthly option expiration).

In practical terms, a large portion of current flows does not come from investors taking fundamental medium-term positions, but from market participants active on extremely short time horizons — sometimes just a few hours — via so-called “0DTE” options (expiring on the same day).

In this context, dealers play a central role. When an investor buys an option — for example, a call option to anticipate a rebound or to hedge against a decline — an intermediary must take the opposite position by selling it: these are typically the dealers.

They immediately collect a premium, with a simple goal: for the option to expire worthless. However, when volatility remains low — typically with a CBOE Volatility Index around 20–22 — a large portion of these options do indeed end up expiring without being exercised. Investors then lose the entire premium paid, while dealers keep it.

This mechanism has several significant consequences.

To prevent the options from becoming “in the money” — and thus costly for them — they constantly adjust their positions: they buy when the market falls and sell when it rises. This creates a cushioning effect that limits overly sharp short-term movements.

Next, this mechanism gives rise to a well-known phenomenon: investors who buy protective positions (puts) or bullish bets (calls) with very short maturities see their positions deteriorate rapidly if the market does not move quickly enough. As the expiration date approaches, the time value of these options erodes — a process known as “premium erosion.”

Finally, short positions are often forced to cover at unfavorable terms as expiration approaches, fueling technical rebounds even in the absence of positive news. Conversely, buyers of protection may be forced to unwind their positions before expiration, further reinforcing this dynamic.

Ultimately, the market operates in what is known as a “short volatility” regime, where volatility compression becomes dominant.

In this regime, bad news tends to be absorbed — not because it is insignificant, but because technical flows related to options temporarily take precedence over fundamentals.

Dealers capture the premium, the market remains artificially stable, and investors seeking to hedge or anticipate a rapid move see their positions erode.

This mechanism does not eliminate risk; it merely delays it.

But beyond this dynamic, the main blind spot remains the Fed.

Markets continue to believe that monetary policy will be able to contain the coming shock. Attention remains focused on the Federal Reserve’s upcoming decisions, as if it still held decisive leverage over the situation.

The Fed has chosen to keep rates unchanged, but the dilemma is clear. Lowering rates would fuel an inflationary shock already taking shape. Raising them would heighten the risk of recession. It is now constrained, with no real room to maneuver.

This situation is reminiscent of February 2020. At the time, the first supply chain disruptions in China were already visible but largely ignored. The market remained focused on the Federal Reserve’s ability to cushion the shock. The correction only occurred once the true nature of the shock — not monetary, but logistical — became apparent.

We are now in a comparable situation, with one major difference: the current shock is directly inflationary.

We are thus facing a triple denial — geopolitical, monetary, and market-driven. While investors scrutinize the Fed and short-term technical dynamics, tensions continue to build in the real economy.

It is precisely in this type of environment that the price of gold forms its trends. While equity markets remain artificially propped up by suppressed volatility, gold is consolidating. This phase does not reflect weakness, but rather a period of accumulation.

Every day of denial, every instance of suppressed volatility, and every misreading of actual risk fuels the next upward phase.

Once the market finally comes to terms with the nature of the shock — real, energy-related, and inflationary — the adjustment will not be gradual.

It will be rapid.

Reproduction, in whole or in part, is authorized as long as it includes all the text hyperlinks and a link back to the original source.

The information contained in this article is for information purposes only and does not constitute investment advice or a recommendation to buy or sell.