The U.S. federal debt has now surpassed the symbolic threshold of 100% of GDP, the CRFB (Committee for a Responsible Federal Budget) has just announced. More specifically, this refers to federal debt held by the public ($31.27 trillion), thus excluding debt held by the Fed, the U.S. central bank. Including the latter, total debt reaches $39 trillion, or 122% of GDP.

BREAKING 🚨: U.S. Debt

— Barchart (@Barchart) April 30, 2026

U.S. Debt now exceeds 100% of GDP for the first time since World War 2 🤯👀 pic.twitter.com/FD3KF8IRgQ

One point, however: in Europe, this distinction is not generally made. The Banque de France holds approximately 22% of the government’s debt, but this portion is not subtracted from the total debt. If it were, France’s debt would fall back below 100% of GDP, to around 95%. Some economists even believe that this 22% could be wiped out with the stroke of a pen, without major consequences, since it is debt that the government owes to itself — but that is another debate.

The CRFB emphasizes the “bipartisan” (Republicans and Democrats) nature of this drift: unfunded tax cuts, new spending, emergency aid, and the absence of binding rules to rein in deficits. As Atlantic Council explains, three items are driving spending up in particular: pensions, healthcare programs, and interest payments.

The first two rise automatically as the population ages; the third skyrockets as soon as interest rates rise, with debt service now accounting for 14% of the budget. Revenue, meanwhile, remains broadly stable as a share of GDP. The result: even in the absence of a major shock, the United States has settled into a regime of permanent deficit.

Real growth of around 2% is no longer sufficient to offset primary deficits (i.e., excluding debt service) exceeding 3% of GDP.

This continued rise in debt has not, so far, triggered panic in the markets. It must be said that the markets don’t really have a choice: the dollar remains the world’s primary reserve currency, the dominant currency for international transactions (oil, commodities, etc.), as well as the foundation of the world’s largest and most liquid financial market, with no real competitor to date.

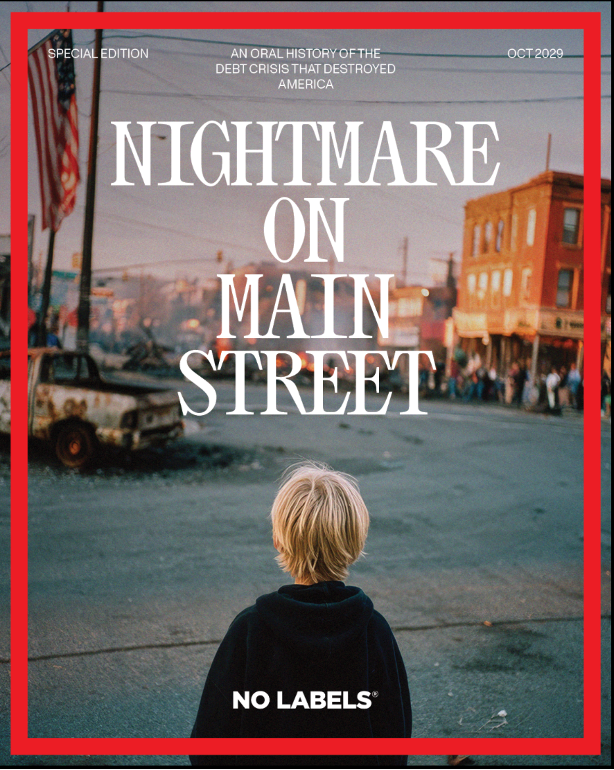

However, investor confidence could eventually erode — this is the scenario envisioned by the organization No Labels (Fortune). A century later, is the United States on the verge of a financial crisis comparable to the Great Depression of 1929? In a 75-page document titled “Nightmare on Main Street”, No Labels envisions an America on the brink of economic collapse, having failed to manage its public finances.

The turmoil is projected to begin in September 2028, two months before the presidential election that is supposed to determine Donald Trump’s successor.

The crisis begins with difficulties in selling U.S. debt: investors demand ever-higher interest rates, rising from 5% to 6%, then 7%, 8%…

Treasury bond holders panic: “Who would want to buy our 10-year bonds offering a 5% yield when it’s possible to buy new ones at 8%? No one, unless we sell them at a steep discount. That’s what we had to do,” says the fictional CEO of an American bank.

The value of bonds then collapses, dragging banks down with it, as bonds constitute one of their main balance sheet assets. Credit tightens sharply, hitting the real economy hard with corporate bankruptcies and massive layoffs. The Fed attempts to limit the damage by cutting interest rates, but at the cost of a resurgence of inflation and a further erosion of purchasing power.

This is, of course, merely a scenario, but the deterioration of public finances and the explosion of the debt burden do not appear sustainable in the long term. Moreover, the United States is not an isolated case: France is following a similar trajectory. But as the world’s leading economic power, a U.S. default would have catastrophic consequences.

As is often the case in economics and the markets, psychology plays a central role. And throughout 2029, the United States will be marking the 100th anniversary of the 1929 crisis — enough to fuel anxiety and invite bad luck.

Reproduction, in whole or in part, is authorized as long as it includes all the text hyperlinks and a link back to the original source.

The information contained in this article is for information purposes only and does not constitute investment advice or a recommendation to buy or sell.