Building a portfolio is the foundation for any investor, which raises the first questions to ask: what criteria to use, what rules to establish, and so on. I touched on this topic in January 2025 in Gold Is Making a Strong Comeback in Investment Portfolios. I’m revisiting it here through the analysis of Jeff Park, a former institutional trader at Morgan Stanley, now an advisor at Bitwise and the creator of Radical Portfolio Theory™, whom I discovered in this video.

As he explains in his article, the traditional 60/40 portfolio — composed of 60% bonds for safety and 40% stocks for growth — has lost its relevance. The reason: the strengthening correlation between these two asset classes. Previously, they moved in opposite directions: during periods of growth, stocks drove the portfolio, while during recessions, bonds provided a reliable return. The 60/40 portfolio was then an optimal solution, combining return and safety.

But that seems to be a thing of the past. Since 2021, the correlation has turned positive: stocks and bonds move in the same direction, generating too much volatility and risk.

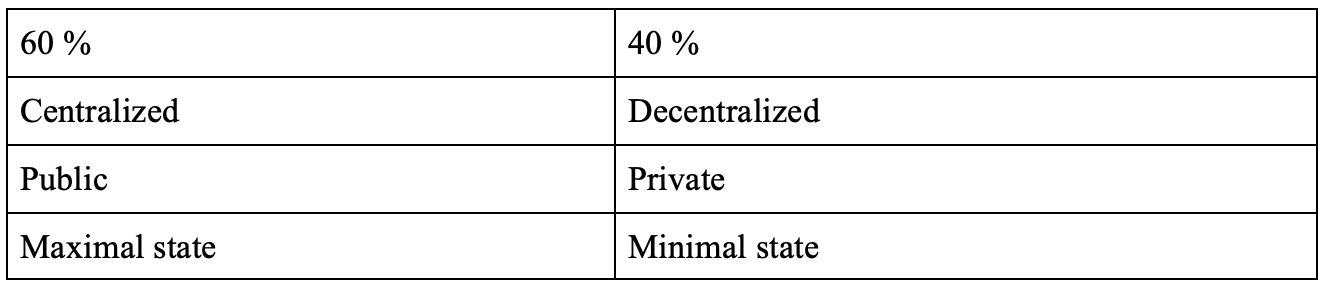

What should be done? Jeff Park proposes the “radical portfolio,” structured around an “inside/outside the system” framework, where the “system” refers to the state. The 60/40 split is retained, but this time it is defined according to the following criteria:

The 60/40 distinction is now drawn between assets that depend on the government and those that do not. On one side are sovereign bonds, banking products, and shares of companies dependent on the government (through government contracts or regulations), which offer average but relatively stable returns. On the other, there is physical gold, self-held bitcoin, works of art, certain tech stocks, professional gaming and betting sites (such as Polymarket, where one can trade directly), and financial market bets, which offer potentially high returns but with increased volatility.

Above all, this second category offers a form of protection in the event of government failure — a risk that has been largely ignored until now. The distinguishing factor is therefore the government itself, perceived as a growing threat — whether due to the accumulation of regulations, rising taxes, the development of “crony capitalism” (favoring certain large corporations close to the government), or, in the face of mounting debt, the risk of bankruptcy or the imposition of Greek-style austerity, which could be devastating to the economic fabric.

Be careful, however, not to make a mistake: with physical gold, we are in the resilient 40% category, whereas with paper gold, we enter the state sphere and lose the initial advantages.

Digital technologies must be distinguished from the rest of the economy, as Jeff Park explains. We also find this idea in an excellent comment from the AI-focused X account @brivael: “There is no innovation anywhere anymore, except in tech. Why? Because tech is still an infinite-sum game. Value is created from nothing there; prosperity is generated there. Everywhere else — education, healthcare, real estate, energy, transportation — we’ve overregulated, bureaucratized, and protected to the point of killing the infinite-sum games. All that’s left are zero-sum games. And a zero-sum game, by definition, is pure competition for a slice of a pie that’s no longer growing."

Tech is, by nature, ahead of regulation, which is both its strength and its advantage over other sectors of the economy.

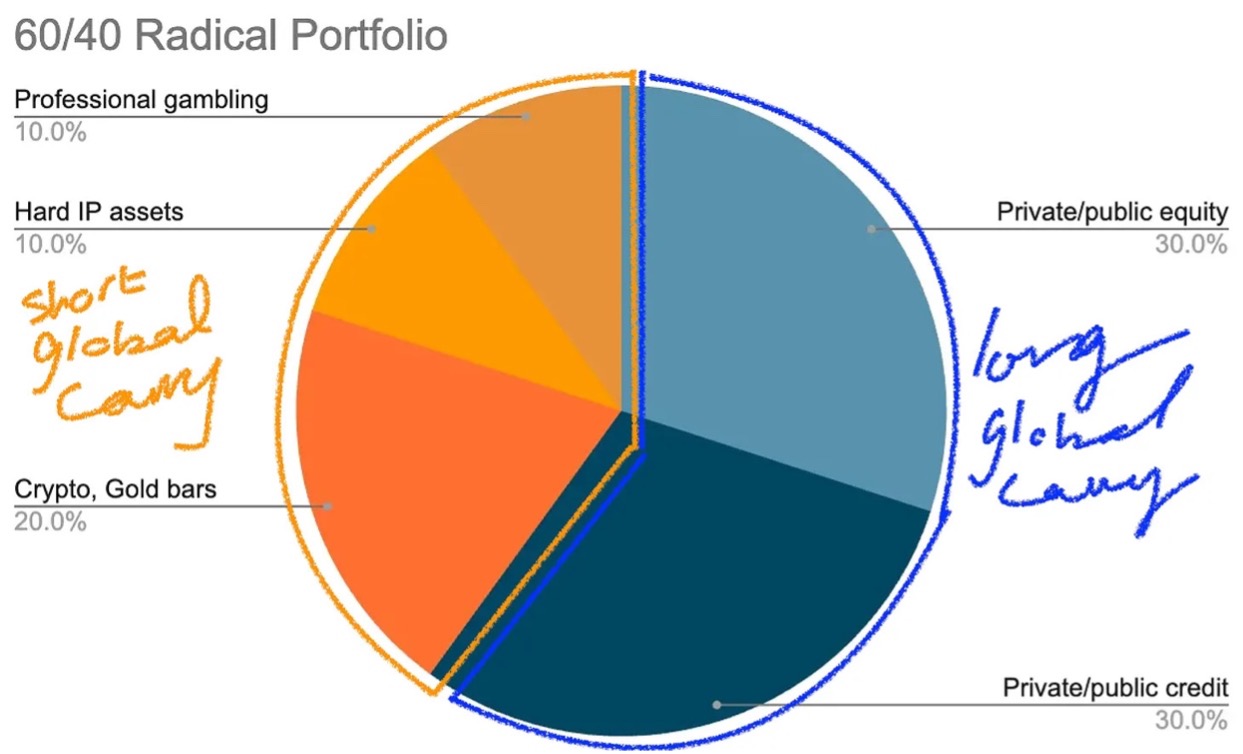

Here is Jeff Park’s Radical Portfolio:

Equities shift into the 60% allocation, alongside sovereign bonds (thus bringing the 60/40 portfolio down to a “60”). Hard IP assets can be translated as “hard intellectual property assets,” meaning technology companies in a near-monopoly position (such as Google) or technology patents.

On the one hand, there are stable but fragile assets (particularly in the event of government default); on the other, there are more volatile but “antifragile” assets, to use Nicholas Taleb’s term — antifragility referring to something that grows stronger over time and through shocks, going beyond mere resilience. This analysis is particularly relevant: the antifragile segment is capable of withstanding almost anything, including government default (or severe austerity). Yet this risk looms ever larger as public debt climbs, in both the United States and Europe.

In Europe, however — and in France in particular — this graph must be adapted. Professional gambling companies are banned there (La Française des Jeux holds a monopoly, Polymarket is banned), and digital technologies remain in their infancy compared to Silicon Valley. In the European Union, AI has been heavily regulated even before it truly emerged, which is hindering its development.

As a result, there is little left to include in the antifragile portion: physical gold, bitcoins, possibly bets on financial markets, and that’s it.

In short, the state poses a threat that must be factored into portfolio construction.

Reproduction, in whole or in part, is authorized as long as it includes all the text hyperlinks and a link back to the original source.

The information contained in this article is for information purposes only and does not constitute investment advice or a recommendation to buy or sell.