The U.S. economy continues to send mixed signals. The Citigroup Economic Surprise Index (CESI) rebounds this week:

At the same time, orders for durable goods are falling sharply:

The consumer continues to be resilient, but these latest numbers show that businesses are preparing to lower their growth expectations.

But there is no indication of a sharp slowdown in demand. This allows the Fed to continue to hope for a soft landing for the economy. By encouraging risk-taking, this rhetoric runs counter to anti-inflation policy and fails to take into account the lagged effects of a change in monetary policy. Many observers now expect the economy to be affected by the rate hikes with a delay of several months: the effects of the rate hike have not yet materialized in the real economy. After having been slow to control inflation and then having missed its forecasts on the transitory nature of inflation, the Fed is likely to make a mistake by being too moderate on the risks of a slowdown. This new policy mistake would increase the probability of a recession.

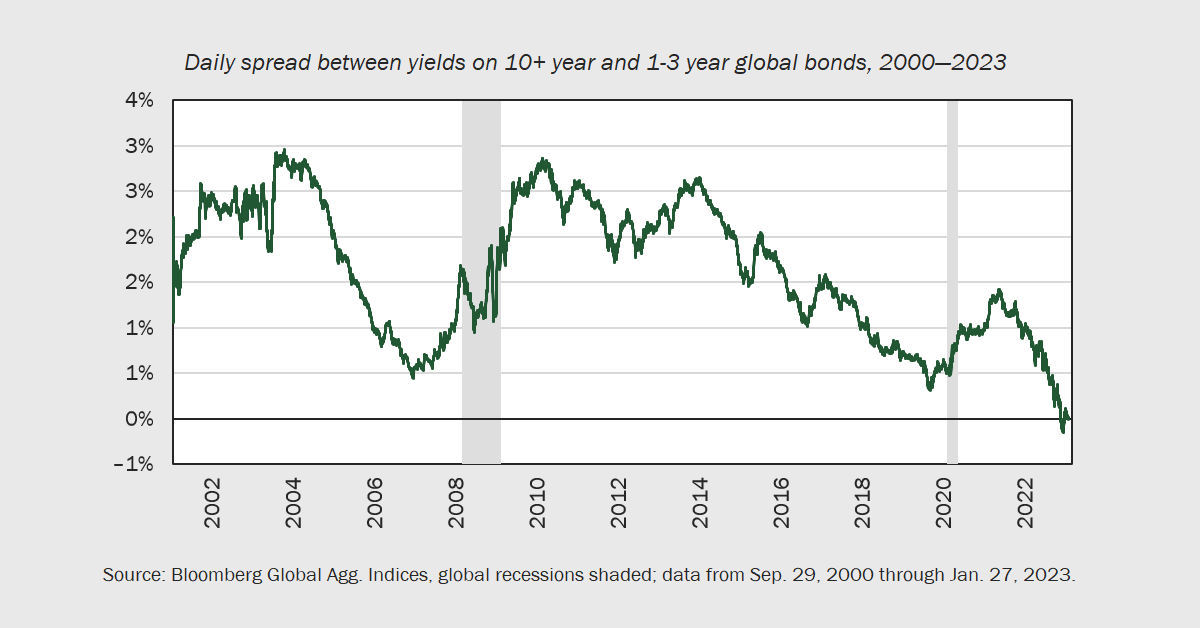

The inversion of rates (between the 10-year and the 2-year in particular) indicates the arrival of a recession in the United States by the end of the year:

In 2007, the inversion of the yield curve signaled the start of a recession.

Is this indicator still as accurate today? The curve is less readable because of Fed and Treasury purchases. How can we give credence to these indicators when central banks (and even the Treasury) are becoming major players in these markets, which are no longer free to determine the true value of the rate spread?

A bad recession forecast can have damaging consequences on an investment strategy! For the time being, although the U.S. economic numbers are not impressive, they do show some resilience, especially on the consumer side.

Unfortunately, the situation in Europe is quite different.

German GDP declined in the last quarter of 2022:

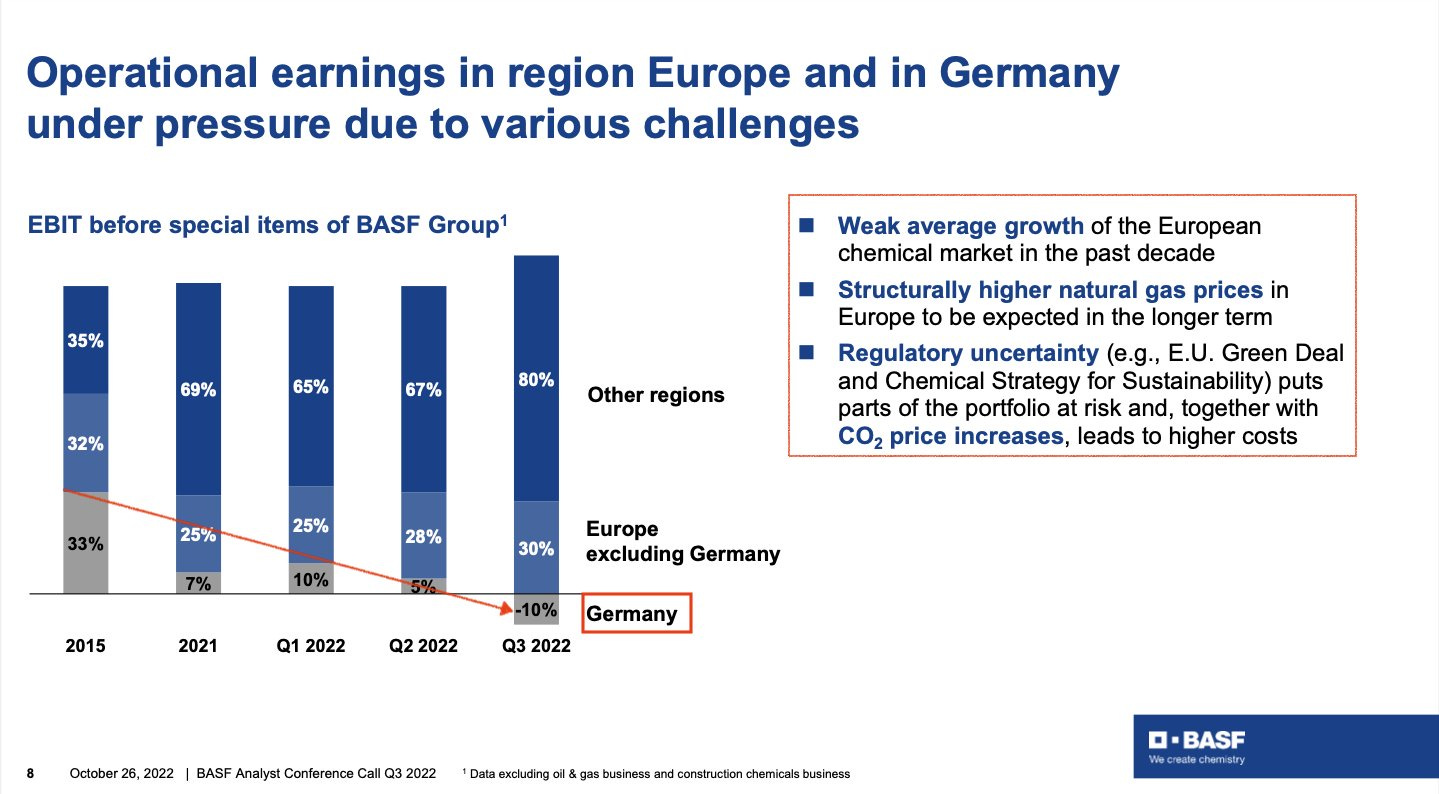

Global chemical giant BASF has announced the permanent closure of several production units at its historic Ludwigshafen site, resulting in the loss of 2,600 jobs, mainly in Europe. According to company chairman Martin Brudermüller, "Europe's competitiveness is increasingly suffering" because of rising energy costs.

The erosion of the German chemical group's margins began with the decline in industrial activity in Europe and worsened with the energy crisis. Last year, business was in the red, forcing BASF to seek growth elsewhere to offset its losses in Germany.

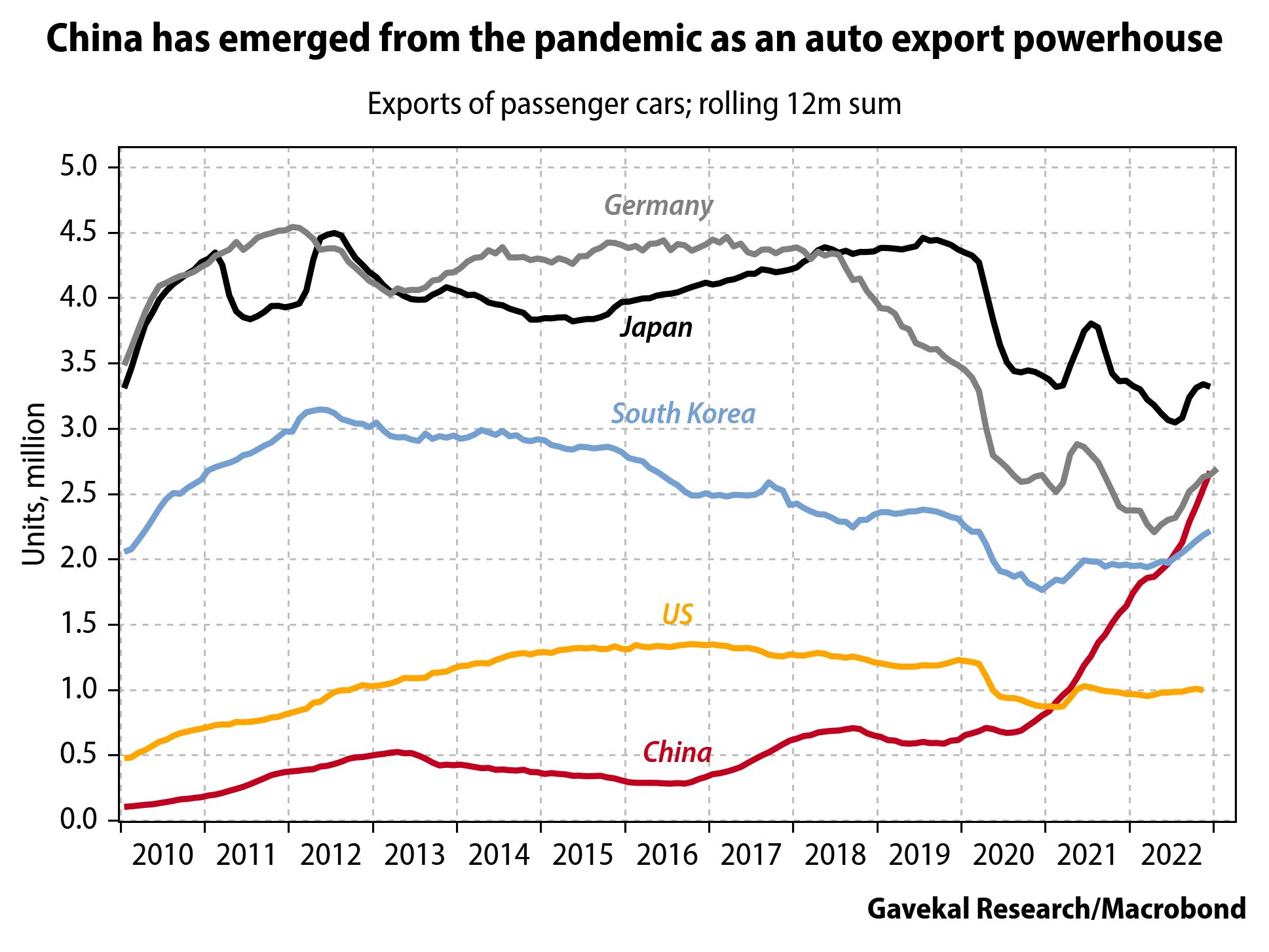

The chemical industry is the first industrial sector to be affected by the energy crisis. However, another flagship sector of German industry is under threat: the automotive industry is undergoing a radical transformation, particularly with the massive arrival of more dynamic Chinese competitors in the field of electric models.

China is poised to overtake Germany as the world's largest exporter of cars. More worryingly, Germany is struggling to take a significant share of the Chinese domestic market. After chemicals, the second pillar of German industry is faltering.

Germany's deindustrialization continues with a 3.6% decline in private investment in machinery and equipment in the fourth quarter. Not only are factories closing, but German companies are now looking to invest in other parts of the world to remain competitive.

Germany, once one of the countries most advantaged by globalization, is now feeling the full impact of deglobalization and rising energy costs.

At the same time, geopolitical tensions have reached a new critical level this week, notably with China's proposal of a peace plan to end the conflict in Ukraine. If this plan is not discussed, China may be forced to end its official neutrality and supply arms to Russia.

The geopolitical event of the week is China's dramatic shift in rhetoric toward the United States.

In an unusually virulent intervention, Chinese Foreign Ministry spokesman Wang Wenbin recalled that in its 240-year history, the United States has gone only 16 years without a war and has tried to assassinate more than 50 foreign leaders...

Chinese diplomacy, which has been rather measured until now, is getting tougher, which marks an escalation in the global geopolitical situation.

The price of gold reflects this inability to bring down the fever triggered by the conflict in Ukraine.

Reproduction, in whole or in part, is authorized as long as it includes all the text hyperlinks and a link back to the original source.

The information contained in this article is for information purposes only and does not constitute investment advice or a recommendation to buy or sell.