Thanksgiving weekend set new records in the US.

Firstly, an all-time record for the number of aircraft in the US sky on November 26, 2023:

The Transportation Security Administration screened 2,894,304 passengers at the nation's airports, marking the busiest day ever for air travel.

An all-time record was also set on Black Friday: online sales generated a record $9.8 billion, up 7.5% on the previous year. On Thanksgiving Day, the day before Black Friday, online sales amounted to $5.6 billion in the US.

A total of $15.4 billion was spent over two days.

Worldwide, Black Friday online sales topped the $70 billion mark for the first time.

This record spending logically led to another record, that of household consumer credit card debt: total credit card debt reached an all-time high of $1.1 trillion. Consumers racked up record levels of debt during Black Friday.

This spike in household debt was accompanied by intensive use of savings reserves. For the first time since the start of the pandemic, the surplus savings in the United States, accumulated during the Covid period, were depleted.

Households are consuming and taking on debt at record levels.

The US government is doing the same.

US public debt increased by $61 billion overnight, reaching a peak of $33.827 billion last Friday. Only $173 billion short of the mind-boggling $34 trillion mark. Just two months ago, the $33 trillion mark was reached.

In addition to being at a record level, this debt is increasing at a rate never seen before.

The consumer engine is firing on all cylinders, and even the rate hikes on credit cards failed to quell the consumer fervor of this promotional weekend.

With rates on card debt now approaching 30%, consumption on credit has become expensive, and the discount offered during these promotional days often doesn't even cover the cost of the credit purchase.

While online sales and air travel have benefited from the consumer craze, the real estate sector has taken a turn for the worse.

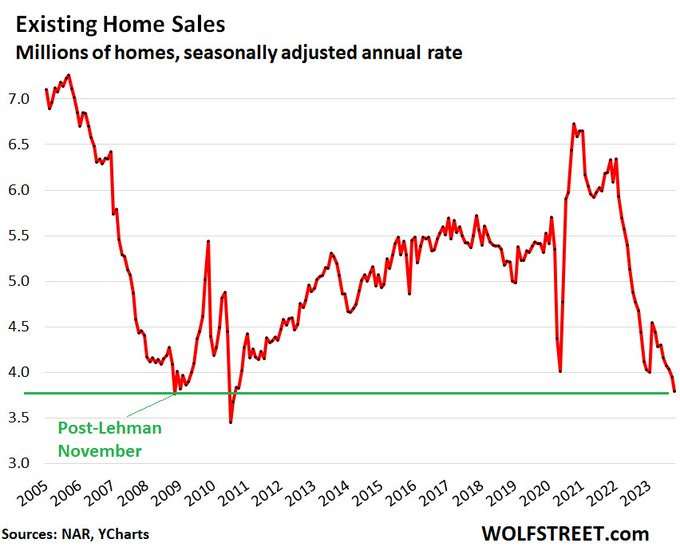

Existing home sales have collapsed since rates were raised:

Activity is now at critical levels, unseen even at the height of the subprime crisis. We are witnessing a historic drying-up of the real estate market, with the number of new loan signatures down by over 80%, or even more depending on the region, since rates were raised.

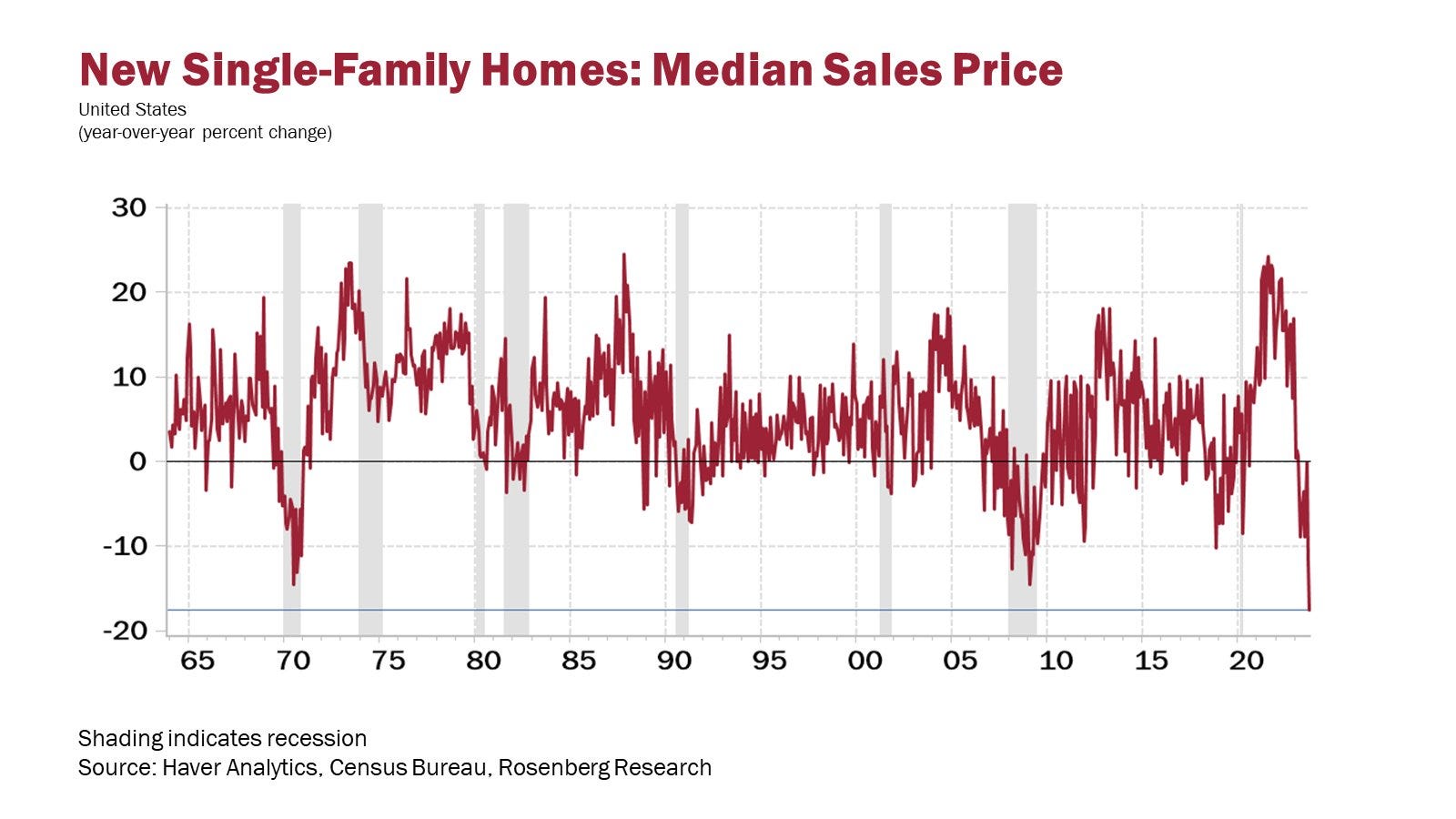

Since the summer, we have even seen a fall in prices, with this month's drop reaching -20% in annual variation. It has to be said that prices had really soared after 2020, and this spectacular fall merely corrects the excesses of recent years.

Although the fall in prices has been a notable feature of recent weeks, what remains worrying is the level of transactions, which is still very low.

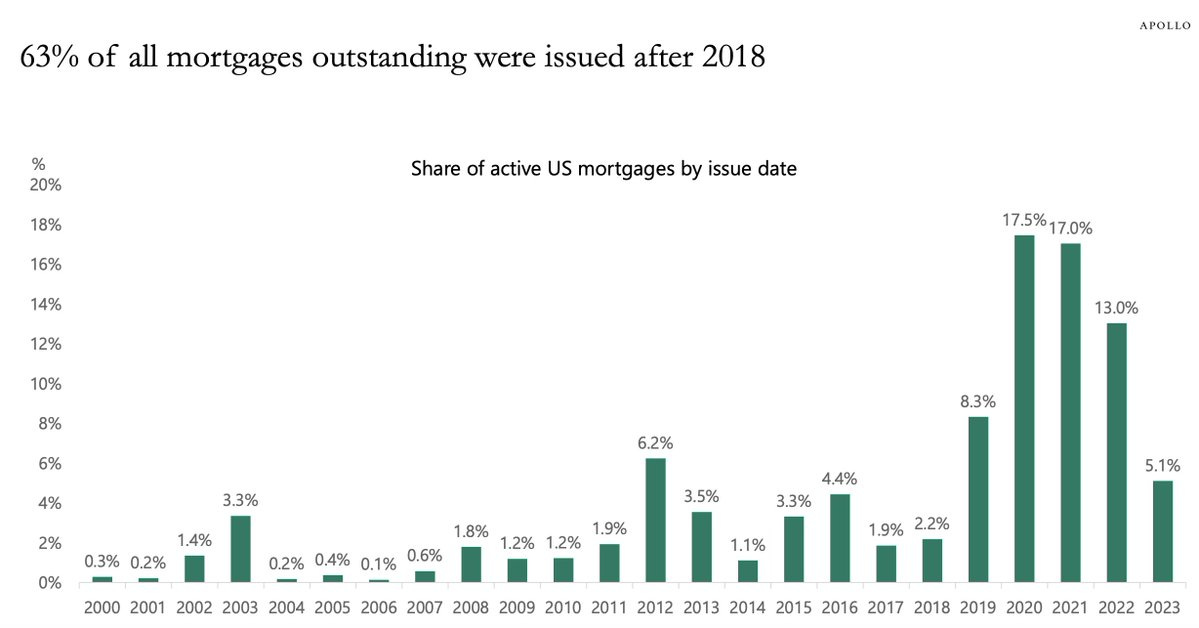

One explanation for this market stall lies in the refinancing of mortgages just before the rate hike. Most households renegotiated their loans while rates were low between 2018 and 2020. Today, almost two-thirds of American households are in this situation.

These Americans have no incentive to move: by keeping their home, they preserve the possibility of repaying at low rates. If they move, they lose this advantage and will have to repay twice as much in their new home.

The low level of repayment compared with what they would actually have to pay, given the level of interest rates, has become an advantage in kind for these households, constituting a real estate asset in its own right!

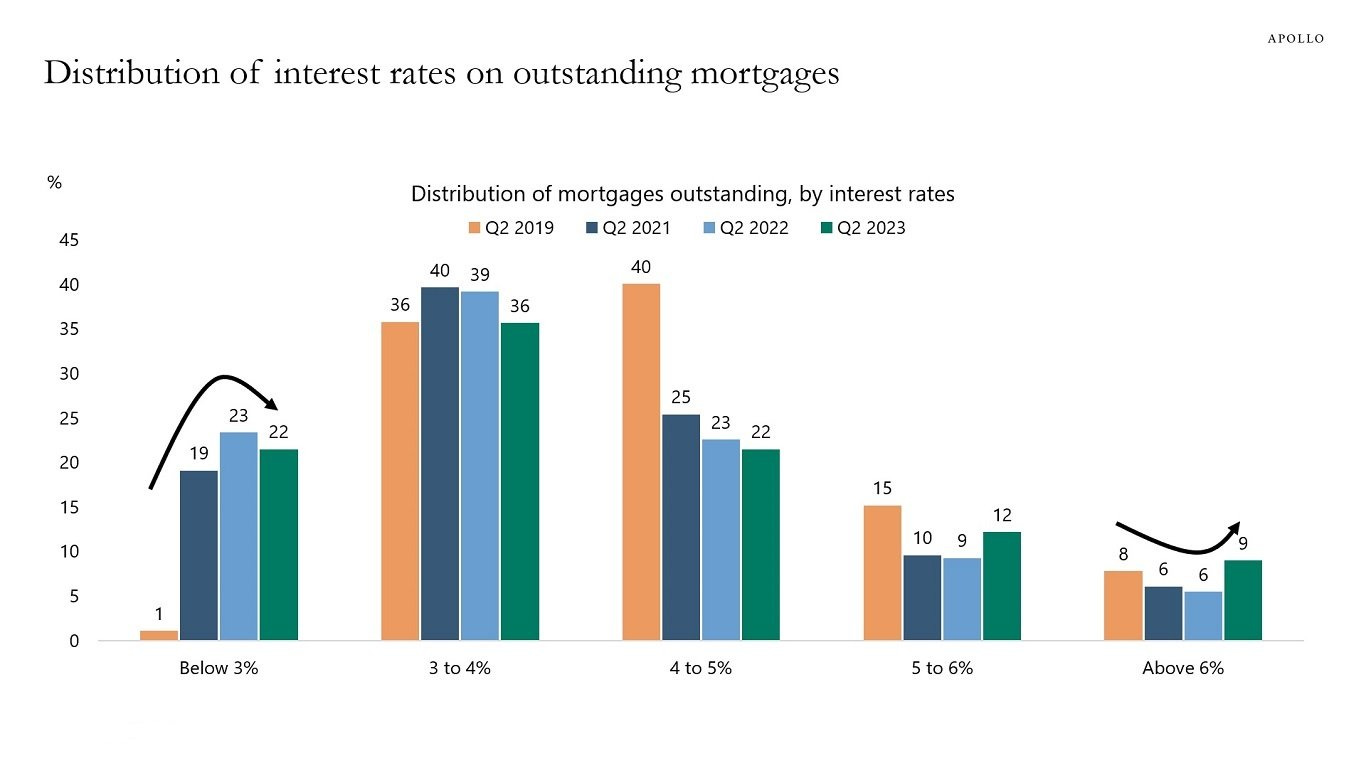

22% of American households continue to benefit from loan repayments of less than 3%. A real bargain that doesn't really encourage them to move!

The monthly cost of a new mortgage has doubled since January 2021. In 2021, the median payment on a new mortgage was around $1,500 per month. It has now reached the record level of $3,000 per month and continues to rise, while mortgage rates reach 8%.

Prices aren't falling enough to attract new buyers, and there's no incentive for homeowners to sell. If they do sell, they lose the advantage of being able to repay their credit-purchased assets at a low rate. Under these conditions, the appeal of real estate is logically eroded.

In other words, real estate is no longer a safe haven due to the stagnation of the real estate market and the absence of investment incentives. This stalemate is driving buyers to inaction, while sellers are encouraged to hold on to their properties to avoid paying double in repayment costs in the event of a move.

In China, the growing disinterest in real estate has also changed savers' behavior towards gold. Partly because stone no longer offered an attractive safe-haven for investors, many households turned to buying physical gold.

The young Chinese generation is particularly affected by this new approach to saving.

Gold Rush in China (@LaurentMaurel_)

— GoldBroker (@Goldbroker_com) September 29, 2023

▶ https://t.co/Aqm4Ph6PMp#gold #China #SGE #Shanghai #yuan pic.twitter.com/4Q8FpbScal

Will we see a similar phenomenon towards the purchase of physical gold in the United States? Could gold once again become a safer and more popular savings vehicle than real estate in Western countries?

In any case, gold's current good form contrasts with the sluggishness of the real estate market.

Last week, the price of gold in dollars set a new record on the Shanghai Gold Exchange. This performance in China should logically lead the price of gold to approach its record high in London.

Reproduction, in whole or in part, is authorized as long as it includes all the text hyperlinks and a link back to the original source.

The information contained in this article is for information purposes only and does not constitute investment advice or a recommendation to buy or sell.